Pre-Sale Property Valuation: Understanding Appraisal Costs

By Housey · Last reviewed 1st of June 2026

Pre-Sale Property Valuation: Understanding Appraisal Costs

Deciding on an asking price is one of the earliest and most consequential steps in selling a UK property. Whether you are a homeowner preparing to move, an executor handling a probate estate, or a landlord selling investment property, understanding which type of valuation you need — and what it costs — helps you enter the market with realistic expectations and the right documentation in hand. The regulatory and legal landscape around property valuations in England and Wales is more nuanced than many sellers realise.

Key points

- Estate agent market appraisals are free but are not independent regulated valuations; obtain at least three from agents actively selling comparable properties in your area.

- A formal RICS Red Book valuation carries legal weight and is required for probate (Inheritance Tax), divorce financial settlements, Capital Gains Tax calculations, Help to Buy equity loan redemption, and shared ownership staircasing.

- RICS residential valuation fees typically range from £150 to £700 for standard UK homes; complex, large, or listed properties usually attract higher fees (indicative, last reviewed 2026-06-01).

- HMRC requires a formal valuation for Capital Gains Tax when selling a property that was not your primary residence throughout ownership — such as a buy-to-let, inherited property, or holiday home.

- An insurance reinstatement valuation is entirely separate from a market valuation; it assesses rebuild cost, not sale price, and is used to set an accurate buildings insurance sum insured.

Types of property valuation in the UK

Valuation type | Who provides it | Typical cost | When you need it | Legal weight |

|---|---|---|---|---|

Estate agent market appraisal | RICS or NAEA-registered estate agent | Free | Setting an asking price | None — opinion only |

RICS Red Book formal valuation | RICS-registered valuer (MRICS or FRICS) | £150–£700+ | Probate, divorce, CGT, Help to Buy, shared ownership | High — RICS-regulated |

Automated valuation model (AVM) | Rightmove, Zoopla, Nationwide | Free | Rough orientation only | None |

Mortgage valuation | Lender-appointed surveyor | £0–£500 | Required by the buyer's mortgage lender | For lender use only |

Insurance reinstatement valuation | RICS or BCIS-qualified surveyor | £250–£750 | Setting buildings insurance sum insured | For insurance purposes |

Indicative UK costs, last reviewed 2026-06-01. Costs vary by property size, type, and location.

Estate agent market appraisals: what they are and are not

A market appraisal from an estate agent is a professional opinion of what your home is likely to achieve in current market conditions. It is not a RICS-regulated valuation. Several points to bear in mind:

- Agents have a commercial interest in winning your instruction, which can create upward pressure on their estimates — sometimes called 'overvaluing to win the pitch'.

- Always obtain at least three appraisals from agents who actively sell comparable properties in your street or postcode.

- Ask each agent to show you comparable evidence: sold prices from Rightmove or the HM Land Registry sold price database.

- An agent's estimate can be revised as market conditions change; it is not a contractual commitment.

For the majority of straightforward residential sales, a free estate agent appraisal is sufficient to set an asking price. You do not need a formal RICS valuation simply to list a property for sale.

When a formal RICS Red Book valuation is required

Certain transactions and legal processes require a formal RICS-compliant valuation under the RICS Valuation — Global Standards 2022:

- Probate: HMRC requires a formal valuation of a deceased person's property as at the date of death for Inheritance Tax purposes.

- Divorce and financial settlement: Courts and solicitors routinely require an independent formal valuation to establish a fair division of assets.

- Capital Gains Tax: If selling a property that was not your primary residence throughout ownership, HMRC requires a formal valuation at the relevant acquisition or change-of-use date.

- Help to Buy equity loan redemption: Homes England requires an RICS-compliant valuation from an independent surveyor to determine the repayment figure.

- Shared ownership staircasing or resale: Housing associations typically require an RICS valuation to determine the fair value of the share being sold or purchased.

- Disputed valuations: If a buyer or their lender challenges your asking price, a formal Red Book valuation from an independent RICS valuer carries significantly more evidential weight than an agent's appraisal.

Which valuation do you need?

- Selling a standard home through an estate agent? Three free market appraisals from active local agents are sufficient for most sellers.

- Selling a probate property or acting as executor? A formal RICS Red Book valuation for Inheritance Tax purposes is required by HMRC.

- Selling a buy-to-let or second property? Confirm with your accountant whether a formal CGT valuation is needed before completion.

