First-Time Buyer Essentials: Your Complete Guide to Purchasing Property

By Housey · Last reviewed 18th of May 2026

First-Time Buyer Essentials: Your Complete Guide to Purchasing Property

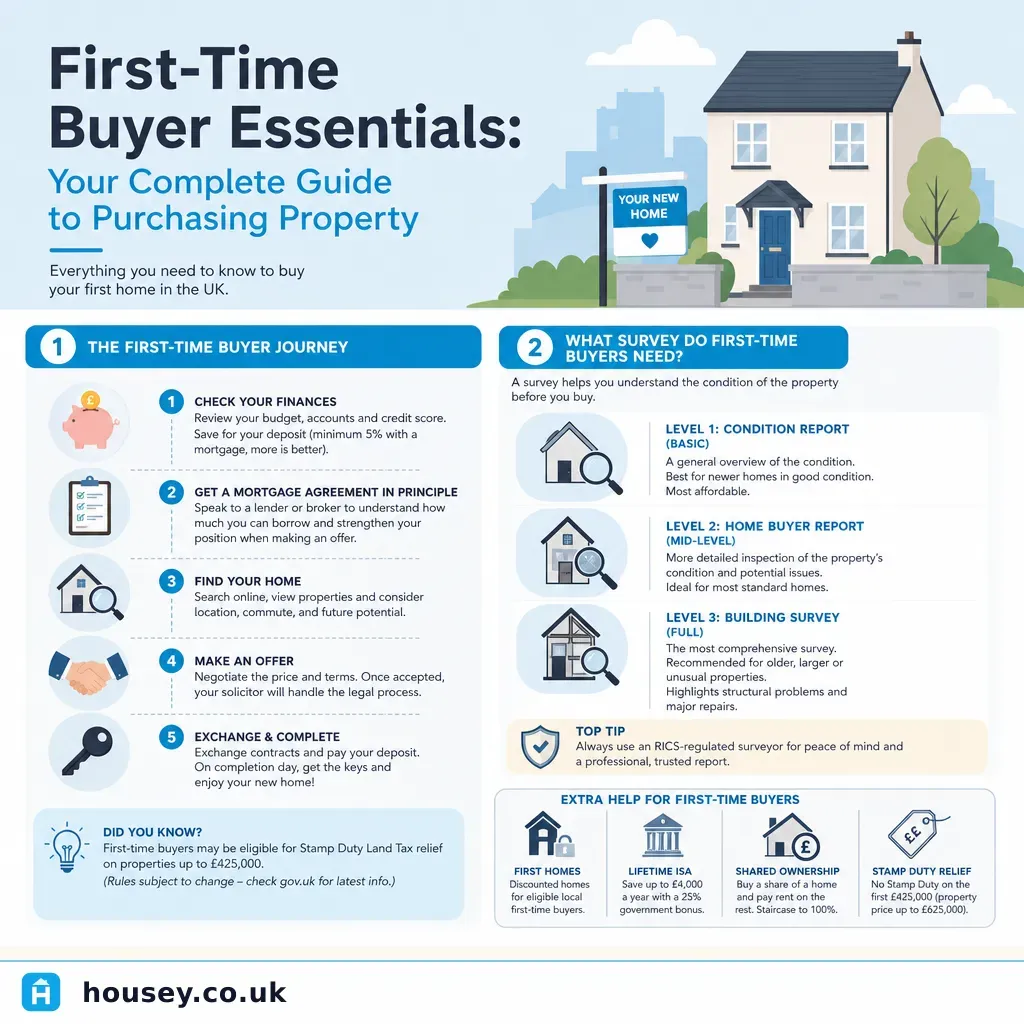

Buying your first home in the UK involves a sequence of legal, financial, and practical steps — each with its own timeline, cost, and risk. Most first-time buyers encounter this process with limited prior experience, navigating mortgage applications, conveyancing, surveys, and exchange within a market that can move quickly and unpredictably. Understanding what each stage involves — and what can go wrong — is the most practical preparation you can do before making an offer.

Key points

- Stamp Duty Land Tax (SDLT) relief in England means first-time buyers pay 0% on the first £300,000 and 5% on £300,001–£500,000; separate regimes apply in Scotland (Land and Buildings Transaction Tax) and Wales (Land Transaction Tax) — check the relevant revenue authority for current thresholds.

- Exchange of contracts — not offer acceptance — is the legally binding point; either party can withdraw without penalty before exchange.

- A mortgage Agreement in Principle (AIP) typically takes 24–48 hours to obtain and signals to sellers and estate agents that you are a credible buyer with financing in place.

- A RICS Level 2 Home Survey is usually appropriate for conventional homes built after around 1900 in reasonable condition; a RICS Level 3 Building Survey is recommended for older, extended, altered, or visibly defective properties.

