Comprehensive Budget for a Property Renovation and Resale Project

By Housey · Last reviewed 6th of May 2026

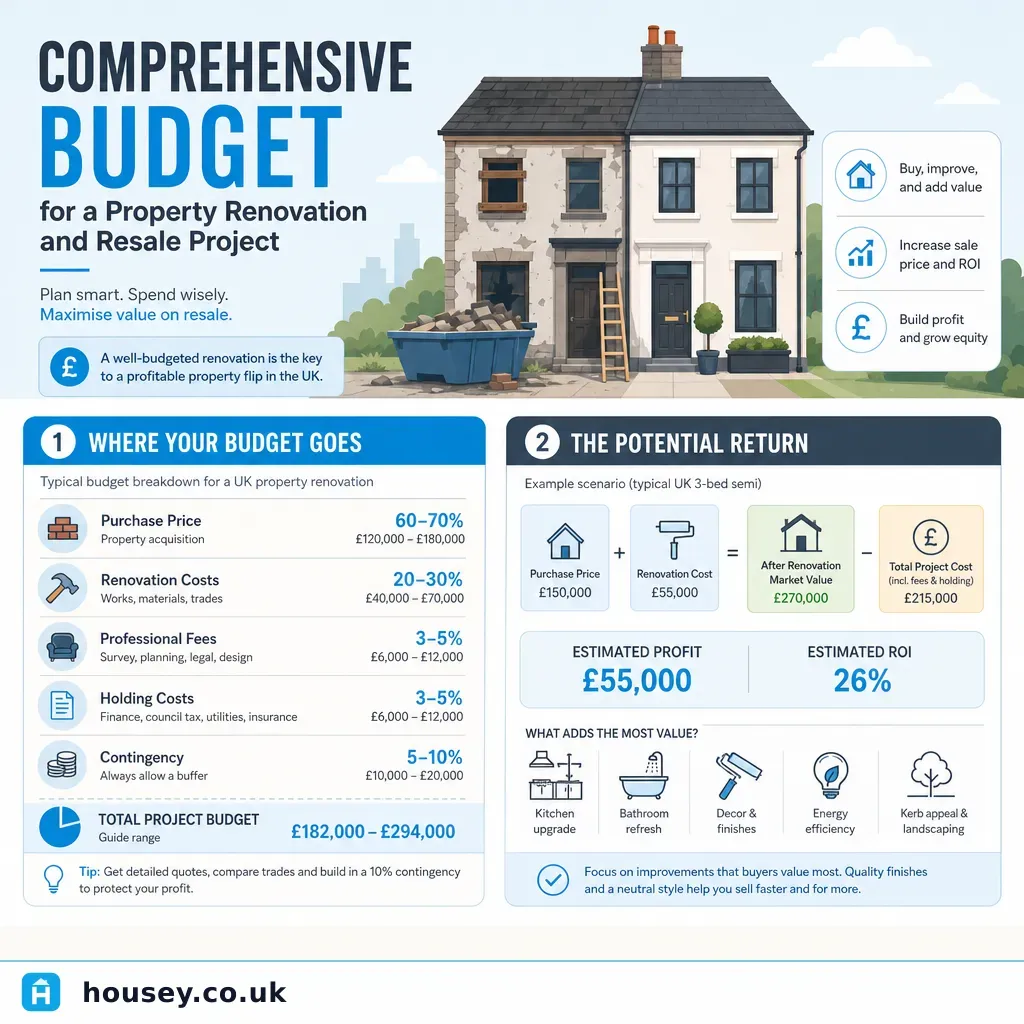

Comprehensive Budget for a Property Renovation and Resale Project

Buying a property to renovate and resell can generate meaningful returns, but the margin between profit and loss is rarely as wide as it appears in a preliminary spreadsheet. This approach — sometimes called a renovation-for-resale or flip — requires a comprehensive budget that accounts for every cost layer from acquisition through to sale completion, not just the build work itself. The question of how to structure that budget arises most often among first-time property investors, landlords considering selling tired stock, and homeowners evaluating whether significant pre-sale investment is worthwhile.

Key points

- Stamp Duty Land Tax (SDLT) is payable on purchase; buyers who already own property pay the higher rate surcharge — currently 3 percentage points above standard rates in England and Northern Ireland as at May 2026 — which on a £150,000 purchase adds approximately £5,500 to acquisition costs.

- A RICS Level 3 structural survey before exchange is standard practice for any renovation project property; the typical cost of £500–£1,500 is minor relative to the risk of defects discovered after contracts are exchanged.

- Capital Gains Tax (CGT) is payable on profit from selling a property that was not your main home; the principal private residence exemption does not apply to investment or renovation-for-resale purchases — take qualified tax advice before committing.

- A 15–20% contingency on total construction costs is the minimum recommended buffer; pre-1940s properties and those with visible defects frequently require more.

- Building Regulations approval is required for structural alterations, electrical re-wiring, new plumbing, and extensions; absence of approval can block a sale if buyers' solicitors raise it on enquiry.