- Redeeming a Help to Buy equity loan? Homes England requires an independent RICS valuation — not an estate agent appraisal.

- Involved in divorce proceedings? A jointly instructed RICS valuation is the standard approach in England and Wales.

- Concerned about buildings insurance being accurate? Commission a reinstatement cost assessment from a RICS or BCIS-qualified surveyor — this is a separate instruction from any sale valuation.

What affects the cost of a formal RICS valuation?

Several factors influence how much a residential RICS valuation costs in the UK:

- Property size and type: A two-bedroom flat is quicker to assess than a five-bedroom detached house with outbuildings or a large period property.

- Location: Urban valuers serving active comparable-evidence markets may be competitively priced; rural or specialist areas can attract higher fees.

- Purpose: Probate and matrimonial valuations often involve additional research, correspondence with HMRC, and documentation, increasing the fee.

- Urgency: Expedited turnarounds — for example, to meet a probate or Help to Buy deadline — typically attract a premium.

- Property complexity: Listed buildings, properties with unusual tenure, or those with planning anomalies require more investigation and carry higher professional risk.

- Firm size: Larger RICS practices and sole-practitioner valuers may price differently for identical instructions; it is worth obtaining two or three quotes.

What to ask before instructing a valuer

Before appointing a RICS valuer for a formal pre-sale report:

- Are you RICS-registered (MRICS or FRICS) and do you hold a current practising certificate?

- Have you valued comparable properties in this specific area recently?

- Will the report be issued under RICS Red Book Global Standards 2022 with Market Value as the stated basis of value?

- What documents do you need from me — title register, floor plans, EPC, lease if leasehold?

- Will you inspect the property in person, or is this a desk-based assessment?

- How long will the report take to produce after inspection?

- Is your fee fixed, and does it include VAT?

- What happens if access problems arise on the day of inspection?

Important limitations

Property valuations reflect comparable market evidence available at the date of inspection and can change as the market moves. A RICS valuation is a professional opinion of value, not a guarantee of sale price or a mortgage offer. For tax purposes — Inheritance Tax or Capital Gains Tax — always confirm with your solicitor or accountant which type of valuation is required and which HMRC methodology applies. HMRC rules on property valuations can change, and Homes England requirements for Help to Buy redemptions are subject to periodic revision.

What to ask a qualified professional

- Is a formal RICS valuation required for my specific transaction, or will an estate agent appraisal suffice?

- Which RICS Red Book basis of value applies to my situation — Market Value, Existing Use Value, or another?

- If the property is leasehold, will the unexpired lease term materially affect the valuation?

- For probate purposes, do I need separate valuations for any non-property assets?

- If I am selling a Help to Buy home, what is the current Homes England process and list of acceptable valuers?

When to get professional help

Instruct a RICS-registered valuer rather than relying solely on a free estate agent appraisal when:

- A solicitor, HMRC, a court, or a mortgage lender has requested a formal valuation

- You are selling a probate or inherited property

- You are redeeming a Help to Buy equity loan

- The property is listed, has unusual or complex tenure, or involves unresolved planning history

- You are in a disputed transaction and need independent evidential support for the asking price

- You want to verify that your buildings insurance reinstatement figure is accurate before sale

How Housey can help

Housey connects you with qualified surveyors offering valuation surveys and insurance valuations for pre-sale purposes. Whether you need a formal RICS Red Book report for probate, CGT, or Help to Buy redemption, or a reinstatement cost assessment for your buildings cover, Housey can help you find and compare accredited professionals in your area.

Frequently asked questions

How much does an estate agent valuation cost?

Estate agent market appraisals are free of charge. Agents are motivated by the prospect of winning your sale instruction. You should compare at least three appraisals and ask each agent to show you the comparable sold-price evidence underpinning their estimate, as agents can sometimes overvalue to secure the instruction.

Do I need a formal valuation to sell my house?

For most standard residential sales, no. A free estate agent appraisal is sufficient to set an asking price. A formal RICS Red Book valuation is required only where a legal or regulatory process mandates it — such as probate, Help to Buy equity loan redemption, Capital Gains Tax, shared ownership staircasing, or divorce proceedings.

How long does a RICS property valuation take?

The inspection typically takes 30 minutes to two hours depending on property size and complexity. Most RICS valuers deliver a written report within three to ten working days of inspection. Expedited turnarounds may be available at a premium. Confirm the expected turnaround and any urgency premium when requesting quotes.

Can I challenge an estate agent's valuation?

