Which Home Improvements Add Real Value to Your Property?

By Housey · Last reviewed 11th of May 2026

Which Home Improvements Add Real Value to Your Property?

For many UK homeowners, renovating is not purely about comfort — it is also a financial calculation. Whether preparing to sell, raising funds through remortgaging, or making a long-term investment decision, understanding which improvements tend to translate into measurable value — and which rarely recoup their cost — is essential before committing to significant spend.

Key points

- Loft conversions typically add 10–20% to a property's value and often deliver one of the strongest returns of any home improvement, particularly in areas with a large price gap between two- and three-bedroom properties.

- Single-storey kitchen extensions consistently rank among the highest-value improvements in UK market research, with typical uplifts in the range of 5–15%.

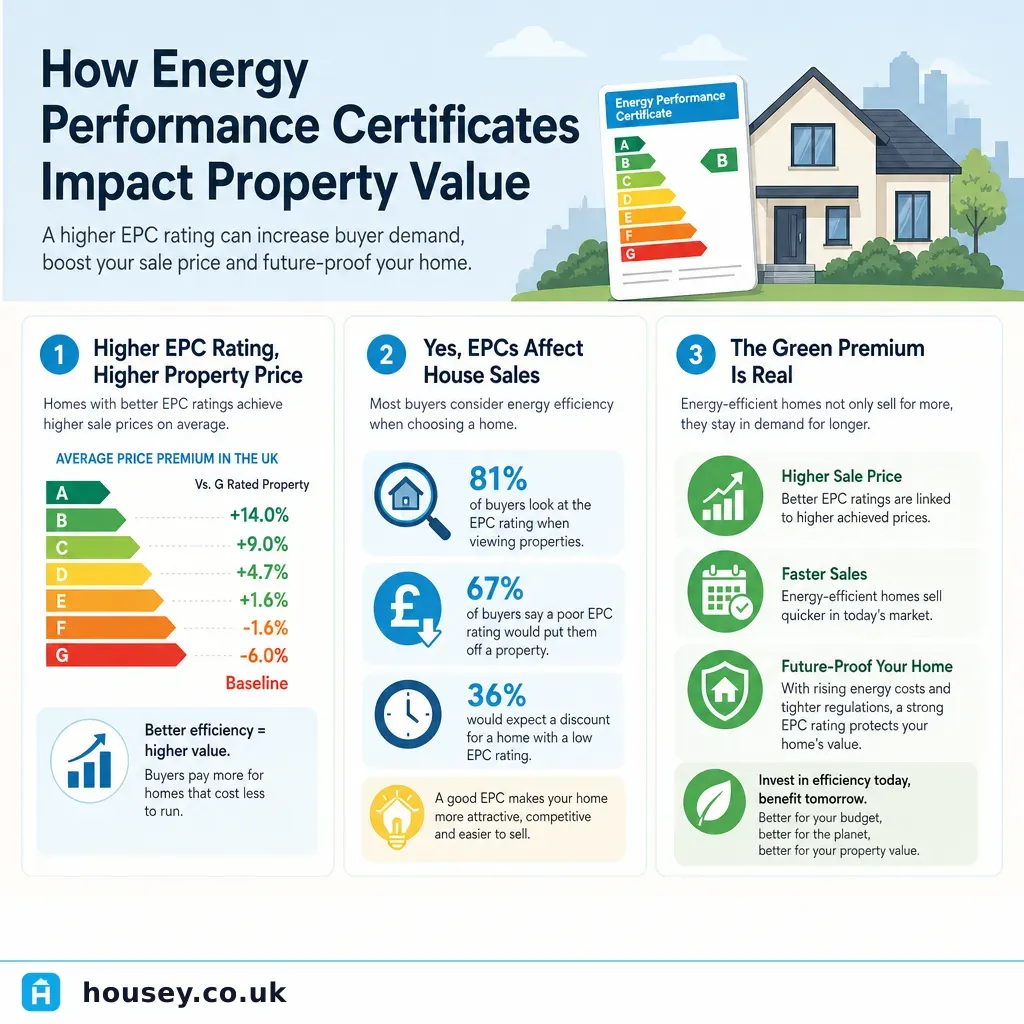

- Energy Performance Certificate (EPC) ratings increasingly affect buyer decisions and mortgage availability; improving from band E to band C can measurably strengthen saleability.

- Permitted development rights allow many extensions and loft conversions without full planning permission, but rules vary by property type, location, and whether an Article 4 direction applies.

- Over-improvement relative to the neighbourhood price ceiling — spending significantly more than the top comparable sale on your street — rarely recovers its full cost.

Which improvements most reliably add value?