- Conveyancing typically takes 8–12 weeks from offer acceptance to completion; leasehold purchases commonly take longer due to additional enquiries directed to the freeholder or managing agent.

What happens at each stage

The UK buying process follows a broadly linear sequence, though delays and complications are common. Understanding each stage helps you prepare documents, instruct professionals at the right time, and avoid avoidable hold-ups.

- Budget and mortgage preparation — Establish your deposit, obtain a mortgage Agreement in Principle from a lender or broker, and confirm your total budget including purchase costs: SDLT, legal fees, survey, and removal.

- Property search and offer — Search via estate agents, Rightmove, Zoopla, and local agents; make a written offer subject to survey and contract.

- Instruct a solicitor or licensed conveyancer — Your conveyancer raises enquiries, reviews title documents, commissions searches (local authority, drainage, environmental), and reports to your lender.

- Commission an independent survey — This is separate from the lender's valuation; choose the appropriate RICS survey level for the property's age, type, and condition.

- Exchange of contracts — Both parties sign and exchange identical contracts; you pay your deposit (typically 10%); a completion date is fixed and becomes legally binding.

- Completion — The balance transfers; you receive the keys; your conveyancer registers the title with HM Land Registry.

Which survey do you need?

A lender's mortgage valuation confirms the property is adequate security for the loan — it is not a condition survey and should not substitute for an independent inspection. Choosing the right RICS survey level depends on the property's age, construction, and visible condition.

Property situation | Likely survey choice | Why |

|---|---|---|

1990s or newer estate house, standard construction, no visible defects | RICS Level 2 Home Survey | Conventional build; moderate risk of hidden defects |

1930s–1980s semi-detached or terrace, some wear visible | RICS Level 2 Home Survey | Age warrants close inspection; standard structure |

Victorian or Edwardian terrace, solid walls, past alterations | RICS Level 3 Building Survey | Older construction, likely hidden defects, detailed report needed |

Listed building, thatched cottage, or converted property | RICS Level 3 or specialist survey | Non-standard construction; lender may require additional checks |

Any property with visible cracks, damp, or suspected structural movement | RICS Level 3 or structural engineer report | General survey may identify concern; engineering diagnosis may also be needed |

Decision tree: are you ready to make an offer?

- Proceed if you have a mortgage Agreement in Principle, a solicitor ready to instruct, and have viewed the property at least once in person.

- Wait if you have not confirmed your borrowing capacity — you risk losing the property to a buyer with financing already arranged.

- Speak to your mortgage broker first if you are self-employed, have recent credit events, or are buying via a Help to Buy or shared ownership scheme — eligibility rules and deposit requirements differ.

- Consult a solicitor before offering on any leasehold property where the lease has fewer than 80 years remaining — lease extension costs can be significant and some lenders will decline to lend.

- Check with your local planning authority if the property has had recent alterations with no visible building regulations completion certificate — retrospective indemnity insurance may be required.

What not to assume as a first-time buyer

Many first-time buyers make avoidable and costly mistakes based on common misunderstandings.

- Do not assume an accepted offer is secure. In England and Wales, verbal and written offer acceptances are not legally binding. The seller can accept a higher offer — gazumping — at any point before exchange.

- Do not rely solely on the lender's valuation. It confirms the lender's security, not the property's condition. Commissioning your own RICS survey is strongly advisable on any property.

- Do not assume the quoted completion date will hold. Chains frequently cause delays — build in flexibility on tenancy end dates, storage bookings, and removal dates.

- Do not confuse exchange and completion. You are legally committed at exchange, not completion. Missing completion after exchange can result in penalty interest and potential legal action.

- Do not overlook leasehold implications. Service charges, ground rent restrictions under the Leasehold Reform (Ground Rent) Act 2022, and the distinction between share of freehold and long leasehold are live issues your conveyancer should explain before exchange.

First-time buyer costs checklist

Cost item | Typical range in England | Notes |

|---|---|---|

Mortgage arrangement fee | £0–£2,000 | Often added to the loan; compare total cost over the deal period |

RICS Level 2 Home Survey | £400–£900 | Varies by property size, location, and surveyor |

RICS Level 3 Building Survey | £600–£1,500+ | Complex or large properties at the higher end |

Conveyancing (solicitor or conveyancer) | £1,000–£2,500 | Plus disbursements: searches, Land Registry fee, ID checks |

Stamp Duty Land Tax (first-time buyer relief) | £0 on first £300,000; 5% on £300,001–£500,000 | Check GOV.UK for current thresholds; separate rates apply in Scotland and Wales |

Removal costs | £400–£2,000+ | Depends on volume, distance, and access |

Indicative UK costs, last reviewed 2026-05-18. Figures vary by property, location, and provider. Always request itemised quotes.

