Buy-to-Let Property Investment: Essential Guidance for Landlords

By Housey · Last reviewed 25th of May 2026

Buy-to-Let Property Investment: Essential Guidance for Landlords

Purchasing a buy-to-let property sits at the intersection of property law, tax planning, and landlord regulation — three areas that have each shifted significantly since 2015. The question arises most often for first-time investors considering their initial rental purchase, for existing homeowners looking to retain a previous property after moving, and for portfolio holders assessing whether to expand. What is at stake is not just rental income, but a set of statutory obligations and financial exposures that now affect net returns more materially than at any earlier point in the modern buy-to-let market.

Key points

- The Stamp Duty Land Tax (SDLT) surcharge on additional residential properties in England rose to 5% from 31 October 2024; Scotland's Additional Dwelling Supplement under LBTT is 6%, and Wales uses Land Transaction Tax with its own higher residential rates.

- Individual landlords can no longer deduct mortgage interest from rental income as a business expense; they instead receive a 20% tax credit under rules introduced by Section 24 of the Finance (No. 2) Act 2015, fully in force since April 2020.

- Rental properties in England and Wales must hold a valid Energy Performance Certificate (EPC) rated E or above before a new or renewed tenancy can be granted; proposals to raise the minimum to EPC band C by 2030 are under ongoing consultation.

- Landlords must arrange an annual gas safety check by a Gas Safe registered engineer and provide each tenant with a current Landlord Gas Safety Record before occupancy for new tenancies, or within 28 days of each annual check.

- Rental income above £1,000 per year must be declared to HMRC via Self Assessment, with Income Tax charged at the landlord's marginal rate after allowable expenses.

What does buy-to-let actually cost to enter?

The upfront cost of a buy-to-let purchase exceeds that of a primary residence. SDLT is charged at standard residential rates plus the 5% surcharge on every band for additional properties in England. On a £250,000 investment property the SDLT bill alone could reach approximately £11,250 — verify your exact position using the GOV.UK SDLT calculator.

Beyond SDLT, buyers should budget for mortgage arrangement fees (often £999–£2,500), a lender's valuation, conveyancing costs, and any immediate works needed to reach lettable standard.

Indicative UK costs, last reviewed 2026-05-25. Costs vary significantly by property type, location, lender, and solicitor.

Cost category | Indicative range | Notes |

|---|---|---|

SDLT additional dwelling surcharge (England) | 5% on each band | Different rates apply in Scotland and Wales |

BTL mortgage arrangement fee | £999–£2,500 | Fee-free products available at higher rates |

Conveyancing | £1,000–£2,000 | Includes searches, Land Registry, disbursements |

Lender's valuation | £200–£600 | Separate from any buyer's survey |

Landlord buildings insurance (annual) | £200–£600 | Varies by property value and location |

How buy-to-let mortgage finance works

Buy-to-let lenders typically apply a rental income stress test, requiring projected rent to cover 125–145% of the monthly payment calculated at a notional rate of around 5.5–6%, regardless of the actual product rate. Most require a minimum deposit of 25%.

Purchasing through a limited company has become more common since Section 24 removed full mortgage interest relief for individuals. Companies can still deduct mortgage interest as a business expense, but pay corporation tax on profits and dividend tax on extraction. The right structure depends on individual tax circumstances.

Ownership structure | Tax on rental profit | Mortgage interest treatment | Best suited to |

|---|---|---|---|

Individual (basic-rate taxpayer) | Income Tax at 20% | 20% tax credit only | Smaller portfolios, lower earners |

Individual (higher-rate taxpayer) | Income Tax at 40–45% | 20% tax credit — less efficient | Larger portfolios; seek specialist advice |

Limited company | Corporation Tax (25% main rate) | Fully deductible | Higher earners, portfolio builders |

Consult a qualified accountant or tax adviser before deciding on ownership structure.

Legal obligations before your first tenancy

Landlords in England must meet the following statutory requirements before any tenancy begins. Failure can result in civil penalties, criminal prosecution, or the inability to serve a Section 21 notice.

- Gas safety: Annual Gas Safe check; Landlord Gas Safety Record provided to tenants before occupancy or within 28 days of each check.

- Electrical safety: Electrical Installation Condition Report (EICR) every five years in England; provided to new tenants before they move in.

- EPC: Valid EPC rated E or above required before marketing or letting; F and G-rated properties cannot legally be let in most circumstances.

- Smoke and CO alarms: At least one smoke alarm per occupied storey; CO alarm in every room with a fixed combustion appliance (excluding gas cookers), under the Smoke and Carbon Monoxide Alarm (Amendment) Regulations 2022.

- Deposit protection: Registered in a government-approved scheme (DPS, MyDeposits, or TDS) within 30 days of receipt.

