Complete Guide to Purchasing Property in the UK

By Housey · Last reviewed 31st of May 2026

Complete Guide to Purchasing Property in the UK

Buying a home in the UK is a multi-stage legal and financial process that typically takes between three and five months from offer acceptance to completion, involving solicitors, surveyors, mortgage lenders, and estate agents at various points. First-time buyers, those moving up the ladder, and investors all face the same legal framework — though the specifics differ for leasehold properties, new builds, and homes in Scotland, which operates a separate conveyancing system based on missives. Getting the right professionals in place early and understanding the sequence of steps can significantly reduce the risk of costly surprises after you've committed funds.

Key points

- In England and Wales, neither party is legally bound until exchange of contracts — either side can withdraw before then, sometimes with significant financial consequences for the buyer who has already paid for surveys and searches.

- Stamp Duty Land Tax (SDLT) rates and thresholds changed in April 2025 — use the GOV.UK SDLT calculator for current figures, as first-time buyer relief thresholds were adjusted at that point.

- A mortgage lender's valuation is carried out for the lender's benefit, not the buyer's — it will not identify building defects or structural problems.

- Leasehold properties require additional legal checks beyond standard freehold conveyancing: remaining lease length, ground rent terms, service charge history, and any major works planned by the freeholder.

- In Scotland, the process differs substantially — offers are legally binding at the point of conclusion of missives, and most properties are marketed with a Home Report that includes a condition survey.

Step 1: Before making an offer

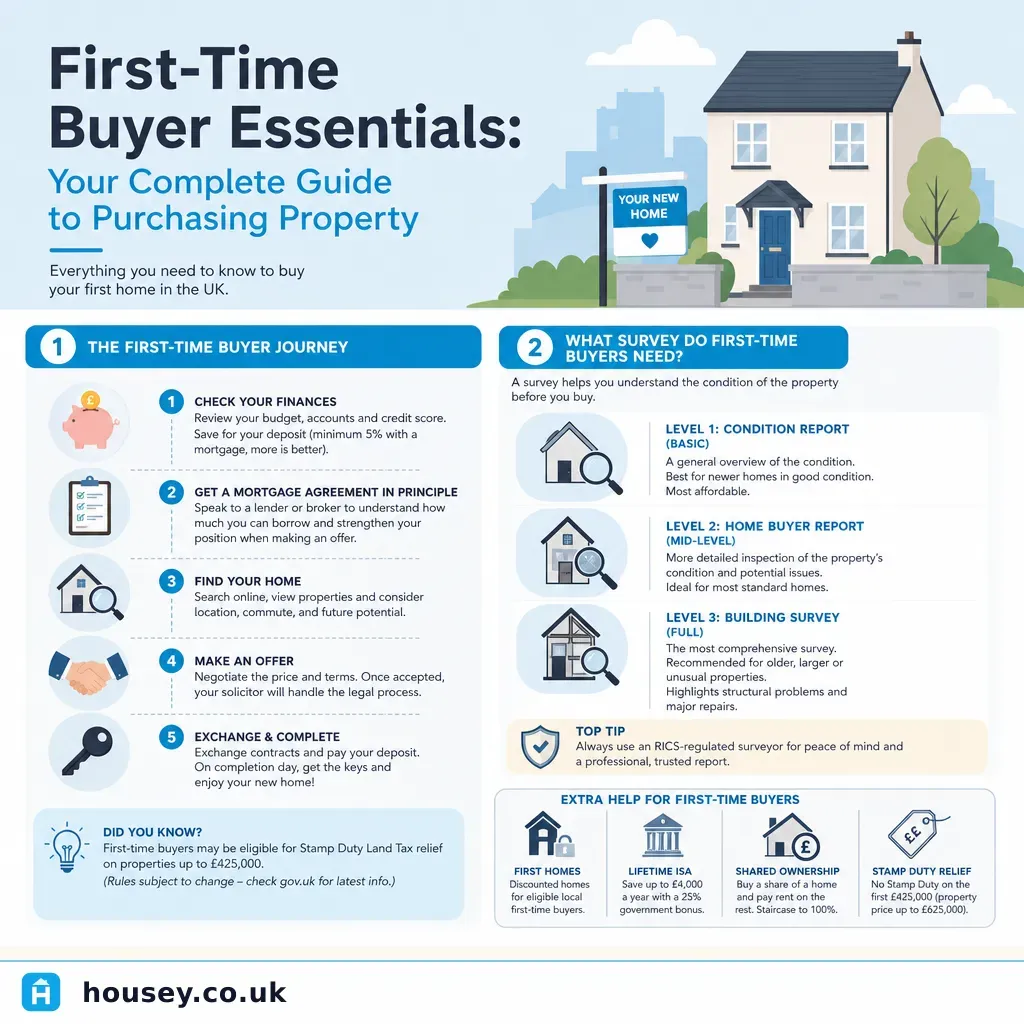

Before viewing or offering on property, put your finances in order:

- Obtain a mortgage agreement in principle (AIP) from a lender or mortgage broker — this demonstrates to sellers and estate agents that you are a credible buyer. It is not a full mortgage offer and does not guarantee lending.

- Calculate your total budget including SDLT, legal fees, survey costs, removal costs, and any immediate repairs — not just the deposit and mortgage repayments.

- Register with local estate agents and set up search alerts on Rightmove, Zoopla, and OnTheMarket for your target areas and price range.

Indicative upfront buying costs in England (2026): SDLT (rates vary by price, buyer status, and whether you own other property — use the GOV.UK SDLT calculator); solicitor or conveyancer fees £1,200–£2,500 plus disbursements; survey £400–£1,500 depending on level; mortgage arrangement fee £0–£2,000; removals £300–£2,000+. Indicative UK costs, last reviewed 2026-05-31.

Step 2: Making an offer and instructing professionals

Once you've found a property:

- Make your offer through the estate agent, in writing, stating it is subject to survey and mortgage.

- Instruct a conveyancer or solicitor as soon as the offer is accepted — do not wait until searches are ordered.

- Apply for your full mortgage using the agreed offer price.

- Book an independent survey — your choice of survey level is one of the most consequential decisions in the buying process.

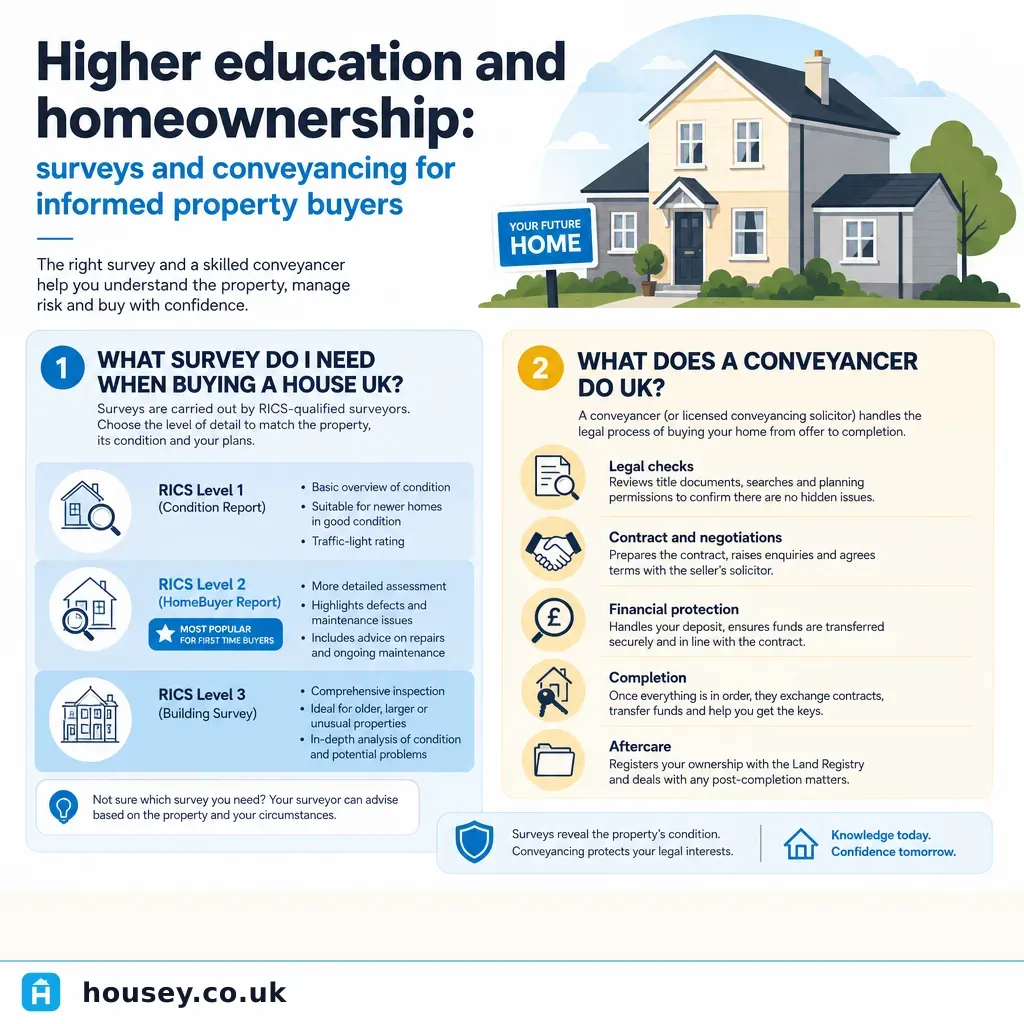

Choosing the right survey: a comparison

Survey type | Best suited to | What it covers | Typical cost (indicative, 2026) |

|---|---|---|---|

RICS Level 1 Condition Report | New builds or recently completed conventional homes | Traffic-light condition ratings; no detailed advice | £300–£500 |

RICS Level 2 Home Survey | Conventional homes in broadly reasonable condition | Defects, risks, urgent repairs, maintenance advice | £400–£900 |

RICS Level 3 Building Survey | Older, larger, unusual, altered, or visibly defective properties | Full structural assessment, maintenance advice, cost guidance | £600–£1,500 |

Structural engineer's report | Specific defect investigation — cracks, movement, subsidence | Targeted engineering diagnosis of a known issue | £300–£800+ |

New-build snagging inspection | New-build properties before legal completion | Defects and incomplete work to report to the developer | £300–£600 |

A mortgage lender's valuation is not a survey and will not protect you as a buyer. Always commission your own independent inspection before exchange of contracts.

Step 3: Conveyancing — what happens during the legal process