Improvement | Typical value uplift (indicative) | Planning usually required? | Best suited to | Risk if done poorly |

|---|---|---|---|---|

Loft conversion | 10–20% | Usually not (permitted development) | Victorian terraces, semi-detached homes | Structural issues, inadequate insulation, insufficient head height |

Single-storey rear extension | 5–15% | Often not (up to 4 m under PD for attached) | Most house types | Damp ingress, substandard build quality |

Double-storey extension | 10–20% | Usually required | Larger homes with adequate budget | Planning refusal, party wall disputes |

Kitchen refurbishment | 3–8% | No | Any property | Over-specification for the local market |

Bathroom addition or upgrade | 2–5% | No | Homes with only one bathroom | Poor waterproofing, substandard plumbing |

EPC and energy-efficiency upgrades | Variable; improves saleability and reduces buyer negotiation | No | Pre-2000 homes; landlords approaching regulatory deadlines | Moisture risk if retrofit is not properly specified |

New roof or roof repairs | Rarely adds above cost; prevents value loss | No | Homes with ageing or failing roof coverings | Ongoing structural damage and survey flags if deferred |

Garage conversion | 5–10% | Sometimes required | Properties where parking is not a premium factor | Loss of perceived parking value in car-dependent locations |

Indicative value uplifts. Returns vary significantly by location, property type, and quality of execution. Indicative UK costs, last reviewed 2026-05-11.

Loft conversions: often the strongest return

A loft conversion typically creates an additional bedroom — sometimes with an en-suite — which directly addresses the buyer criteria most likely to trigger a meaningful price premium. The uplift is most pronounced where the price gap between a two-bedroom and three-bedroom property is significant, as is often the case in Greater London, commuter towns, and high-demand urban areas.

The main conversion types are:

- Velux conversion: No structural alteration to the roof pitch; roof lights added to the existing slope. Lowest cost option, typically £20,000–£30,000.

- Dormer conversion: A box-like extension added to one or both roof slopes, creating substantially more usable floor space. Typically £30,000–£50,000.

- Hip-to-gable: Restructures the end roof slope on a semi-detached or detached property. Often combined with a rear dormer.

- Mansard conversion: Full rear slope rebuild to near-vertical; maximum space gain but highest cost. Typically £45,000–£70,000+.

Most loft conversions fall within permitted development, but properties in Conservation Areas, listed buildings, flats, and those where prior extensions have used PD allowances may require full planning permission.

Extensions: buyers pay for usable space

In the UK residential market, price per square metre is a key value driver. Adding usable floor area — particularly a kitchen-diner opening to the garden, or an additional reception room — tends to be valued directly by buyers. Returns are strongest where the extension fully complies with Building Regulations (structural, Part L thermal performance, Part P electrical, Approved Document F ventilation) and where the new space improves the property's flow and natural light rather than simply adding volume.

Single-storey rear extensions up to 3 metres (attached dwellings) or 4 metres (detached) can generally be built under permitted development. The Neighbour Consultation Scheme extends this to 6 metres (attached) or 8 metres (detached) subject to a 42-day notification period and no valid objection.

Energy efficiency: an increasingly important value driver

Proposed minimum EPC C requirements for private rented properties in England, preferential mortgage rates for EPC A/B homes, and rising energy costs mean that energy-efficiency credentials are increasingly influencing buyer and lender decisions.

Improvements with the most direct EPC impact include:

- Cavity wall or solid wall insulation (the most significant single measure for pre-1980 properties)

- Loft insulation (lowest cost and fastest payback)

- Upgrading to double or triple glazing through qualified window and door installers

- Heat pump installation replacing a gas boiler (significant capital cost but strong EPC benefit)

- Solar photovoltaic (PV) panels

Government grant schemes — including ECO4 and the Great British Insulation Scheme — may fund partial or full costs for eligible households. Check current eligibility on GOV.UK, as schemes and criteria change regularly.

Note: Major fabric improvements carry a moisture and condensation risk if not correctly specified. PAS 2035 is the UK standard for whole-house retrofit assessment; always use a qualified Retrofit Coordinator for significant fabric interventions.

Worked UK property scenario

Scenario: A 1930s three-bedroom semi-detached in a commuter town outside Bristol. Current value: approximately £290,000. Top of the comparable range on the street: approximately £375,000.

- A rear dormer loft conversion (estimated cost: £42,000) adding a fourth bedroom with en-suite could realistically push value to £325,000–£340,000 — a gross return of roughly 1.1× the cost invested.

- A single-storey kitchen extension (estimated cost: £35,000) creating an open-plan kitchen-diner with garden access could add £20,000–£35,000 in value.

