Specialist Properties: Barges and Houseboats for Living

By Housey · Last reviewed 8th of May 2026

Specialist Properties: Barges and Houseboats for Living

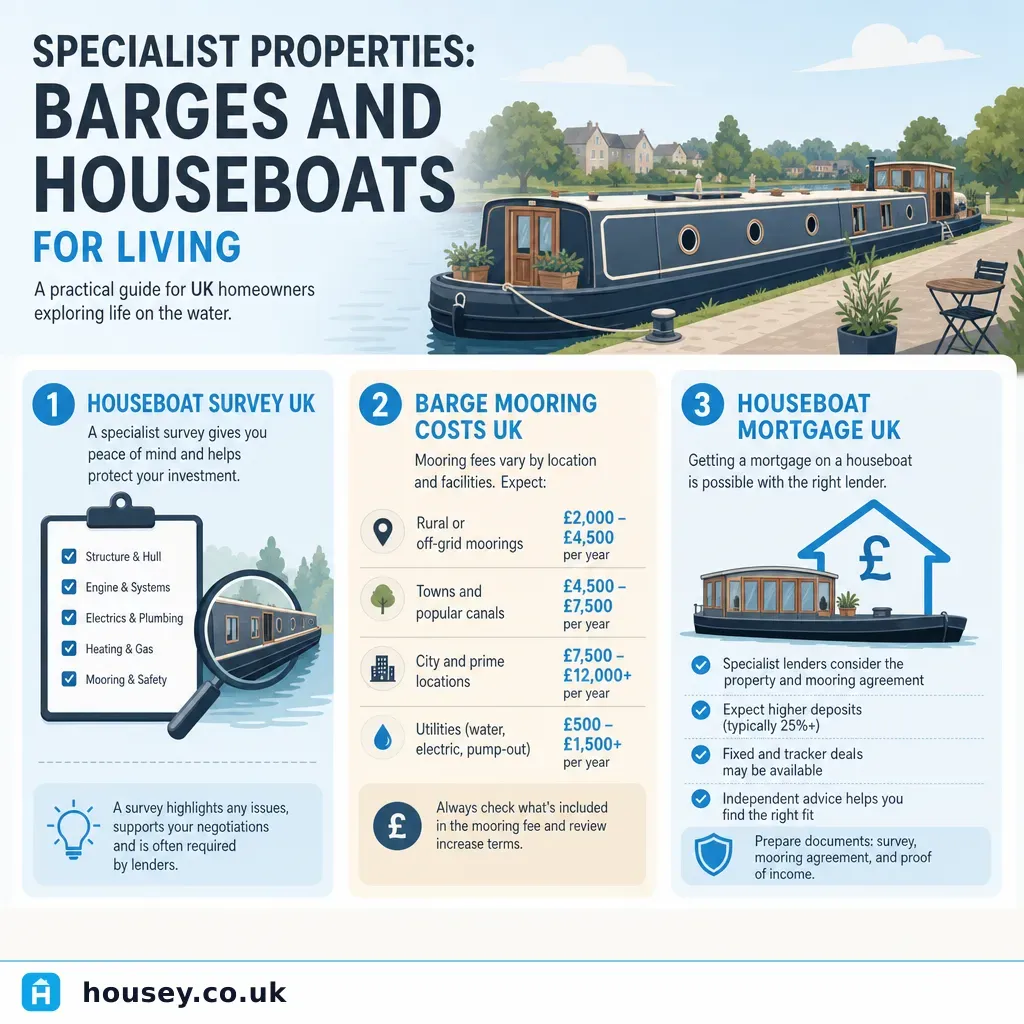

Purchasing a barge, narrowboat, or houseboat in the UK sits entirely outside the standard residential property framework — the legal ownership structures, surveys, finance, and regulatory certificates all follow maritime conventions rather than land law. The question of mooring security is as significant as the vessel's structural condition, and the costs of getting either wrong can be substantial. Whether you are drawn to canal living or a tidal estuary mooring, understanding these differences before making an offer is essential.

Key points

- A Boat Safety Scheme (BSS) certificate — renewed every 4 years — is required for most vessels on Canal & River Trust (CRT) managed waterways; it covers gas, fire, and fuel safety but is not a structural survey.

- Hull surveys must be conducted out of water: for steel-hulled narrowboats and barges this means a dry dock or slipway lift, including ultrasonic thickness testing to detect corrosion.

- Standard residential mortgages cannot be secured against floating vessels: specialist marine finance or houseboat mortgages are required, often with different deposit and loan-to-value terms.

