Remortgaging Your Property: Process, Options, and Benefits

By Housey · Last reviewed 25th of May 2026

Remortgaging Your Property: Process, Options, and Benefits

Remortgaging — switching your existing mortgage to a new deal, either with your current lender or a different one — is one of the most financially significant decisions a UK homeowner makes on a regular basis. It typically arises when an introductory fixed or tracker deal is approaching its end date, or when you want to release equity for home improvements or debt consolidation. Getting the timing and product choice right can save thousands of pounds over the life of the loan.

Key points

- Most introductory mortgage deals run for 2–5 years; once they expire, the lender moves you to their Standard Variable Rate (SVR), which is usually significantly higher than competitive remortgage rates.

- You can usually begin the remortgage process 3–6 months before your current deal ends without triggering early repayment charges (ERCs).

- Early repayment charges typically range from 1% to 5% of the outstanding loan balance — always check your original mortgage offer document for the exact figure and expiry date.

- A new lender will usually require a property valuation (desktop, drive-by, or full inspection) to confirm your loan-to-value (LTV) ratio before issuing a mortgage offer.

- Remortgaging to release equity is subject to the lender's affordability assessment and maximum LTV limits, commonly 80–85% for straightforward residential properties.

What is remortgaging and why do homeowners do it?

Remortgaging means replacing your current mortgage with a new one secured against the same property. You may switch to a new lender entirely — requiring a full legal change — or take a new deal with your existing lender, which is often called a product transfer. A product transfer is typically faster and cheaper, as it requires no legal work or new property valuation.

The most common reasons UK homeowners remortgage are:

- Avoiding the Standard Variable Rate: When an introductory deal ends, lenders move borrowers onto their SVR, which often runs several percentage points above the best available fixed or tracker rates.

- Releasing equity: Accessing equity built through capital repayment or house price growth to fund home improvements, consolidation, or other significant expenditure.

- Changing mortgage type: Moving from interest-only to repayment, or switching from a variable to a fixed rate for payment certainty.

- Change in circumstances: A change in income, a relationship breakdown, or an intention to let the property may require a different mortgage product.

The remortgage process step by step

- Check your current deal terms. Find your mortgage offer document and note the deal end date and any ERCs. ERCs can make early switching costly, so confirm these figures before making any decision.

- Start researching 3–6 months before the end date. Most lenders allow you to lock in a rate up to six months ahead, protecting you against rate rises whilst completing at the end of your current term.

- Calculate your loan-to-value (LTV). Divide your outstanding balance by an estimate of your property's current value. A lower LTV — below 60%, 75%, or 80% — typically unlocks better rates and wider lender choice.

- Compare products on total cost, not just rate. Use the total cost over the deal period (headline rate plus all fees) as the basis for comparison. Arrangement fees of £999–£1,999 are common; on smaller balances, they can outweigh a marginally lower rate.

- Submit an application. Provide income and expenditure information, consent to a credit check, and arrange a lender valuation of the property.

- Legal work. A full remortgage to a new lender requires a solicitor or licensed conveyancer to handle the title transfer. Many lenders include a free panel legal service; a product transfer requires no legal work at all.

- Completion. The new lender redeems the old mortgage, the new deal begins, and the new charge is registered at HM Land Registry.

Indicative UK costs, last reviewed 2026-05-25. Arrangement fees, valuation fees, and legal costs vary by lender and loan size. Always obtain a full mortgage illustration (ESIS) from a regulated adviser before committing.

Fixed, tracker, or variable: which deal type suits you?

Mortgage type | Best for | Not ideal for | Key risk |

|---|---|---|---|

Fixed rate (2-year) | Short-term certainty; flexibility to switch again soon | Long-term rate security | Rate may be above market at end of deal |

Fixed rate (5-year) | Budget stability over the medium term; fewer remortgage cycles | Those planning to move or overpay substantially | ERCs typically apply for the full 5 years |

Tracker (base rate + margin) | Those who want to benefit if the Bank of England base rate falls | Borrowers who need predictable monthly payments | Payments rise directly with base rate increases |

Discount variable | Short-term cost saving if the lender's SVR is reduced | Those who need payment certainty | SVR changes at lender's discretion |

Offset mortgage | Higher earners with significant savings seeking tax-efficient interest reduction | Smaller savers or those needing simple products | Complexity; linked savings account typically earns no interest |

Should you remortgage or do a product transfer?