- Both improvements combined (estimated total cost: £77,000) approach — but are unlikely to exceed — the neighbourhood price ceiling of approximately £375,000, making the combined uplift close to break-even before agent and legal fees.

This illustrates a key risk: the neighbourhood ceiling limits what any improvement can return, regardless of build quality.

What not to assume

- New kitchens always add value. A £30,000 kitchen in a £185,000 terraced house is unlikely to recover its cost — many buyers prefer to choose finishes themselves.

- Permitted development means no restrictions apply. PD rights have specific conditions on height, materials, setbacks from boundaries, and other factors. Properties in Conservation Areas, National Parks, Areas of Outstanding Natural Beauty, or subject to Article 4 directions may have most PD rights removed.

- An extension adds value proportional to what it cost. The premium depends on whether the new space matches buyer expectations, passes building control, and suits the property type and local market.

- EPC improvements deliver pound-for-pound value uplifts. Energy-efficiency work primarily improves saleability and reduces buyer negotiation leverage rather than lifting the headline asking price directly.

- Planning permission always adds value. Consent for an impractical or unwanted scheme adds little market value.

Improvements that rarely recoup full cost

- Swimming pools — high maintenance cost, not universally valued, reduce usable garden area

- Highly personalised interiors — bespoke murals, niche finishes, strongly themed rooms

- Uninsulated conservatories — often perceived as cold in winter and unusable in summer

- Over-specification of fixtures in a low-value property — quality that materially exceeds local market expectations

When to get professional help

Before committing to major spend, consider an independent assessment of likely value impact. Seek professional advice if:

- The planned works cost more than 10% of the property's current value

- You are unsure whether an improvement is feasible under planning or permitted development rules

- You want to understand how proposed works would affect your EPC rating and mortgage options

- You are planning to sell within 12 months and need to prioritise spend against likely return

How Housey can help

Housey can help you plan and execute improvements with the right professionals. Compare quotes from vetted extension builders, get expert input from energy-efficiency consultants on EPC-boosting upgrades, or request a valuation survey to establish a clear baseline before committing to your budget.

Frequently asked questions

Does a new roof add value to a property?

A new roof rarely adds value above its cost — but it prevents value loss. Buyers, mortgage lenders, and valuers will flag an end-of-life or failing roof, and it is commonly used as a negotiating point to reduce the agreed price. Replacing it before marketing removes a deduction rather than adding a premium.

Does a garden redesign add property value?

A tidy, well-maintained garden improves first impressions and buyer appeal, but full redesigns rarely recover their cost directly in monetary terms. Kerb appeal and functional outdoor space matter at the point of sale; high-specification landscaping generally does not pay back as a price uplift.

Should I get planning permission before making improvements?

For improvements requiring full planning permission, obtaining consent before sale is important — buyers and mortgage lenders generally require evidence of lawful permission for structural works. For works within permitted development rights, a Lawful Development Certificate from your local planning authority provides documentary confirmation and can simplify the conveyancing process.

Can home improvements affect my mortgage or remortgage?

A significant improvement that increases the property's value may allow you to remortgage at a better loan-to-value ratio once work is complete. Always inform your mortgage lender before starting major structural works — some policies require notification to maintain valid buildings insurance during construction.

Sources and further reading

- Permitted development rights for householders: technical guidance — GOV.UK

- Energy Performance Certificates — GOV.UK

- Great British Insulation Scheme — GOV.UK

- UK House Price Index reports — HM Land Registry

- PAS 2035: Retrofitting dwellings for improved energy efficiency — BSI Group

Useful next reads

Buying & Moving

Buying & MovingProperty Enhancement Strategies for a Successful Sale

Enhancing a UK property before listing typically involves improving kerb appeal, decluttering and neutralising décor, addressing minor maintenance issues, and investing in professional photography.

Buying & Moving

Buying & MovingHow to Get Your Property Professionally Valued

To get a professional property valuation in the UK, instruct a RICS Registered Valuer for any formal purpose — mortgage, probate, Help to Buy, or legal proceedings.

Buying & Moving

Buying & MovingExtending Your Property Lease: Increasing Value and Longevity

Qualifying leaseholders in England and Wales can extend their lease by 90 years at a peppercorn ground rent under the Leasehold Reform, Housing and Urban Development Act 1993.

Buying & Moving

Buying & MovingProperty Comparables: Using Market Data to Assess Home Value

Property comparables — known as 'comps' — are recently sold properties similar in size, type, tenure, and condition to the one being valued.

Buying & Moving

Buying & MovingHow Energy Performance Certificates Impact Property Value

A higher EPC rating can add measurable value to a UK property through a 'green premium' on open market sales, preferential green mortgage rates, and stronger buyer confidence.