Extending Your Property Lease: Increasing Value and Longevity

By Housey · Last reviewed 30th of May 2026

Extending Your Property Lease: Increasing Value and Longevity

Leasehold ownership is the norm for most UK flats, and the length of your remaining lease is one of the most financially significant numbers attached to your property. A lease that has slipped below 80 years — or is heading there — can make your home harder to mortgage, harder to sell, and lower at valuation. Understanding when and how to act is essential whether you are planning to sell, remortgage, or simply protect the value of your investment for the long term.

Key points

- Qualifying leaseholders in England and Wales have a statutory right under the Leasehold Reform, Housing and Urban Development Act 1993 to extend their lease by 90 years at a peppercorn (zero) ground rent.

- You must have owned the leasehold property for at least two years before you can use the statutory route.

- Once a lease falls below 80 years, a calculation known as marriage value applies — the leaseholder must pay the freeholder 50% of the increase in property value arising from the extension, which can add substantially to the premium.

- The formal statutory route begins with a Section 42 Notice served on the freeholder; a specialist solicitor should draft and serve this on your behalf.

- The Leasehold and Freehold Reform Act 2024 received Royal Assent and is being implemented in stages — some provisions affecting ground rent and the extension process may change, so check current GOV.UK guidance for the latest position.

How lease lengths affect your property

Most leasehold flats in England and Wales are sold on leases of 99, 125, or 999 years. Over time, that term reduces, and lenders and valuers pay close attention to it.

Many mainstream mortgage lenders require a minimum unexpired lease term — often 70 to 85 years at the time of application, and sometimes more depending on their own criteria. Some will not lend at all if fewer than 70 years remain. A property with a 68-year lease may be effectively unmortgageable, sharply reducing the pool of potential buyers and suppressing its market value.

Surveyors and valuers also factor lease length into their assessments. A short lease can translate directly into a reduced valuation figure, affecting both the price you achieve on sale and the equity available when you remortgage.

Statutory vs informal lease extension: which route suits you?

Leaseholders generally have two options: the formal statutory route under the 1993 Act, and an informal negotiated approach agreed directly with the freeholder.

Route | Best for | Not ideal for | Typical timescale | Main risk if wrong |

|---|---|---|---|---|

Statutory (Section 42 Notice) | Most qualifying leaseholders; provides legal certainty and a defined timetable | Those who have owned fewer than two years and cannot yet use this route | 6–12 months | Strict deadlines apply; missing the counter-notice window can be costly |

Informal negotiation | Cases where the freeholder is cooperative and a deal can be reached quickly; may suit newer owners ineligible for the statutory route | Freeholders who are unresponsive or demand an inflated premium | Weeks to months | No legal ceiling on premium; freeholder can withdraw at any point |

The statutory route gives the leaseholder more protection. The process follows a defined timetable, and if the parties cannot agree on a premium, either side can apply to the First-tier Tribunal (Property Chamber) to determine a fair price. The informal route can be faster and cheaper when both sides are motivated, but without the 1993 Act's protections, the freeholder has no obligation to agree or to price the premium reasonably.

Understanding the lease extension premium

The premium you pay to extend your lease is calculated using a formula that accounts for:

- The ground rent the freeholder gives up over the extended term.

- The deferment of the reversion — what the property will be worth when the current lease expires.

- Marriage value — applicable only when fewer than 80 years remain. The leaseholder must share 50% of the increase in property value arising from the extension with the freeholder.

Marriage value can add substantially to the cost. A flat with 79 years remaining may cost noticeably more to extend than the same flat with 81 years remaining. Acting before the lease drops below 80 years is one of the most financially significant decisions a leaseholder can make.

Indicative cost guidance: lease extension premiums vary enormously by property value, location, lease length, and ground rent terms. As an illustration only, extending a lease on a flat worth £250,000 with 85 years remaining might attract a premium in the range of £5,000–£15,000, but a similar flat with 65 years remaining could face a premium several times higher. Always obtain a specialist lease extension valuation before proceeding — figures here are illustrative only (last reviewed 2026-05-30; source: Leasehold Advisory Service).

The statutory process step by step

- Check your eligibility. You must have been the registered owner for at least two years. The property must be a qualifying flat — generally a residential long lease, not a commercial property or house.

- Instruct a specialist solicitor and a RICS-accredited valuer. The valuer will assess the likely premium range; the solicitor will prepare and serve the Section 42 Notice.