How to structure your renovation budget

A complete renovation-for-resale budget has four distinct cost layers that are commonly conflated or incompletely estimated:

Layer 1: Acquisition costs

- Purchase price

- Stamp Duty Land Tax (including higher rate surcharge if applicable)

- Conveyancer or solicitor fees: typically £1,000–£2,500 plus disbursements

- RICS Level 3 structural survey: £500–£1,500

- Mortgage or bridging finance arrangement fees and monthly interest during the hold period

- Buildings insurance from exchange

Layer 2: Pre-construction costs

- Structural engineer's assessment if structural work is planned: £500–£1,500

- Architect or architectural technologist drawings: £1,500–£5,000 depending on scope

- Building Regulations application fee: £200–£1,000 depending on project value

- Party wall surveyor fees where applicable: £700–£2,000 per award

- Specialist surveys (asbestos, Japanese knotweed, drainage CCTV): £150–£600 each

Layer 3: Construction costs

- Structural repairs (roof, foundations, walls, lintels): highly variable by condition

- Plumbing and heating — boiler replacement and system: £3,000–£12,000

- Full electrical re-wire and consumer unit: £2,500–£8,000 for a three-bedroom property

- Damp treatment and replastering as required

- Kitchen fit-out: £4,000–£20,000 depending on specification

- Bathroom and en-suite fit-out: £3,000–£12,000 each

- Windows and external doors: £5,000–£20,000 depending on number and specification

- Decoration and flooring throughout

- Contingency: minimum 15–20% of construction total

Layer 4: Selling costs

- Estate agent fees: typically 1–3% of sale price

- Conveyancer or solicitor fees: £800–£2,000

- Energy Performance Certificate: £60–£120 (required for all residential sales)

- Property photography and floorplan: £150–£500

- Capital Gains Tax on any gain, if applicable

Indicative UK costs, last reviewed 2026-05-06. Costs vary by region, property size, specification, and contractor. Always obtain multiple quotes.

Which renovations add the most resale value in the UK?

Not every pound spent returns more than a pound at sale. Understanding where expenditure translates into buyer value is central to managing a renovation project profitably.

Renovation | Value uplift potential | Best suited to | Common pitfall |

|---|---|---|---|

Structural defect repair (roof, damp, movement) | Essential — unlocks mortgageability | Any property with known defects | Must be resolved before cosmetic spend |

Full re-wire and new consumer unit | High — unlocks buyer finance | Pre-1980s properties | Often invisible but expected in the price |

Boiler replacement and new heating | High | Properties with old or absent central heating | Radiator sizing and pipework replacement costs |

New kitchen | High (mid-market) | Properties with original or very dated kitchen | Over-specifying beyond the local ceiling |

New bathroom(s) | Medium–High | Period homes with a single dated bathroom | Wet room vs bath: consider local buyer profile |

Loft conversion | High — adds a bedroom | Properties where bedroom count caps value | Building Regulations and structural load costs |

Single-storey extension | Medium–High | Properties with spare garden space | Planning permission; build cost vs local ceiling |

Decoration and cosmetics | Medium — low cost, high visibility | All properties | Neutral palettes outperform personal choices |

A worked UK property scenario

The following uses rounded illustrative figures to show how budget layers combine. It is not a guarantee of typical outcomes — actual costs and achieved prices vary materially by location, condition, and market.

Property: 1960s semi-detached, three bedrooms, Birmingham. Purchase price: £135,000. Comparable fully renovated sales on the same street: £190,000–£200,000.

Acquisition costs:

- Purchase price: £135,000

- SDLT (higher rate, buyer already owns property): approximately £5,550

- Conveyancing: £1,500

- RICS Level 3 structural survey: £750

- Bridging finance (six months at approximately 0.85%/month): approximately £6,885

- Buildings insurance: £600

- Acquisition subtotal: approximately £150,285

Construction budget:

- New boiler and central heating: £5,000

- Full electrical re-wire and consumer unit: £5,500

- New kitchen with fit-out: £8,000

- New bathroom: £4,500

- Damp treatment, replastering, and decoration: £7,000

- Flooring throughout: £3,500

- Contingency (15%): £5,025

- Construction subtotal: approximately £38,525

Selling costs:

- Estate agent at 1.5%: approximately £2,925

- Conveyancing: £1,200

- EPC: £80

- Property photography and floorplan: £300

- Selling subtotal: approximately £4,505

Gross margin before CGT:

- Anticipated sale price: £195,000

- Total all-in costs: £150,285 + £38,525 + £4,505 = £193,315

- Gross margin before CGT: approximately £1,685

This scenario shows how tight the margin can be when all cost layers are included. A 10% construction cost overrun (£3,852) eliminates the margin entirely before CGT is considered. Accurate pre-purchase budgeting and a realistic assessment of the local ceiling price are what separate profitable projects from loss-making ones.

What not to assume when budgeting for resale

Do not assume the structural survey is optional. A RICS Level 3 survey before exchange is the most cost-effective step in any renovation project. Defects undiscovered before purchase — Japanese knotweed, structural movement, asbestos, drainage failure — can destroy a project's economics once found post-exchange.

Do not assume permitted development covers your plans. Extension, loft conversion, and change-of-use rights depend on the property's planning history, location, and the local authority's restrictions. Verify with the local planning authority before including any such element in your budget.

