Conveyancing for Buy-to-Let Properties: A Landlord's Guide

By Housey · Last reviewed 25th of May 2026

Conveyancing for Buy-to-Let Properties: A Landlord's Guide

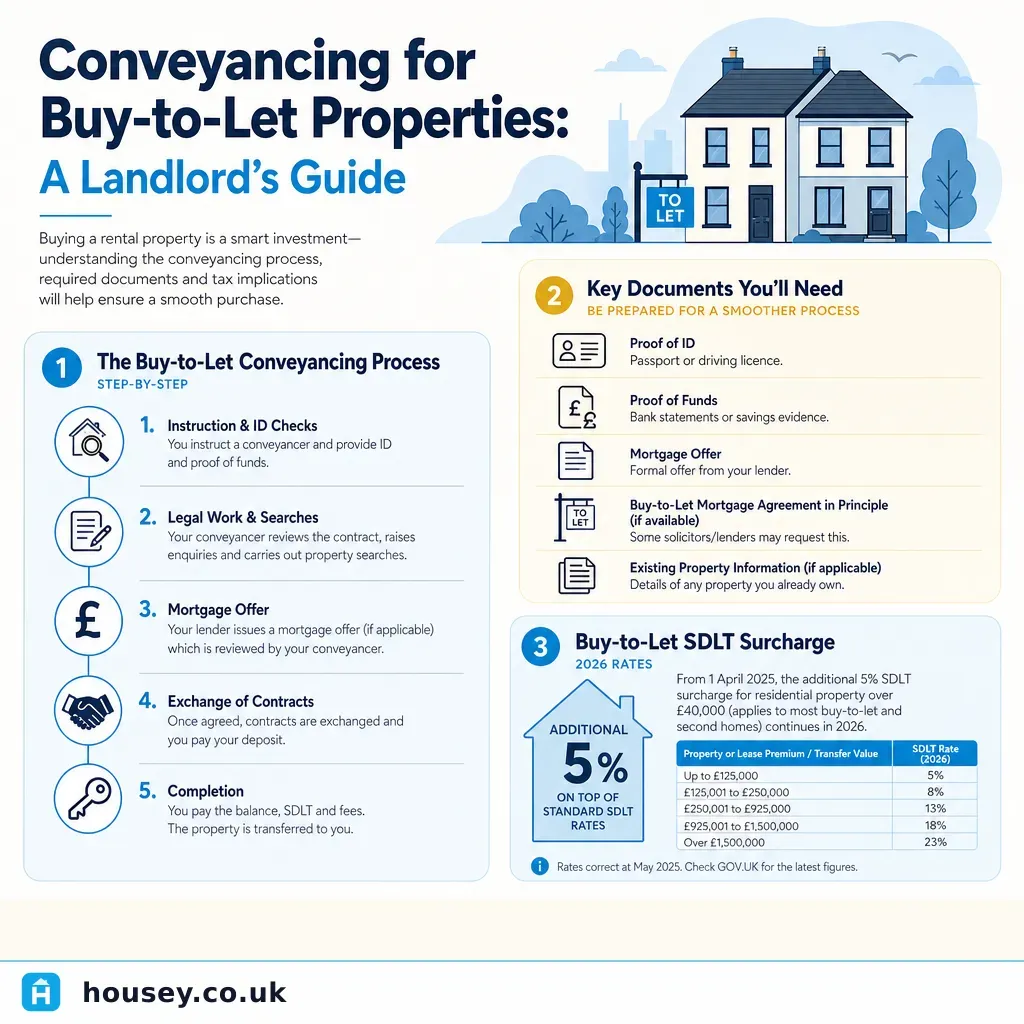

Buying a residential investment property in the UK involves the same fundamental legal process as purchasing a home to live in, but with additional layers that a solicitor or licensed conveyancer must address carefully. Stamp duty surcharges, existing tenancy agreements, local authority licensing obligations, and buy-to-let mortgage conditions all require specific attention during the conveyancing process. Understanding what your conveyancer needs — and what checks they will carry out — helps you avoid delays and unexpected costs.

Key points

- The additional dwelling surcharge for buy-to-let purchases in England is 5% on top of standard SDLT rates (effective from 31 October 2024), payable within 14 days of completion.

- If you purchase a property with an existing assured shorthold tenancy (AST) in place, the tenancy is inherited by you on completion — your solicitor must review the AST terms before exchange.

