Property Comparables: Using Market Data to Assess Home Value

By Housey · Last reviewed 11th of May 2026

Property Comparables: Using Market Data to Assess Home Value

Understanding how professional valuers assess property prices is more useful than many buyers and sellers realise. Comparable evidence — sold prices for similar nearby homes — underpins almost every residential valuation in England and Wales, from estate agent appraisals to RICS Red Book mortgage valuations. Getting to grips with this data before making or accepting an offer gives you a factual basis for negotiation rather than relying on instinct or asking prices alone.

Key points

- HM Land Registry publishes all residential sold prices in England and Wales; the Price Paid Data is updated monthly and freely searchable at landregistry.data.gov.uk.

- A valid comparable is typically within 0.25 miles, sold within the past 12 months, and of similar size (within approximately 10%), property type, and tenure (freehold or leasehold).

- RICS Red Book valuations (RICS Valuation – Global Standards) used for mortgage purposes require at least three comparable sales; lenders instruct the valuer independently of the buyer or seller.

- Leasehold properties with fewer than 80 years remaining on the lease carry a material value discount, because many mortgage lenders will not lend on short leases.

- Automated valuation models (AVMs) used by property portals carry margins of error of ±10–20%; they do not replace a RICS-registered surveyor's assessment.

What are property comparables and why do they matter?

Property comparables (commonly called "comps") are recently sold properties that share key characteristics with the home being assessed. They form the backbone of almost every professional valuation in England and Wales: mortgage valuers, RICS-registered surveyors, and estate agents all rely on comparable evidence to support their figures.

For buyers, reviewing comps before making an offer helps guard against paying above market value. For sellers, comparable evidence provides a check on whether an agent's asking price is realistic or inflated to win the instruction. For homeowners remortgaging or pursuing a lease extension, comparable analysis may directly affect the negotiated outcome.

The UK's open access to Land Registry sold-price data makes self-researched comparable analysis more accessible than in many countries — but interpreting the data accurately requires knowing which adjustments are appropriate.

Where to find reliable comparable data in the UK

Several sources provide sold-price information in England and Wales:

Source | What it shows | Cost | Key limitation |

|---|---|---|---|

HM Land Registry Price Paid Data | All residential sales by address and date | Free | 2–3 month reporting lag; no floor area |

UK House Price Index (GOV.UK) | Area-level average prices by property type | Free | Aggregated — not property-specific |

Rightmove / Zoopla sold prices | Land Registry data with listing photos | Free | Useful for condition context; prices unadjusted |

EPC Register (MHCLG) | Floor area, energy rating, construction type | Free | Data quality varies; not all properties covered |

HM Land Registry Title Register | Tenure, title charges, covenants | £3 per register | Requires a separate lookup per property |

RICS-instructed valuation | Red Book valuation with comparable analysis | £150–£500+ indicative | Lender-instructed for mortgage purposes |

Scotland uses the Registers of Scotland; Northern Ireland uses Land and Property Services.

How to select and adjust comparables

Choosing comparables is not simply a matter of finding the nearest recent sales. Each comparable needs to be weighed against the subject property for meaningful differences. RICS guidance and standard surveying practice typically require at least three comparable sales meeting the following criteria:

- Location: within 0.25 miles in urban areas; up to 2–5 miles in rural areas with low transaction volumes.

- Recency: sold within the past 12 months; within 6 months in active markets. Older sales may be adjusted for intervening market movement.

- Property type: like-for-like comparisons (terraced to terraced, flat to flat). Cross-type comparisons require significant adjustment and carry greater uncertainty.

- Tenure: freehold versus leasehold. A leasehold flat with 75 years remaining is not directly comparable to one with 120 years remaining.

- Size: within approximately 10% of gross internal floor area. EPC records include floor area data for many UK properties.

- Condition: a recently refurbished property is not directly comparable to one requiring full renovation without material adjustment.

Worked UK property scenario

A buyer is considering a 1970s semi-detached house in a market town in the East Midlands, listed at £285,000. They pull three comparables from HM Land Registry data:

- Comp A: Same road, near-identical semi, sold four months ago at £272,500 — EPC records note the central heating needs updating.

- Comp B: Adjacent road, slightly smaller semi (approximately 8% less floor area), sold eight months ago at £265,000 — recently renovated kitchen and bathroom.

- Comp C: Parallel road, larger semi with a single-storey rear extension, sold six months ago at £310,000.