- Mooring tenure is separate from vessel ownership: residential moorings may be freehold, leasehold, or licence-based — each carries different protections and risks.

- RICS surveyors do not survey vessels; use a surveyor accredited by the Yacht Designers and Surveyors Association (YDSA) or the Royal Institution of Naval Architects (RINA).

What kind of vessel can you live on?

The most common types of residential floating home in the UK are:

- Narrowboats: typically around 6ft 10in (2.08m) wide, built for the UK canal network. Most are steel-hulled and range from approximately 40ft to 72ft in length.

- Wide-beam barges: wider than narrowboats (up to approximately 4m), suitable for rivers and wider canals. They offer more living space but are restricted to certain routes.

- Dutch barges and converted commercial barges: large steel vessels, often converted to a high specification, found mainly on rivers and tidal waters.

- Purpose-built floating homes: increasingly found at purpose-developed residential marina berths, sometimes resembling conventional homes on floating pontoons.

Each type has different survey requirements, running costs, and restrictions on where it can be moored and navigated.

Legal status and mooring tenure

A vessel is personal property (a chattel), not land. It is not registered at HM Land Registry. Ownership is evidenced by a Bill of Sale and, for larger vessels or those on tidal waters, possibly registration with the MCA's Small Ships Register or Part I Register under the Merchant Shipping Act 1995.

Mooring tenure is one of the most important factors to assess before purchase:

Mooring type | Ownership structure | Key risks |

|---|---|---|

Freehold mooring | You own the land beneath the berth | Rare; provides maximum security |

Long leasehold mooring | Leasehold interest, typically 99+ years | Check ground rent, service charges, break clauses |

Licence-based mooring | Contractual right only; no property interest | Can be terminated with notice; check licence terms carefully |

CRT residential licence | Canal & River Trust licence for a specific mooring or continuous cruising | Residential use requires specific CRT approval; not all moorings permit this |

A solicitor experienced in marine and waterways property should review any mooring agreement before exchange. This is not a standard conveyancing transaction.

Surveys and inspections for floating homes

Unlike a conventional property, no single survey covers everything you need. Expect to commission several separate assessments:

1. Hull survey (out of water) This is the most critical structural assessment for a steel-hulled vessel. The boat must be lifted out of the water — typically at a dry dock or boatyard — so the surveyor can inspect the hull externally, test steel thickness using ultrasonic gauges, and check the condition of the blacking (anti-corrosion coating), anodes, and underwater fittings. Indicative UK costs range from approximately £300–£800 for a narrowboat hull survey, varying by vessel size and boatyard rates (Indicative UK costs, last reviewed 2026-05-08; obtain quotes from at least two YDSA-accredited surveyors).

2. Full condition survey (in-water inspection) This covers the superstructure, internal fit-out, electrical systems, plumbing, engine, and general condition of the vessel. Combined hull and condition surveys are sometimes offered together.

3. Boat Safety Scheme (BSS) examination Conducted by a BSS-registered examiner, this checks gas installations, fire extinguishers, fuel systems, and engine ventilation. A valid BSS certificate is required for most CRT licences. It does not replace a structural survey.

4. Engine and mechanical inspection If the vessel has a diesel or petrol engine, a specialist marine engineer should inspect it separately unless the condition survey explicitly covers this.

If the floating home is connected to shore-based infrastructure — pontoons, jetties, or boathouse structures — a structural survey of shore-based infrastructure of those fixed elements may be appropriate. For identified concerns with specific elements, specific defect surveys can address targeted issues in onshore structures.

Comparing a floating home with a conventional property purchase

Factor | Floating home | Conventional residential property |

|---|---|---|

Survey professional | YDSA or RINA accredited marine surveyor | RICS-registered surveyor |

Legal registration | Bill of Sale; MCA register (depends on vessel type and size) | HM Land Registry |

Finance | Marine mortgage or specialist lender | Standard residential mortgage |

Annual running costs | Mooring fees, CRT licence, blacking, insurance, diesel | Council tax, utilities, buildings insurance |

Safety certificate | BSS certificate every 4 years | EPC required for rental only |

Planning considerations | For mooring infrastructure; not the vessel itself | For extensions and alterations |

Tenure security | Dependent on mooring agreement | Freehold or leasehold title |

Financing a floating home

Most high-street lenders do not offer mortgages on vessels. Options typically include:

- Specialist marine mortgage lenders: a small number of UK lenders offer products specifically for live-aboard vessels. Typical loan-to-value ratios are lower than standard residential mortgages, often 70–80%, and a satisfactory hull survey is usually a condition of the loan.