- Choose a product transfer if your current lender offers a competitive rate, you want to avoid legal fees and a new valuation, and your LTV has not improved significantly since your original purchase.

- Choose a full remortgage if another lender offers a meaningfully better product — and the saving outweighs the fees — your LTV has improved and you want to access a better pricing tier, or you need to borrow additional funds your existing lender will not provide.

- Ask a whole-of-market mortgage broker if you are unsure — they can compare product transfers and open-market deals simultaneously, and many charge no fee to the borrower.

- Check your ERC position first — if you are well within a fixed deal period, early repayment charges may make any switch uneconomical until closer to the end date.

What to ask before accepting a remortgage offer

- What is the total cost over the deal period, including all fees?

- Is the arrangement fee added to the loan or paid upfront, and how much does that difference cost over the deal period?

- What are the early repayment charges and when exactly do they expire?

- What rate will I revert to at the end of the deal, and how does it compare to the market?

- What are the overpayment allowances during the deal period (typically 10% per year without penalty)?

- Is the lender's free legal service sufficient for my property type, or should I instruct my own solicitor?

- What is the maximum LTV for this product, and which pricing band does my current property value place me in?

When to get professional help

A regulated mortgage adviser (holding FCA authorisation) is worth consulting before any remortgage — and is essential in more complex situations:

- Your income has changed since your original mortgage — self-employment, maternity or paternity leave, or irregular income may be assessed differently by lenders.

- You want to borrow additional funds alongside the remortgage, such as for a loft conversion or extension.

- You are considering releasing equity for significant home improvements that may require planning permission or building regulations approval.

- Your property is of unusual construction, is listed, or has a short remaining lease — lender appetite for these varies considerably.

- You are unsure whether to fix, track, or consider an offset product given current market conditions.

Always confirm your adviser is authorised on the FCA Financial Services Register.

How Housey can help

If your remortgage involves raising funds for home improvements or you need support with the legal process of switching to a new lender, our conveyancing service can connect you with regulated solicitors who handle remortgage legal work efficiently and cost-effectively.

Frequently asked questions

How long does a remortgage take in the UK?

A product transfer with your existing lender can complete within days or a week. A full remortgage to a new lender typically takes 4–8 weeks from application to completion, depending on valuation timescales and how quickly legal work progresses. Beginning the process 3–6 months before your deal ends gives you a comfortable buffer and avoids any gap on the Standard Variable Rate.

Do I need a solicitor to remortgage?

A product transfer with your existing lender requires no solicitor. A full remortgage to a new lender involves registering a new mortgage charge at HM Land Registry, which requires legal work. However, many lenders provide a free panel legal service that is sufficient for straightforward properties. You can instruct your own solicitor if you prefer independent advice throughout the process.

Can I remortgage if I have bad credit?

It may be harder to access competitive rates with adverse credit on record, but specialist lenders do offer remortgage products for borrowers with CCJs, defaults, or missed payments. A mortgage broker experienced in adverse credit situations is advisable. Check your credit file with the main UK agencies — Experian, Equifax, and TransUnion — before applying so you can see what lenders will see.

What is an agreement in principle for a remortgage?

Also called a decision in principle (DIP), this is a conditional indication from a lender of how much they would lend, based on an initial credit check and basic information. For a remortgage, it is useful for identifying which rate tiers you may qualify for before committing to a full application and a hard credit search on your file.

Sources and further reading

- Remortgaging your home guide — MoneyHelper (HM Treasury / FCA)

- Mortgage guidance for consumers — Financial Conduct Authority

- HM Land Registry practice guides — HM Land Registry / GOV.UK

- FCA Financial Services Register — Financial Conduct Authority

Useful next reads

Buying & Moving

Buying & MovingCost-Effective Relocation: Strategies for Saving Money When Moving House

Moving house in the UK involves costs well beyond the removal van — stamp duty, conveyancing, surveys, and storage all add up.