Your conveyancer or solicitor will carry out the legal work in parallel with your survey and mortgage application:

- Raise enquiries with the seller's solicitor about the property, boundaries, and any disputes

- Review title documents and Land Registry entries at HM Land Registry

- Order searches (local authority, drainage, environmental, and others depending on location and property type)

- Review the formal mortgage offer once it arrives and check any conditions attached

- Report to you on all findings and flag issues before exchange

Common causes of delay: slow local authority searches (some take 4–8 weeks), missing documents from sellers, complex leasehold titles, management company enquiries, and issues revealed by environmental or drainage searches.

For leasehold properties, ask your solicitor to check: remaining lease length (below 80 years becomes increasingly expensive to extend); ground rent terms (escalating or doubling ground rents can affect mortgage eligibility); service charge history and accounts for at least three years; and any major works planned or already started by the freeholder.

Step 4: Exchange and completion

Exchange of contracts is the point at which both parties become legally bound. At exchange, the buyer pays a deposit — typically 10% of the purchase price, though 5% is sometimes agreed — and a completion date is set in the contract.

Between exchange and completion, you should:

- Arrange buildings insurance, which should be in place from the point of exchange

- Confirm your removal booking and finalise logistics

- Notify utilities, DVLA, HMRC, your bank, your employer, and any other relevant organisations of your new address

- Carry out a final inspection of the property if the seller agrees

Completion occurs when your solicitor transfers the balance of funds to the seller's solicitor, keys are released, and legal ownership passes to you. Your solicitor will register the title transfer at HM Land Registry.

Document preparation checklist

Having these documents ready early speeds up mortgage applications and conveyancing:

Important limitations

Property law in England and Wales is complex and subject to change. This article is a general guide only and does not constitute legal, financial, or surveying advice. Stamp duty rates, search timescales, mortgage requirements, leasehold rules, and conveyancing practice can vary and change. Scotland and Northern Ireland operate under different legal frameworks. Always instruct a qualified solicitor or licensed conveyancer for legal work and take independent financial advice before committing to a purchase.