- Personal loans or marine finance: for lower-value narrowboats, some buyers use secured or unsecured personal loans. Interest rates and terms vary significantly.

- Cash purchase: common at lower price points, particularly for narrowboats under £100,000.

Always confirm that any lender has experience with the specific vessel type and mooring tenure. A marine mortgage broker can help identify appropriate products.

Red flags when viewing a houseboat or barge

These issues warrant close scrutiny or, in some cases, withdrawal from the purchase:

- No recent out-of-water hull survey: a vessel that has not been lifted and surveyed in the past 5 years carries unknown hull condition risk.

- Thin steel readings: ultrasonic thickness below approximately 3–4mm (depending on plate position and vessel specification) indicates serious corrosion risk in steel-hulled vessels.

- Unclear or short-term mooring arrangement: a licence-only mooring with minimal notice protection means you could lose your berth with limited warning.

- No valid BSS certificate: indicates the vessel may fail the safety check required for a CRT licence.

- Bubbling paintwork, rust, or soft spots below the waterline: these suggest active hull degradation.

- Unauthorised residential use: some moorings permit leisure use only; residential occupation may be unlawful under planning conditions.

- Outstanding finance on the vessel: vessels can be subject to maritime liens or hire-purchase agreements; a marine solicitor should carry out a vessel search before exchange.

- Persistent condensation, damp, or mould inside: floating homes are prone to condensation; significant mould suggests inadequate ventilation or insulation that will need addressing.

Important limitations

This article provides general information about buying a floating home in the UK. Requirements and rules can vary depending on vessel type, its location (tidal versus non-tidal waters, CRT waterways versus private navigation authorities), mooring tenure, and the local planning authority. Nothing in this article constitutes legal, financial, structural, or marine engineering advice. Always appoint a qualified marine surveyor, a solicitor experienced in waterways property, and a specialist marine finance broker for your specific situation.

What to ask a qualified professional

Before appointing a marine surveyor:

- Are you a member of YDSA, RINA, or another recognised marine surveying body?

- Does your survey include an out-of-water hull inspection, or only an in-water condition assessment?

- Will you provide ultrasonic steel thickness readings with your report?

- What happens if the hull cannot be lifted during the survey period?

- Does your report cover the engine and mechanical systems, or is that a separate instruction?

Before signing a mooring agreement:

- Is this mooring approved for residential use under planning law?

- What is the notice period for termination, and on what grounds can the agreement be ended?

- Are there restrictions on vessel type, length, or beam at this mooring?

- Who is responsible for maintaining the pontoon, and the water and electricity connections?

Before arranging marine finance:

- Do you have experience with this vessel type and mooring tenure?

- What LTV ratio is available, and what valuation or survey approach do you require?

- Is a valid BSS certificate and hull survey required as a condition of the offer?

When to get professional help

Appoint a qualified marine surveyor before making any offer on a houseboat or barge — do not rely on a BSS examination alone as evidence of structural integrity. If you are uncertain about a mooring's legal status or a vessel's registration, instruct a solicitor with specific waterways experience before exchange. If you are constructing new mooring infrastructure or a boathouse, consult your local planning authority about consent requirements before any work begins.

How Housey can help

Housey connects you with professionals who can assess fixed waterfront and onshore structures. For shore-side infrastructure such as jetties, pontoons, and boathouse structures, request a structural survey of shore-based infrastructure or a specific defect survey for targeted concerns. Use Housey to compare quotes from experienced surveyors in your area.

Frequently asked questions

Do I need planning permission to live on a houseboat in the UK?

Not for the vessel itself, but the mooring may require planning permission — particularly if it involves new pontoons, jetties, or changes to riverbank infrastructure. Residential use of a mooring is a material change of use and generally requires planning consent. Always check with the relevant local planning authority and the Canal & River Trust before assuming residential use is permitted.

What is a Boat Safety Scheme certificate and do I need one?

The Boat Safety Scheme (BSS) certificate confirms that a vessel's gas, fire, and fuel systems meet minimum safety standards. It is required every 4 years for most boats on inland waterways managed by the Canal & River Trust. It is not a full structural survey and does not assess hull integrity — a separate out-of-water hull survey is needed for that.

Can I get a standard mortgage on a houseboat or barge?