The unadjusted range is £265,000–£310,000. Adjusting for the extension on Comp C (typically a £15,000–£25,000 premium for a modest single-storey addition), the adjusted upper end is approximately £285,000–£295,000. The asking price of £285,000 sits within a defensible range, provided the subject property is in comparable or better condition to Comp A. This analysis does not replace a professional RICS valuation, but gives the buyer a structured basis for negotiation.

What not to assume when using comparables

Common misunderstandings lead buyers and sellers to misinterpret the data:

- Asking prices are not comparables. Only completed sales registered at HM Land Registry count as comparable evidence.

- New builds are rarely useful comparables for second-hand properties. Developer incentives, part-exchange, and historic Help to Buy usage distort new-build prices in ways that do not apply to the resale market.

- Automated valuation models are not mortgage valuations. Portal price estimates carry significant margins of error; lenders require an independent RICS-registered valuer.

- A higher nearby sale does not automatically mean your property is worth the same. Size, condition, orientation, floor level (for flats), and tenure all independently affect value.

- A "sale agreed" status is not a completed transaction. Only a registered Land Registry entry confirms legal completion.

Important limitations

This article provides general guidance on using publicly available property data. Property valuation is a regulated activity: formal valuations for mortgage, probate, insurance, or tax purposes must be carried out by a RICS-registered valuer under RICS Valuation – Global Standards (the Red Book). Self-researched comparable analysis cannot account for all the factors a qualified valuer considers, including property-specific defects, tenure complexity, and local market conditions at the date of valuation.

This article does not constitute a property valuation and should not be used as a substitute for professional advice.

What to ask a qualified professional

If you are instructing a valuer or challenging an existing valuation, consider asking:

- Which comparable sales did you rely on, and can I see the comparable evidence?

- How have you adjusted for differences in size, condition, and tenure between the comparables and this property?

- How recent is the comparable evidence, and does it reflect current market conditions?

- What is the range of comparable evidence, and where does this property sit within that range?

- If the property is leasehold, how has the lease length and ground rent structure affected your assessment?

- If your figure is below the agreed purchase price, what specific evidence supports the shortfall?

When to get professional help

Self-researched comparables are useful for informal negotiation, but a qualified professional is needed when:

- You are applying for a mortgage and require a lender-acceptable RICS valuation.

- You are purchasing a leasehold property and need to understand how lease length affects value.

- You are involved in a contested valuation — probate, matrimonial proceedings, or compulsory purchase.

- You wish to challenge a mortgage lender's down-valuation.

- The property has unusual features (listed building, non-standard construction, significant defects, or a commercial element) that make standard comparable analysis unreliable.

How Housey can help

If your comparable research raises questions about an asking price, or you want a documented professional opinion of value, Housey connects you with RICS-registered surveyors offering valuation surveys across the UK. A formal valuation provides structured comparable analysis and a defensible figure you can use in negotiation or present to a lender.

Frequently asked questions

How many comparables do I need to value a property?

RICS Red Book guidance requires a minimum of three comparable sales for a formal valuation. For informal purposes, three to six local comps sold within the past 12 months provide a reasonable evidence base. Using fewer than three risks the analysis being distorted by outliers or unusual transactions.

Can I use Rightmove or Zoopla sold prices as comparables?

Yes, as a starting point. Both aggregate HM Land Registry data and display it alongside listing photographs, which helps assess condition. However, the data carries a 2–3 month reporting lag, does not always include floor area, and cannot replace the adjustments a qualified valuer would apply.

What if there are very few comparable sales in my area?

In areas with low transaction volumes — rural locations or unusual property types — valuers expand the search radius, extend the time period, and apply larger adjustments. The range of uncertainty is wider in these cases, and the case for instructing a professional valuer is correspondingly stronger.

Do comparables work the same way for leasehold flats?

No. Leasehold flats require additional analysis of lease length, service charge, and ground rent structure. A lease below 80 years materially reduces value because many mortgage lenders will not lend on short leases. Comparable evidence for flats should ideally reflect similar lease lengths to be meaningful.

Sources and further reading

- HM Land Registry Price Paid Data — GOV.UK

- UK House Price Index — GOV.UK / HM Land Registry

- RICS Valuation – Global Standards (Red Book) — RICS

- Find an energy certificate — floor area and energy data — GOV.UK / MHCLG

- Registers of Scotland — property sales data — Registers of Scotland

Useful next reads

Buying & Moving

Buying & MovingHow to Get Your Property Professionally Valued

To get a professional property valuation in the UK, instruct a RICS Registered Valuer for any formal purpose — mortgage, probate, Help to Buy, or legal proceedings.