Important limitations

This article provides general information about the UK home-buying process. Property law, mortgage eligibility, stamp duty thresholds, and survey requirements vary depending on tenure type (freehold or leasehold), property condition, lender criteria, and location. Rules in Scotland and Wales differ materially from those in England and Northern Ireland. Nothing in this article constitutes legal or financial advice. Always instruct a qualified solicitor or licensed conveyancer and take independent mortgage advice from a regulated broker.

What to ask a qualified professional

When instructing a conveyancer:

- Are you a solicitor or licensed conveyancer, and what is your experience with this property type and tenure?

- What searches will you commission, and what are the full disbursement costs?

- If title issues or lease complications arise, will the fee change?

- How will you communicate progress, and what are your typical response times?

When commissioning a survey:

- Is the surveyor RICS-registered, and do they have experience with this property type and construction era?

- What will the report cover, and what are the survey's limitations?

- Will you flag anything that may affect the mortgage offer or future resale?

When arranging a mortgage:

- Is this regulated mortgage advice, and are you a whole-of-market broker?

- What are the total costs over the initial deal period, including all fees and the reversion rate?

- How might my circumstances — self-employment, credit history, or property type — affect my options?

When to get professional help

Instruct a qualified professional rather than relying on general guidance if:

- The property is leasehold with fewer than 80 years remaining on the lease.

- You are buying with a Help to Buy equity loan, shared ownership, or any government scheme with specific legal requirements.

- The survey uncovers significant defects — damp, structural movement, roof issues, or non-standard construction.

- You receive a mortgage refusal or down-valuation.

- The seller is pressing for an unusually short exchange timeline.

- Conveyancing searches reveal planning, building regulations, or boundary concerns that require legal advice.

How Housey can help

Housey connects first-time buyers with RICS-registered surveyors and experienced conveyancing solicitors across the UK. Whether you need a RICS Level 2 survey to check the condition of a conventional home, RICS Home Surveys for a more complex or older property, or a solicitor to handle your conveyancing, you can compare quotes from verified local professionals in one place.

Frequently asked questions

Do I need a survey if the lender instructs a valuation?

Yes. A mortgage valuation confirms the property is adequate security for the loan but is not a condition survey. It will not identify damp, structural defects, roof problems, or outdated electrics. An independent RICS survey gives you an informed picture of the property before you are legally committed at exchange of contracts.

Can a seller accept a higher offer after accepting mine in England and Wales?

Yes. Until exchange of contracts, neither party is legally bound. A seller can accept a higher offer — known as gazumping — at any point before exchange. Moving quickly through conveyancing and commissioning your survey promptly reduces the window of exposure, but there is no statutory protection against it in England and Wales.

What is the difference between exchange and completion?

Exchange is the legally binding stage: both parties sign identical contracts and you pay your deposit, usually 10%. Completion is when the balance transfers and you receive the keys. These stages are usually separated by one to four weeks, though simultaneous exchange and completion occurs in some chain-free transactions.

How long does conveyancing take for a first-time buyer?

Most freehold purchases complete within 8 to 12 weeks of offer acceptance. Leasehold purchases typically take longer — often 12 to 16 weeks — due to additional enquiries directed to the freeholder or managing agent. Chains, missing documents, and delayed searches are the most common causes of delay.

Sources and further reading

- Stamp Duty Land Tax: first-time buyers relief — GOV.UK

- RICS Home Surveys — Royal Institution of Chartered Surveyors

- Leasehold Reform (Ground Rent) Act 2022 — legislation.gov.uk

- Buying a home — Citizens Advice

- HM Land Registry registration services fees — HM Land Registry

Useful next reads

Buying & Moving

Buying & MovingFirst-Time Homebuyer's Guide to Moving and Property Inspections

First-time buyers in the UK should know that a lender's mortgage valuation is not a property survey and does not protect the buyer.

Buying & Moving

Buying & MovingComplete Guide to Purchasing Property in the UK

Buying property in England and Wales typically takes 12 to 16 weeks from offer acceptance to completion.

Buying & Moving

Buying & MovingShared Ownership: Building Your Path To Property Ownership

Shared ownership lets you buy a share of a home — typically 10% to 75% — from a housing association and pay subsidised rent on the remainder.

Buying & Moving

Buying & MovingComplete Property Conveyancing Guide: From Offer to Completion

UK property conveyancing typically takes 8 to 16 weeks from offer to completion.

Buying & Moving

Buying & MovingFirst-Time Buyer Properties: Finding Your First Home

First-time buyers in the UK can access support including the Lifetime ISA, which adds a 25% government bonus on savings of up to £4,000 per year.