Yes. An estate agent's market appraisal is their professional opinion and is not binding. If a figure seems unrealistically high or low, ask for the comparable evidence used to support it. You can also check HM Land Registry sold prices for similar properties in your postcode area before deciding on an asking price.

Is a pre-sale valuation the same as a buyer's survey?

No. A pre-sale valuation assesses likely market value. A buyer's survey — such as a RICS Level 2 or Level 3 Home Survey — assesses the physical condition of the property and identifies defects. Some sellers commission a pre-sale condition survey to find issues before listing, but this is entirely separate from a market or Red Book valuation.

Sources and further reading

- RICS Valuation — Global Standards 2022 (Red Book) — RICS

- HM Land Registry: UK House Price Index — GOV.UK

- HMRC: Capital Gains Tax on property — GOV.UK

- Homes England: Help to Buy equity loan — repaying — Homes England

- Citizens Advice: Selling your home — Citizens Advice

Useful next reads

Buying & Moving

Buying & MovingHow to Get Your Property Professionally Valued

To get a professional property valuation in the UK, instruct a RICS Registered Valuer for any formal purpose — mortgage, probate, Help to Buy, or legal proceedings.

Buying & Moving

Buying & MovingSelling Your Home Faster: Strategies for a Quicker Sale

To sell your home faster in the UK, price it accurately from the outset, invest in professional photography, and present the property without clutter or visible defects.

Buying & Moving

Buying & MovingUnderstanding Local Property Values: What Homes Sold For in Your Area

Sold prices for UK properties are publicly recorded by HM Land Registry for England and Wales, Registers of Scotland, and Land and Property Services in Northern Ireland.