Buying & Moving

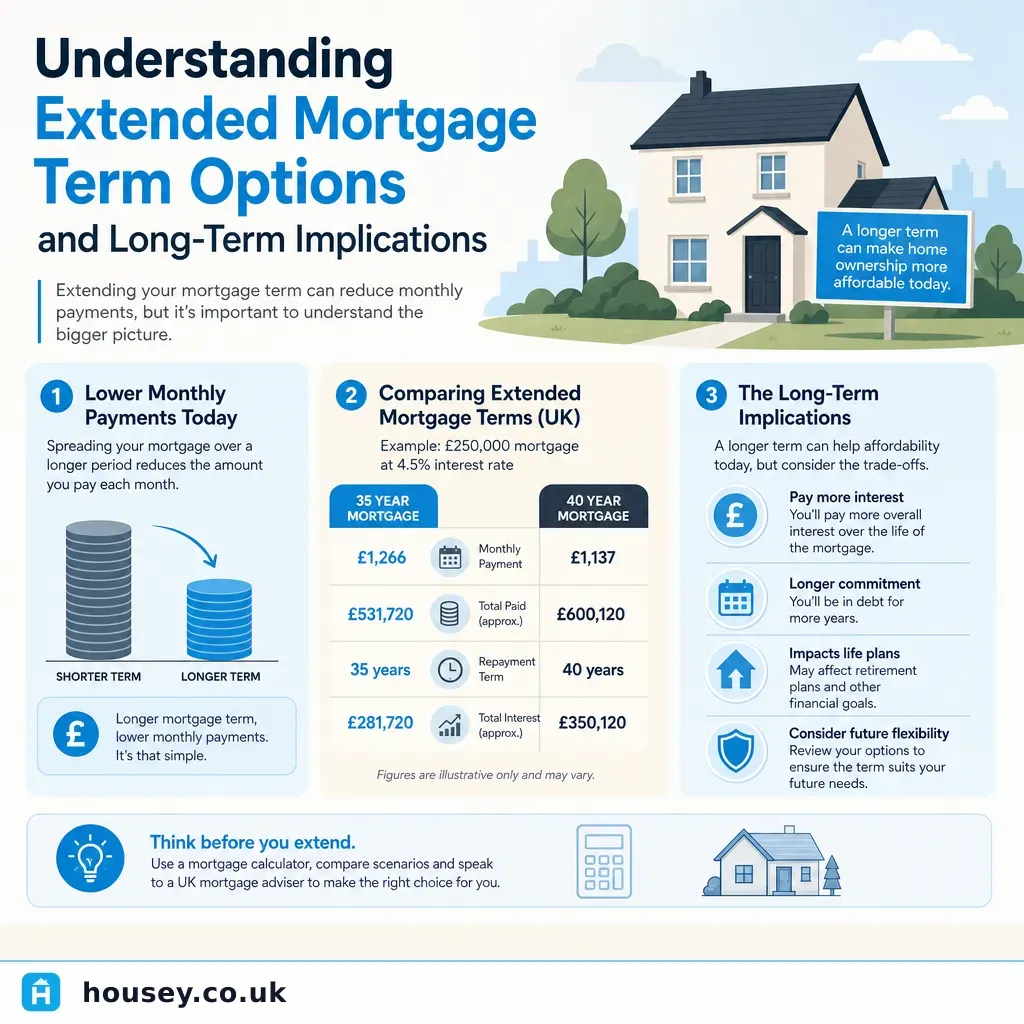

Buying & MovingUnderstanding Extended Mortgage Term Options and Long-Term Implications

UK lenders commonly offer mortgage terms of 25 to 40 years.

Buying & Moving

Buying & MovingManaging Delays with Removal Companies: Rights and Resolution

If a removal company is late, your rights depend on your contract and whether the company is BAR-registered.

Buying & Moving

Buying & MovingUnderstanding Leasehold Property: Rights and Responsibilities

Leasehold means you own a time-limited interest in a property while the freeholder owns the land and building.

Buying & Moving

Buying & MovingThe Complete Property Buying Guide: From Search to Purchase

Buying a property in England and Wales typically takes 3–6 months from accepted offer to completion.