- Section 42 Notice served. This formal notice is sent to the freeholder setting out the premium you propose. The freeholder has two months to respond with a counter-notice.

- Negotiation. Both parties negotiate within the statutory timetable. Many cases settle without going to tribunal.

- Tribunal if needed. Either party can apply to the First-tier Tribunal (Property Chamber) if agreement is not reached within the prescribed period.

- Completion. Once terms are agreed, your conveyancing solicitor handles the legal documentation and the new lease is registered at HM Land Registry.

Homeowner checklist before starting

Important limitations

This article provides general information about the lease extension process in England and Wales only. Lease extension law is complex, and the right strategy — including whether to use the statutory or informal route and the likely premium — depends on your specific property, lease terms, freeholder, and current legislation. The Leasehold and Freehold Reform Act 2024 is being implemented in stages and certain rules may change. Nothing in this article constitutes legal advice. Always take advice from a qualified solicitor and a RICS-accredited valuer before serving any notices or agreeing any terms with a freeholder.

What to ask a qualified professional

Before instructing a solicitor or valuer for a lease extension, consider asking:

- What is the likely premium range for my specific property and lease, and how confident are you in that estimate?

- What are the practical differences between the informal and statutory routes given my freeholder's profile?

- Are there any aspects of my existing lease — ground rent terms, restrictions, or covenants — that could complicate the extension or increase the cost?

- What is your experience with lease extension cases, including appearances before the First-tier Tribunal (Property Chamber)?

- How are your fees structured — fixed fee or hourly — and what does your quote include?

- How long do you expect the process to take, and what factors could cause delays?

When to get professional help

Always instruct a specialist solicitor and a RICS-accredited valuer for a lease extension — this is not a process to navigate alone. Seek professional help without delay if:

- Your lease is approaching or already below 80 years (marriage value territory).

- You are planning to sell within the next 12 months and your lease is below 85 years.

- You are about to remortgage and your lender has raised concerns about lease length.

- Your freeholder is unresponsive or has quoted a premium that seems very high.

- You have received any formal correspondence from your freeholder relating to the lease.

How Housey can help

Housey connects leaseholders with specialists who understand every stage of the lease extension process. Whether you need a lease extension valuation to understand the likely premium, a conveyancing solicitor to serve your Section 42 Notice and manage the legal process, or a broader valuation survey for a fuller picture of your property's condition and value, Housey can help you find qualified local professionals and compare quotes before you commit.

Frequently asked questions

What happens if I ignore a short lease?

If you take no action, the lease term continues to shorten. Below 80 years, extension costs rise significantly due to marriage value. Below around 70 years, many lenders will not offer a mortgage, making the property very difficult to sell and potentially reducing its market value substantially. Addressing a short lease sooner is almost always more cost-effective.

Can I sell a leasehold flat with a short lease?

Yes, but a short lease — typically below 70–80 years — limits your buyer pool to cash purchasers and can suppress the sale price. Some sellers extend before marketing; others assign the right to extend to the buyer at an agreed price reduction. A specialist solicitor can advise on which approach best suits your situation and timescale.

How long does a lease extension take?

The statutory route typically takes 6–12 months, though it can be shorter if both parties agree quickly or longer if the case goes to the First-tier Tribunal (Property Chamber). The informal route can be concluded in weeks when the freeholder cooperates, but there is no statutory timetable to keep negotiations moving if they stall.

What is marriage value and why does it matter?

Marriage value is the increase in combined property value arising from a lease extension. Under the Leasehold Reform, Housing and Urban Development Act 1993, once a lease falls below 80 years, the leaseholder must share 50% of this uplift with the freeholder as part of the extension premium. This can substantially increase the cost of extension, which is why the 80-year threshold is so financially significant.

Sources and further reading

- Lease extension — getting it right — Leasehold Advisory Service (LEASE)

- Extending a lease — GOV.UK

- Leasehold Reform, Housing and Urban Development Act 1993 — legislation.gov.uk

- Leasehold and Freehold Reform Act 2024 — legislation.gov.uk

Useful next reads

Buying & Moving

Buying & MovingExtending Your Lease: Process, Costs, and Timing

Qualifying leaseholders in England and Wales have a statutory right to extend their lease by 90 years at a peppercorn (nil) ground rent under the Leasehold Reform, Housing and Urban Development Act 1993, provided they have owned for at least two years.