No. Conventional residential mortgages cannot be secured against floating vessels, which are not registered at HM Land Registry. You will need marine finance or a specialist houseboat mortgage from a lender with experience in vessel security. Loan-to-value ratios, deposit requirements, and survey conditions typically differ from standard residential products.

How often should a houseboat hull be surveyed?

A full out-of-water hull survey is generally recommended every 5–10 years, or before any purchase regardless of when the previous one was carried out. For steel-hulled narrowboats and barges, this involves a dry dock or slipway lift, ultrasonic thickness testing, and inspection of the blacking and anodes. The surveyor should be an accredited member of YDSA or a comparable body.

Sources and further reading

- Boat Safety Scheme — BSS certificate requirements and registered examiners

- Canal & River Trust: Boating licences — CRT licence requirements including residential mooring conditions

- Yacht Designers and Surveyors Association — Accredited marine surveyors for vessel condition and hull surveys

- GOV.UK: Register a boat — MCA Small Ships Register information

- GOV.UK: Stamp Duty Land Tax — SDLT applies to mooring land interests but not to the vessel itself

Useful next reads

Surveys & Inspections

Surveys & InspectionsWhy Property Boundaries Matter: Surveying and Dispute Prevention

Property boundaries in England and Wales are recorded as general boundaries by HM Land Registry — not precise measurements.

Surveys & Inspections

Surveys & InspectionsSafe Property Viewing Practices: Protecting Yourself During Inspections

When viewing a property in the UK, always tell someone where you are going and share the full address before you leave.

Surveys & Inspections

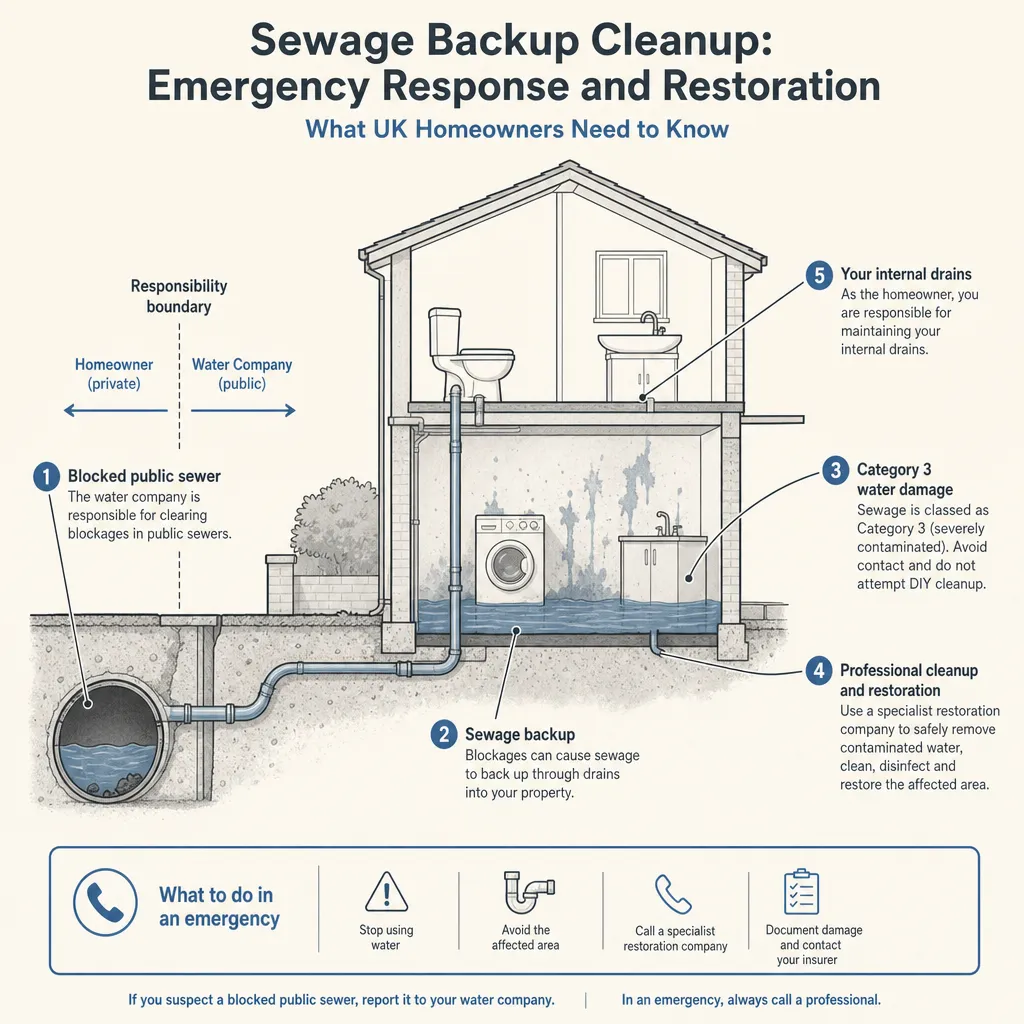

Surveys & InspectionsSewage Backup Cleanup: Emergency Response and Restoration

A sewage backup should be treated as a Category 3 contamination event.