- Buy-to-let mortgage offers contain specific conditions — minimum rental yield ratios, tenant type restrictions, and HMO exclusions — that must be disclosed and correctly noted during conveyancing.

- Mandatory HMO licensing in England applies to properties occupied by 5 or more people from 2 or more separate households; the local authority must be checked before purchase.

- Rental properties in England and Wales must hold a minimum EPC rating of E to be lawfully let; proposed Government changes may raise this minimum to C in future.

Important limitations

This article provides general information about the conveyancing process for buy-to-let properties in England and Wales. It is not legal advice. SDLT rates, local authority licensing requirements, tenancy law, and EPC obligations can change and vary significantly by property type and location. Always instruct a qualified solicitor or licensed conveyancer for any property purchase. The information reflects rules as at 2026-05-25.

How buy-to-let conveyancing differs from residential conveyancing

The legal steps — receiving search results, raising pre-contract enquiries, exchanging contracts, and completing — are the same as any residential transaction. However, a buy-to-let buyer's conveyancer must address several additional elements:

Element | Standard residential | Buy-to-let additional requirements |

|---|---|---|

Stamp Duty (SDLT) | Standard rates apply | 5% additional dwelling surcharge in England (from 31 Oct 2024); Land Transaction Tax in Wales; LBTT Additional Dwelling Supplement in Scotland |

Mortgage conditions | Standard residential lender terms | Buy-to-let lender conditions: rental cover ratio, tenant type restrictions, HMO exclusions |

Existing tenancy | Not applicable | Review AST terms; confirm assignment rights and deposit transfer obligations on completion |

Local authority licensing | Not applicable | Check mandatory, additional, and selective licensing requirements before exchange |

EPC | Standard disclosure | Minimum E rating required for lawful letting in England and Wales |

Building Safety Act 2022 | Standard checks | Additional landlord obligations for qualifying higher-risk buildings above 18 metres |

Documents your conveyancer will need

Preparing documentation in advance can significantly speed up the transaction. Your conveyancer is likely to request the following.

From you (the buyer):

- Proof of identity and current address (passport and recent utility bill or bank statement)

- Source of funds evidence — bank statements, mortgage offer, or gifted deposit letter if applicable

- Your buy-to-let mortgage offer in full

- Details of all other properties you own (relevant to the SDLT surcharge calculation)

From the seller (via their solicitor):

- Title documents and official copies from HM Land Registry

- Existing tenancy agreement(s) if the property is currently occupied

- Tenancy deposit scheme certificate and prescribed information (where tenants are in situ)

- Current gas safety record (if tenants are in occupation at the time of sale)

- Energy Performance Certificate

- Any local authority licensing documentation

- Details of any managing agents and the scope of their authority

- For flats: lease, service charge accounts, and relevant building safety documentation

Buying with a sitting tenant: key legal points

Purchasing a tenanted property — where an AST is already in place — introduces specific obligations that your conveyancer must address before and on completion:

- You inherit the existing tenancy on completion, becoming the new landlord automatically. The tenant does not need to sign a new agreement unless both parties agree to vary the terms.

- The tenancy deposit must be transferred to you or your letting agent and re-protected in a Government-approved scheme within 30 days of completion. Failure to re-protect correctly can prevent you from serving a valid section 21 notice.

- Any outstanding repairs, safety hazards, or unresolved issues noted in the seller's disclosures should be negotiated before exchange of contracts.

- If the seller has served a section 21 or section 8 notice before completion, your solicitor should confirm its validity and the likely timeline to vacant possession.

When this becomes urgent

Seek immediate professional advice if:

- You have already completed a purchase and then discover the property is in a selective licensing zone — operating without a licence is a criminal offence carrying fines of up to £30,000.

- The seller or agent is pressing you to proceed without providing or disclosing the full tenancy documentation — this is a serious red flag and should halt the transaction.

- There is any doubt about whether the tenant's deposit was protected in a Government-approved scheme and whether the prescribed information was correctly served before you took ownership.

- The property is above 18 metres and subject to the Building Safety Act 2022 — specific new landlord obligations apply that your conveyancer must verify.

What to ask a qualified professional

Before instructing a conveyancer for a buy-to-let purchase, ask:

- Do you have recent experience with buy-to-let conveyancing in this local authority area?