Buying & Moving

Buying & MovingWhich Home Improvements Add Real Value to Your Property?

In the UK, loft conversions, single and double-storey extensions, and energy-efficiency upgrades are most reliably linked to added property value.

Buying & Moving

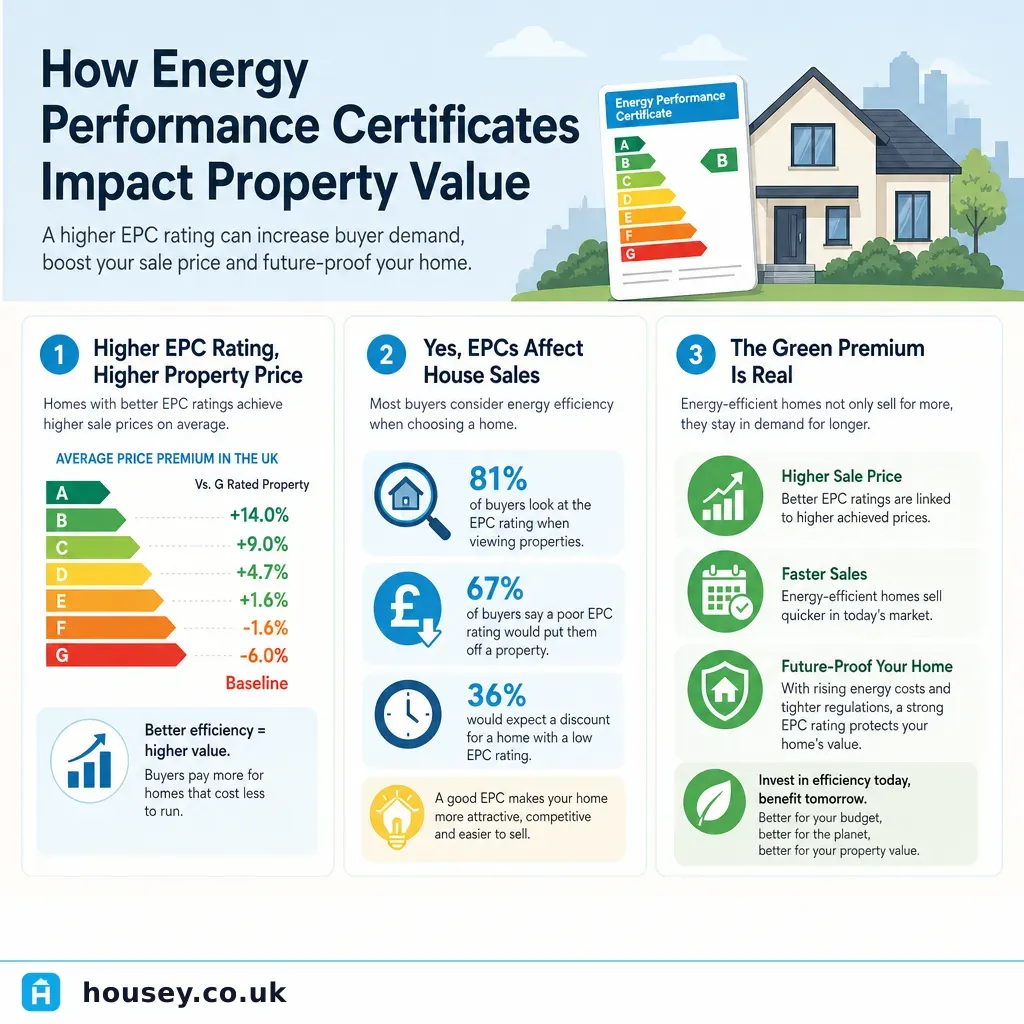

Buying & MovingHow Energy Performance Certificates Impact Property Value

A higher EPC rating can add measurable value to a UK property through a 'green premium' on open market sales, preferential green mortgage rates, and stronger buyer confidence.

Buying & Moving

Buying & MovingAdding Value to a New-Build Property

Adding value to a new-build typically means differentiating your home from identical plots, securing a sound baseline through a professional snagging survey, and making targeted improvements — landscaping, EV charging, or structural upgrades chosen at build stage.

Buying & Moving

Buying & MovingBuy-to-Let Property Investment: Essential Guidance for Landlords

Buy-to-let investment in the UK requires careful financial planning.