Do not assume the local ceiling price is your ceiling. Every road and postcode has a price above which properties struggle to sell regardless of specification. Over-specifying — fitting a premium kitchen in a street where comparable sales top out at £160,000 — is one of the most common and costly renovation mistakes.

Do not assume contractors are immediately available. Quality contractors in most UK markets are booked 6–12 weeks ahead. Factor this lead time into your finance model; every extra week of bridging finance is a real and measurable cost.

Do not assume the market will hold. A six-month renovation project may complete into a different pricing environment. Model a scenario where the achieved sale price is 5–10% below expectation and check whether the project remains viable.

Do not assume cosmetic renovation is sufficient if structural defects exist. Mortgage valuers and buyers' surveyors will identify structural issues. Buyers will reduce their offers or withdraw. Address structural problems before decorating.

Homeowner checklist: before committing to a renovation-for-resale project

When to get professional help

A structural survey from a RICS-qualified surveyor is essential before purchasing a renovation project property. A mortgage valuation is conducted for the lender's purposes and offers no equivalent protection to the buyer.

For any element involving structural alterations, appoint a structural engineer before finalising scope and budget. Unanticipated structural requirements discovered mid-build — a steel beam where a timber lintel was expected, or unexpected foundation issues — are the most common trigger for major budget overruns. Building control consultants can manage the regulatory approval process and help avoid delays that extend your holding costs.

How Housey can help

Housey connects you with qualified professionals throughout a renovation-for-resale project. Start by requesting quotes for a structural survey before exchange, then work with building control consultants to manage regulatory approvals efficiently. When the project is complete, property photography and floorplans present the finished property at its best, and a valuation survey can confirm post-renovation market value before you set your asking price.

Frequently asked questions

What contingency should I include in a renovation-for-resale budget?

Most experienced renovation investors budget a minimum of 15% contingency on total construction costs. For Victorian, Edwardian, or interwar properties, or any property with visible damp, significant roof work, or suspected structural issues, 20% is more prudent. Contingency is most effective when held as a cash reserve rather than borrowed on bridging finance, as unexpected spend on high-rate finance significantly erodes project margins.

Which issues are most likely to prevent or delay a resale in the UK?

Properties with unresolved structural movement, active damp ingress, non-compliant electrical installations (no valid EICR), Japanese knotweed, or drainage failure are frequently declined or restricted by mortgage lenders. Buyers' surveyors will flag these defects, and buyers may reduce their offer or withdraw entirely. Resolving structural and compliance issues before listing is almost always more cost-effective than accepting a heavily discounted offer.

Do I need an architect for a renovation-for-resale project?

Not necessarily. Straightforward internal renovations — replacing a kitchen or bathroom, re-wiring, fitting a new boiler, or decorating — do not require an architect. Where the scope includes a structural opening, extension, loft conversion, or change of use, you will need a chartered architect or an architectural technologist to produce Building Regulations drawings. Building control approval is required for these elements regardless of whether planning permission is also needed.

How do I find the ceiling price for a renovation target property?

Search HM Land Registry sold price data, available free on GOV.UK, filtering for the same road and nearby streets, the same property type, and a similar floor area to your completed property. Rightmove and Zoopla also display sold prices. Estate agents active in the area can provide informal appraisals. Use completed sales data rather than asking prices, and focus on transactions from the previous 12–18 months where sufficient data exists.

Is Capital Gains Tax always payable on a renovated property resale?

CGT is generally payable on profits from selling a property that was not your main home during the period of ownership. The principal private residence exemption does not apply if you purchased the property as an investment or renovation project. CGT rates, annual allowances, and reliefs can change; your specific liability depends on your income, the gain, and allowable costs including professional fees and qualifying improvement expenditure. Take advice from a qualified accountant before purchasing.

Sources and further reading

- Stamp Duty Land Tax — GOV.UK

- Capital Gains Tax: What You Pay It On, Rates and Allowances — GOV.UK

- UK House Price Index — HM Land Registry

- RICS Home Surveys — RICS

- Permitted Development Rights for Householders: Technical Guidance — GOV.UK

- Building Regulations: Approved Documents — GOV.UK

Useful next reads

Buying & Moving

Buying & MovingManaging Delays with Removal Companies: Rights and Resolution

If a removal company is late, your rights depend on your contract and whether the company is BAR-registered.

Buying & Moving

Buying & MovingUnderstanding Leasehold Property: Rights and Responsibilities

Leasehold means you own a time-limited interest in a property while the freeholder owns the land and building.

Buying & Moving

Buying & MovingThe Complete Property Buying Guide: From Search to Purchase

Buying a property in England and Wales typically takes 3–6 months from accepted offer to completion.

Buying & Moving

Buying & MovingLeasehold Property Purchase: Complexity and Key Considerations

Buying a leasehold property means purchasing the right to occupy for a fixed term rather than owning the land outright.

Buying & Moving

Buying & MovingFirst-Time Buyer Essentials Checklist

Buying your first home involves obtaining a mortgage in principle, making an offer, instructing a solicitor, arranging a survey, and exchanging contracts before completion.