- Will you check whether the property is subject to mandatory, additional, or selective licensing requirements before exchange?

- How will you handle the transfer and re-protection of the tenancy deposit on completion?

- Can you advise on the SDLT position for my specific circumstances, including whether any relief applies?

- If the property is a leasehold flat, will you check the lease for any restrictions on short-term letting or sub-letting?

- What are your total fees, and does the quote include SDLT, Land Registry fees, and search costs?

When to get professional help

Buy-to-let conveyancing should always be handled by a qualified solicitor or licensed conveyancer. Specialist advice is particularly important if:

- The property is subject to a non-standard tenancy — a commercial tenancy, a licence to occupy, or a regulated tenancy under the Rent Act 1977 carries very different legal protections and requires careful review before any commitment.

- You are purchasing through a limited company or in a complex joint ownership structure — SDLT and mortgage conditions differ significantly from individual purchases.

- The property is in a selective licensing zone — confirm this with the local authority before exchange, not after completion.

- The building is a qualifying higher-risk building under the Building Safety Act 2022 — new specific obligations apply to landlords of affected buildings.

How Housey can help

Whether you are purchasing your first investment property or expanding a portfolio, our conveyancing service can connect you with experienced solicitors who handle buy-to-let transactions regularly, understand local licensing requirements, and can advise on your SDLT obligations from the outset.

Frequently asked questions

Do I need a specialist solicitor for a buy-to-let purchase?

Not necessarily a different solicitor, but you should confirm that your conveyancer has handled buy-to-let transactions before. They will need to review tenancy agreements, advise on licensing requirements, calculate SDLT correctly including any surcharge, and manage deposit transfer obligations — all of which go beyond the scope of a standard residential purchase.

How much extra SDLT do I pay on a buy-to-let in England?

From 31 October 2024, the additional dwelling surcharge is 5% on top of standard SDLT rates. On a £250,000 purchase, this represents £12,500 in surcharge alone. Always confirm the exact liability with your solicitor, as reliefs such as multiple dwellings relief and linked transaction rules can affect the total amount due.

Can the same solicitor act for both buyer and seller in a buy-to-let transaction?

Dual representation is permitted in limited circumstances under SRA professional conduct rules, but is generally inadvisable in arm's-length transactions. Most buyers instruct their own conveyancer to ensure independent advice, particularly where tenancy agreements, deposit protection, and local authority licensing issues are involved and require careful scrutiny before exchange.

What is a TA6 Property Information Form and why does it matter for buy-to-let?

The TA6 (or equivalent protocol form) is completed by the seller and discloses known information about the property, including disputes, notices, alterations, and tenancy details. For buy-to-let transactions, the seller's replies about existing tenancies, deposit protection, and any local authority notices are particularly important and must be reviewed carefully by your conveyancer before exchange of contracts.

Sources and further reading

- Stamp Duty Land Tax: residential property rates — HM Revenue & Customs / GOV.UK

- Renting out a property: landlord obligations — GOV.UK

- Tenancy deposit protection — GOV.UK

- Minimum energy efficiency standards for private rented homes — GOV.UK

- Houses in Multiple Occupation — GOV.UK

Useful next reads

Buying & Moving

Buying & MovingUnderstanding Leasehold Property: Rights and Responsibilities

Leasehold means you own a time-limited interest in a property while the freeholder owns the land and building.

Buying & Moving

Buying & MovingEPC Requirements for Landlords: Legal Obligations and Compliance

Landlords in England and Wales must ensure privately rented properties achieve a minimum EPC rating of E before letting.

Buying & Moving

Buying & MovingNavigating Simultaneous Purchase and Sale of Property

When buying and selling simultaneously in England and Wales, both sets of contracts are exchanged on the same day — this is called simultaneous exchange.

Buying & Moving

Buying & MovingRight to Buy: Costs, Discounts, and the Path to Home Ownership

Right to Buy lets eligible council tenants in England buy their home at a government-funded discount — between 35% and 70% of its value, depending on tenancy length and property type.

Buying & Moving

Buying & MovingEssential Steps to Selling Your Home Successfully

Selling your home successfully in the UK involves obtaining a valid EPC, choosing an estate agent or alternative method, instructing a solicitor or conveyancer early, and completing the Seller's Property Information Form accurately.