When to get professional help

You should not proceed without professional advice if:

- The property is leasehold with fewer than 90 years remaining on the lease

- Searches reveal contamination, flooding risk, planning enforcement notices, or highway issues

- The survey identifies structural movement, serious damp, roof defects, or other significant problems

- You are buying through Help to Buy, shared ownership, or another government scheme

- The seller's title has missing documents, unregistered land, or restrictions you do not understand

- The property is listed, in a conservation area, or has had unauthorised alterations

What to ask a qualified professional

Before instructing a conveyancer or solicitor:

- Are you regulated by the Solicitors Regulation Authority (SRA) or the Council for Licensed Conveyancers (CLC)?

- Is the quoted fee fixed or an estimate, and which disbursements (searches, Land Registry fees, bank transfer fees) are charged on top?

- How will you communicate updates, and what is your average timescale for this type of transaction?

Before booking a survey:

- Which RICS survey level do you recommend for this property, and what factors influence that recommendation?

- Will you flag items that may need specialist follow-up, such as asbestos, drainage, electrical condition, or structural movement?

- Can I speak to you after the report is issued to discuss the findings and any recommended next steps?

How Housey can help

Housey connects you with professionals at every stage of a UK property purchase. Find qualified conveyancers and solicitors for the legal process, or book a RICS Home Survey matched to your property type and condition. For older or unusual properties, a structural survey provides the detailed inspection you may need before exchange. If you require a standalone valuation survey, Housey can connect you with RICS-registered valuers. Buying a new build? A new-build snagging inspection helps identify defects before legal completion. When you're ready to move, Housey also connects you with house removal companies.

Frequently asked questions

How long does buying a property in the UK take?

In England and Wales, the average time from offer acceptance to completion is 12–16 weeks, though complex chains, title issues, or slow searches can extend this considerably. Scotland operates a different legal process: once missives are concluded the transaction is legally binding, and timescales vary depending on the stage at which surveys and formal offers are arranged.

What searches are carried out during conveyancing?

Standard searches typically include a local authority search covering planning history, road adoption, and nearby proposals; a drainage and water search; and an environmental search for flood risk and contamination. Additional searches — such as coal mining, chancel repair, or specific flood risk assessments — may be recommended by your conveyancer depending on the property's location and construction history.

Can I pull out of a property purchase before exchange?

Yes. In England and Wales, either party can withdraw before exchange of contracts without legal penalty, though you will likely lose survey, solicitor, and search costs already incurred. After exchange, withdrawal exposes you to financial penalties including potential loss of your deposit. In Scotland, once missives are concluded the contract is legally binding and withdrawal may carry significant financial consequences.

Do I need a solicitor or can I use a licensed conveyancer?

Both are qualified to handle residential property transactions. Solicitors are regulated by the Solicitors Regulation Authority (SRA); licensed conveyancers by the Council for Licensed Conveyancers (CLC). Either is generally suitable for straightforward freehold purchases. Complex transactions — particularly those involving leasehold titles, disputes, missing deeds, or unusual land registry entries — may benefit from the broader legal expertise of a solicitor.

Sources and further reading

- GOV.UK — Stamp Duty Land Tax calculator — GOV.UK

- HM Land Registry — buying and owning property — GOV.UK

- RICS — home surveys — RICS

- Law Society — conveyancing guide — Law Society

- Citizens Advice — buying a home — Citizens Advice

- GOV.UK — leasehold property — GOV.UK

Useful next reads

Buying & Moving

Buying & MovingShared Ownership: Building Your Path To Property Ownership

Shared ownership lets you buy a share of a home — typically 10% to 75% — from a housing association and pay subsidised rent on the remainder.

Buying & Moving

Buying & MovingHigher education and homeownership: surveys and conveyancing for informed property buyers

Informed property buyers in the UK typically commission a RICS Level 2 or Level 3 survey before exchange, alongside instructing a conveyancer to carry out legal searches and review title.

Buying & Moving

Buying & MovingUnderstanding Property Conveyancing in England and Wales

Conveyancing is the legal process of transferring property ownership in England and Wales.

Buying & Moving

Buying & MovingPre-Purchase Property Assessment: Strategies and Buyer Advisory

A pre-purchase property assessment in the UK typically combines an independent RICS Home Survey, conveyancing searches, and specialist inspections for damp or electrical condition where needed.

Buying & Moving

Buying & MovingFirst-Time Buyer Essentials: Your Complete Guide to Purchasing Property

Buying your first UK home involves six key stages: securing a mortgage Agreement in Principle, making an offer, instructing a solicitor, commissioning an independent RICS survey, exchanging contracts (the legally binding point), and completing.