Buying & Moving

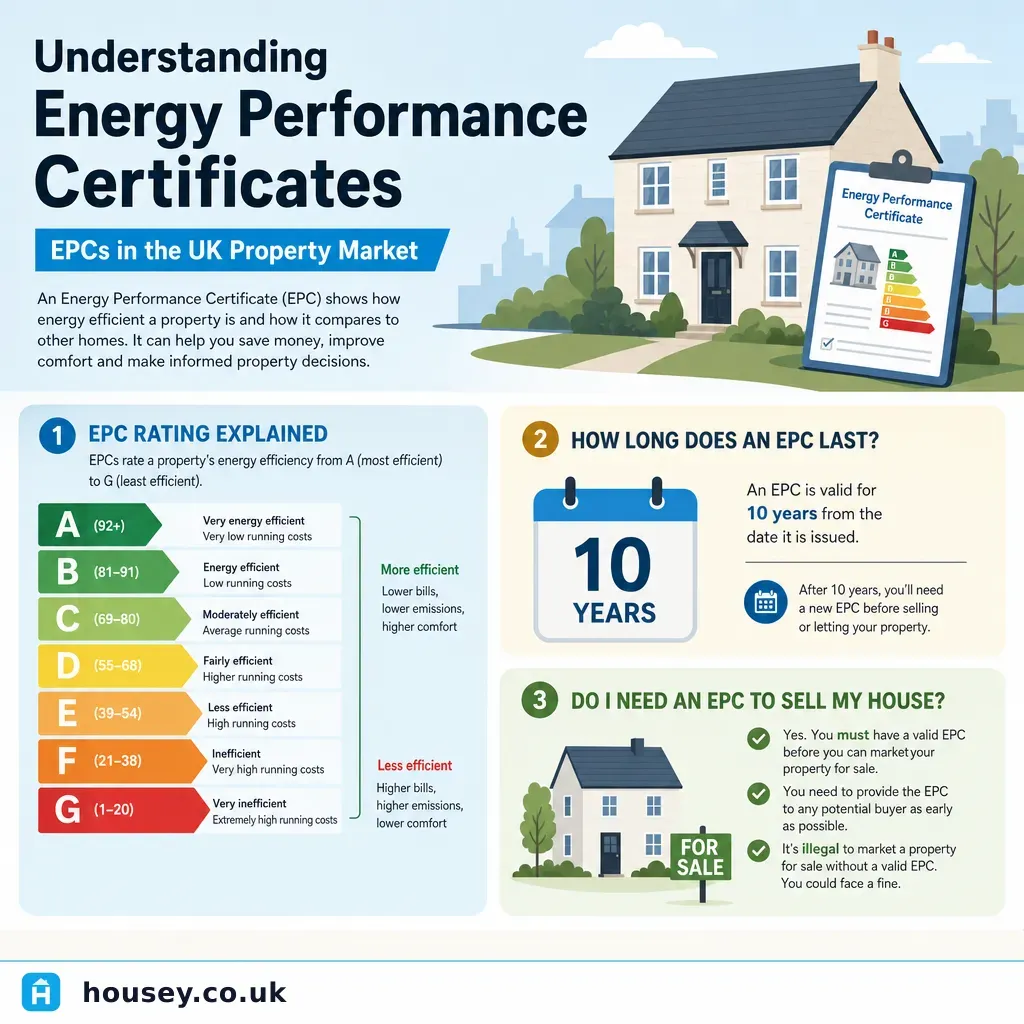

Buying & MovingUnderstanding Energy Performance Certificates: EPCs in the UK Property Market

An Energy Performance Certificate (EPC) rates a property's energy efficiency on a scale from A (most efficient) to G (least efficient).

Buying & Moving

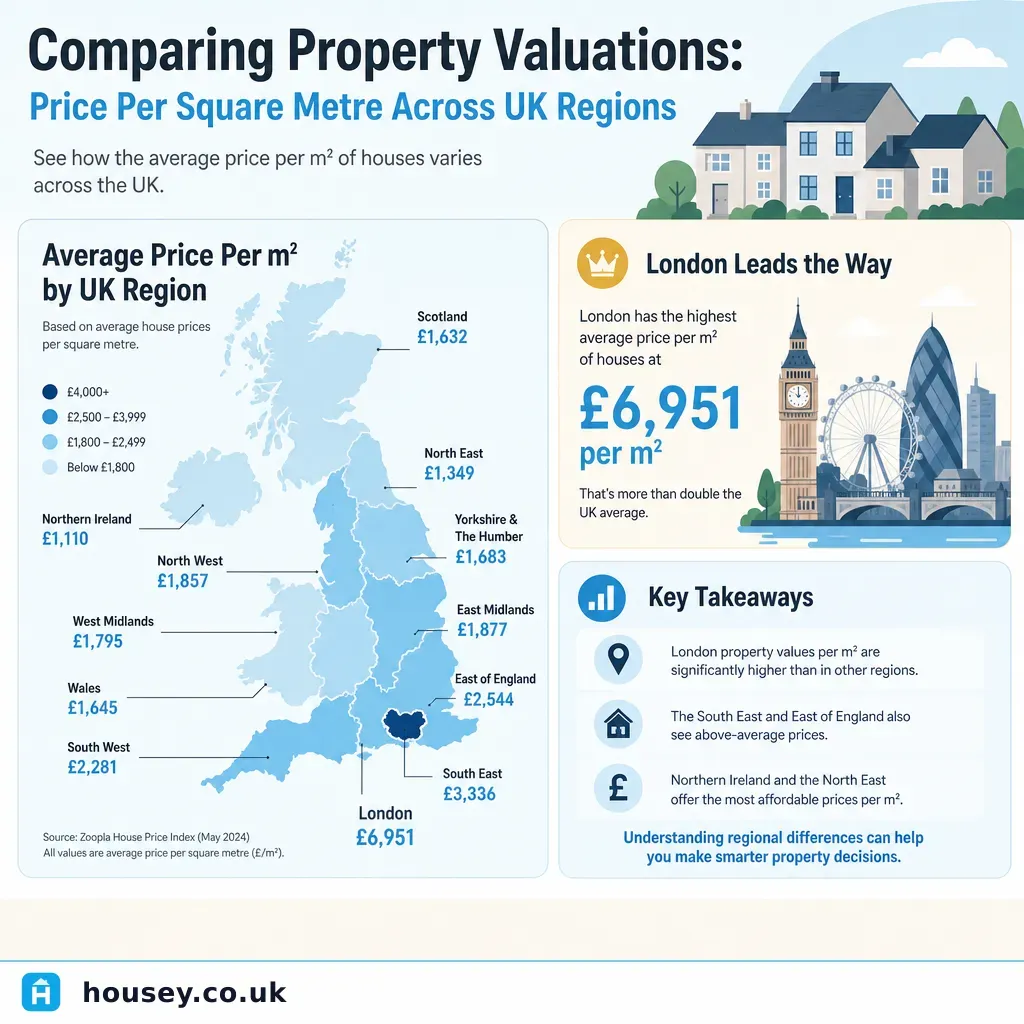

Buying & MovingComparing Property Valuations: Price Per Square Metre Across UK Regions

Property prices per square metre vary dramatically across UK regions.