- Right to Rent: All adult occupiers must be verified before the tenancy starts.

Local authority selective, additional, or mandatory licensing schemes may add further obligations. Houses in Multiple Occupation (HMOs) require a specific licence before any occupancy.

Choosing the right property and calculating yield

- Gross yield = (Annual rent ÷ Purchase price) × 100

- Net yield subtracts void periods, management fees, maintenance, insurance, compliance costs, and financing. Typically 1–2 percentage points below gross, and the only figure that matters for cash-flow purposes.

A gross yield of 5–7% is often cited as reasonable in many UK regional markets. Yields significantly above this may reflect higher tenant turnover risk or more limited capital growth. Obtain written rental comparables from a local letting agent and cross-reference with the Valuation Office Agency's private rental statistics.

Homeowner pre-purchase checklist: buy-to-let

Red flags when considering a buy-to-let purchase

- Short lease on a leasehold flat — fewer than 80 years remaining makes extension costly (marriage value applies) and the property potentially unmortgageable for future buyers.

- EPC below E with no clear upgrade path — the property cannot legally be let until it meets the minimum standard.

- HMO non-compliance or unresolved licensing history — check planning and licensing records with the local authority.

- Large upcoming service charges or major works notices — cladding remediation or roof works on a leasehold flat can destroy projected yield.

- Structural defects or significant damp found in the survey — may affect insurability, refinancing, and future saleability.

Important limitations

This article provides general information only. Buy-to-let investment involves financial, legal, regulatory, and tax obligations that vary by property type, tenure, local authority area, and individual circumstances. Rules on SDLT, income tax, energy standards, and licensing are subject to change. Nothing here constitutes financial, tax, legal, or regulated mortgage advice. Always consult a qualified tax adviser, solicitor, and FCA-authorised mortgage broker before any purchase decision.

What to ask a qualified professional

Solicitor or conveyancer:

- Does the title or lease restrict or condition letting in any way?

- Are there outstanding charges, covenants, or licensing obligations?

- Is this property in a selective, additional, or mandatory HMO licensing area?

FCA-regulated mortgage broker:

- What stress-test rate and interest coverage ratio does this lender apply?

- Is a limited company purchase more tax-efficient given my income?

- What minimum EPC rating does this lender require for a buy-to-let product?

Accountant or tax adviser:

- Should I purchase personally or through a limited company?

- What allowable expenses can I offset against rental income under current HMRC rules?

- How will this purchase affect my Self Assessment position?

When to get professional help

Always instruct qualified professionals before exchanging contracts. Seek specialist advice if:

- The lease has fewer than 90 years remaining

- The survey identifies structural movement, serious damp, or fire safety concerns

- Significant works are needed to reach EPC band E

- You are considering an HMO conversion

- You are uncertain whether to purchase personally or through a company

How Housey can help

Housey connects you with experienced professionals at the two most critical stages of a buy-to-let purchase. Book a valuation survey to confirm the property's market value before you commit, and use our conveyancing service to find a solicitor with landlord transaction experience who can review the title, lease terms, and any licensing obligations before exchange.

Frequently asked questions

Do I need a special mortgage to let a property?

Yes. If you intend to let a property, you must inform your lender and typically need a buy-to-let mortgage. Letting on a standard residential mortgage without consent is a breach of your mortgage conditions and could result in the lender demanding immediate repayment of the outstanding balance.

Can I manage a buy-to-let property myself without a letting agent?

Yes. Self-management is legal and can improve net yield, but you remain personally responsible for all statutory compliance — gas safety checks, EICR, deposit protection, Right to Rent checks, and tenancy documentation. Many first-time landlords underestimate the time, knowledge, and availability this requires.

What happens to my buy-to-let if it sits empty between tenancies?

Void periods reduce net yield directly. You remain liable for council tax during vacant periods and buildings insurance must cover vacancy, though some policies restrict cover after 30 to 60 days. Always check your policy wording and notify your insurer when the property becomes vacant.

Is buy-to-let still a worthwhile investment in 2026?

Profitability depends on local rental demand, purchase price, financing costs, and compliance spending. Higher SDLT surcharges, the removal of full mortgage interest relief for individuals, and rising EPC standards have reduced net returns for many investors. A detailed cash-flow analysis using realistic net yield — not just gross yield — is essential before committing.

Sources and further reading

- Stamp Duty Land Tax: residential property rates — GOV.UK

- Tax relief for residential landlords: how it's worked out — GOV.UK / HMRC

- Gas safety: a guide for landlords — Health and Safety Executive

- Electrical safety standards in the private rented sector — GOV.UK

- Domestic private rented property: minimum energy efficiency standard — GOV.UK

- Smoke and Carbon Monoxide Alarm (Amendment) Regulations 2022 — legislation.gov.uk

Useful next reads

Buying & Moving

Buying & MovingEssential Guidance for Property Landlords and Investors

UK landlords must hold valid gas safety records, electrical installation condition reports, and energy performance certificates before letting a property.