Buying & Moving

Buying & MovingWhich Home Improvements Add Real Value to Your Property?

In the UK, loft conversions, single and double-storey extensions, and energy-efficiency upgrades are most reliably linked to added property value.

Buying & Moving

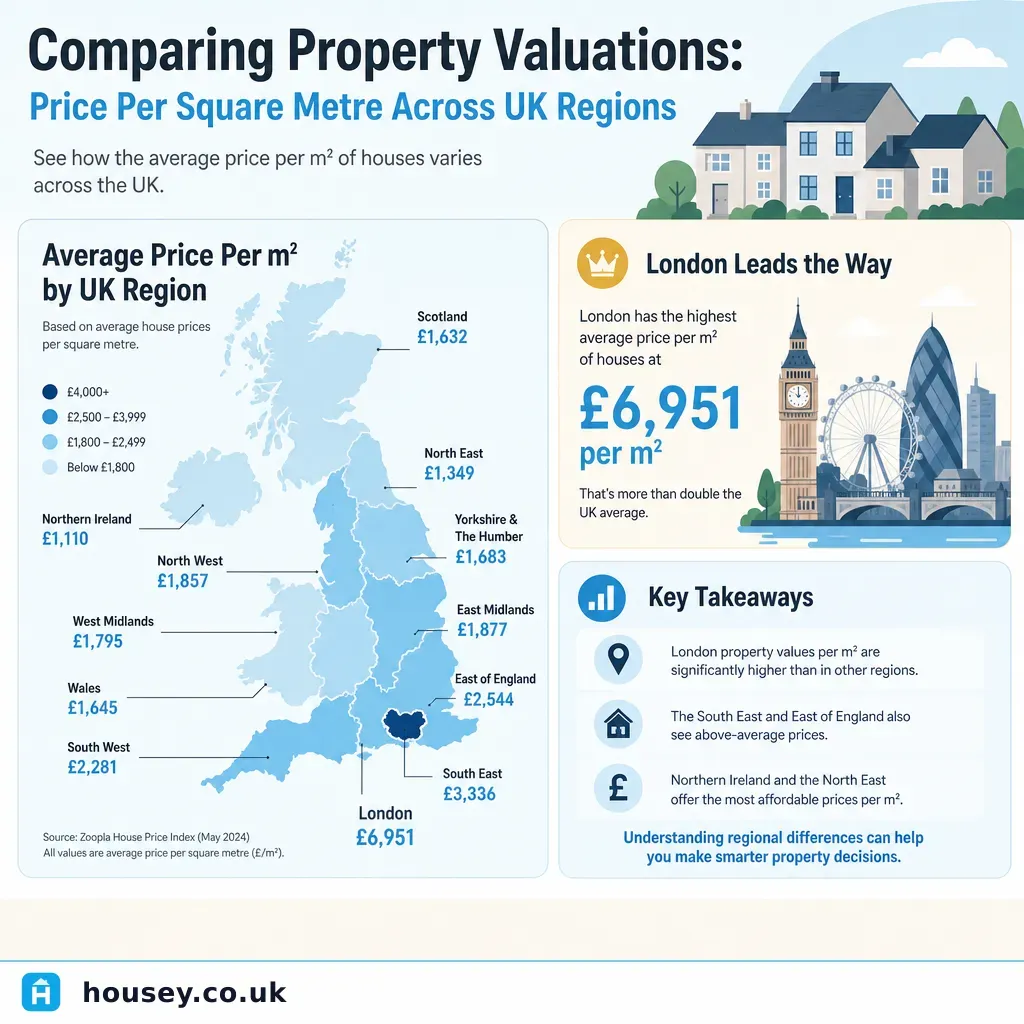

Buying & MovingComparing Property Valuations: Price Per Square Metre Across UK Regions

Property prices per square metre vary dramatically across UK regions.

Buying & Moving

Buying & MovingDetermining Your Property's Market Value: Valuation Guide for Sellers

Market value in the UK is most reliably established by combining estate agent appraisals with your own analysis of recent sold prices on the HM Land Registry database.

Buying & Moving

Buying & MovingUnderstanding Property Valuations: Process, Purpose, and Professional Assessment

A property valuation is a professional opinion of a property's market value, carried out by a RICS Registered Valuer after a physical inspection and comparable sales analysis.