Surveys & Inspections

Surveys & InspectionsIdentifying Asbestos Insulation: What You Need to Know for Your Property

Asbestos insulation was widely used in UK properties built before 2000, commonly found in pipe lagging, ceiling tiles, loose-fill loft insulation, and around boilers.

Surveys & Inspections

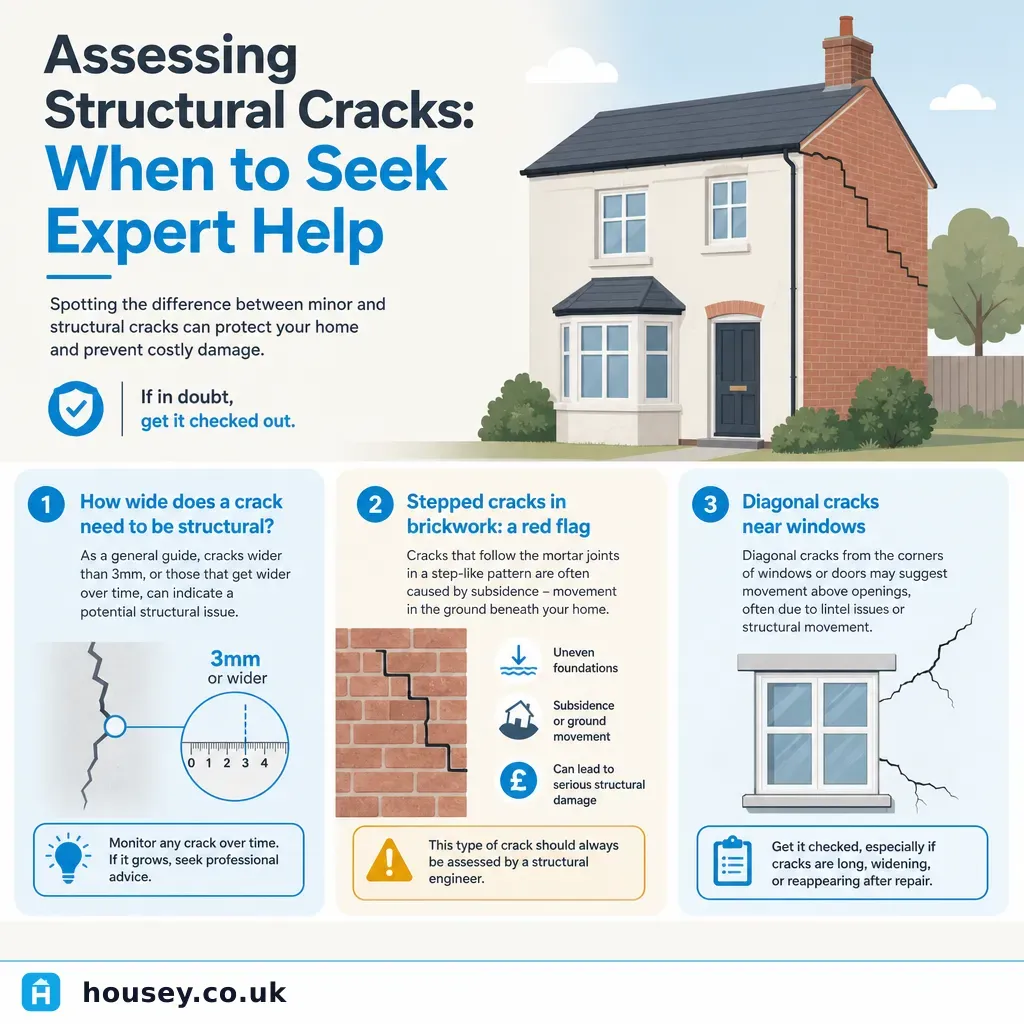

Surveys & InspectionsAssessing Structural Cracks: When to Seek Expert Help

Structural cracks range from harmless shrinkage hairlines to signs of subsidence or foundation movement.