Buying & Moving

Buying & MovingExtending Your Property Lease: Increasing Value and Longevity

Qualifying leaseholders in England and Wales can extend their lease by 90 years at a peppercorn ground rent under the Leasehold Reform, Housing and Urban Development Act 1993.

Buying & Moving

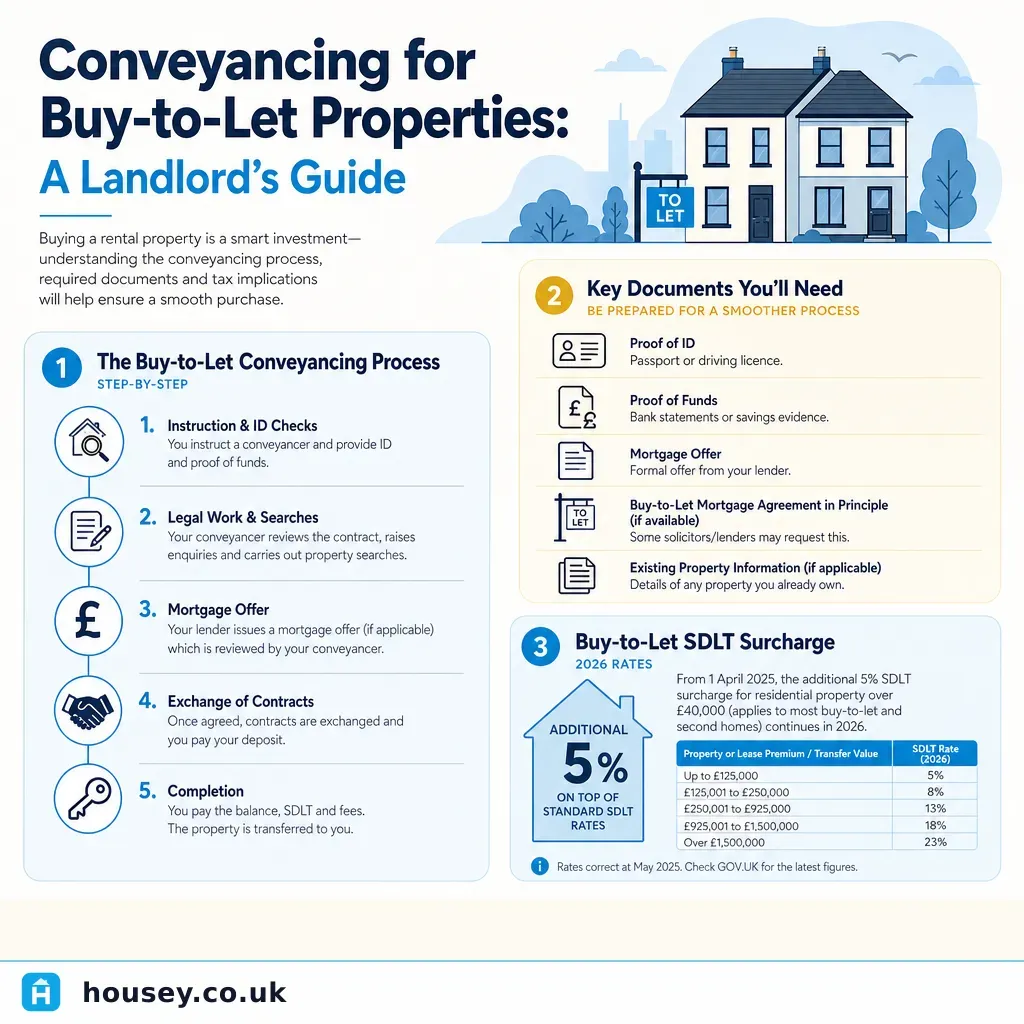

Buying & MovingConveyancing for Buy-to-Let Properties: A Landlord's Guide

Buy-to-let conveyancing follows the same legal process as any residential purchase but adds several layers: a 5% SDLT additional dwelling surcharge in England, review of any existing tenancy agreements, checking local authority licensing requirements, and ensuring buy-to-let mortgage conditions are correctly recorded.

Buying & Moving

Buying & MovingProperty Investment Sentiment: Understanding Market Appetite for UK Real Estate

UK property investment sentiment is shaped by interest rates, rental yields, regional supply and demand, and policy changes such as stamp duty surcharges and landlord tax rules.

Buying & Moving

Buying & MovingFirst-Time Buyer vs Established Homeowner: Property Purchase Considerations

First-time buyers in England pay no stamp duty on the first £300,000 of a property worth up to £500,000 and may access specific mortgage products.