Financing Your Property Purchase: Key Mortgage Considerations for UK Buyers

By Housey · Last reviewed 18th of May 2026

Financing Your Property Purchase: Key Mortgage Considerations for UK Buyers

Securing a mortgage is the central financial step in buying a UK property, yet the range of products, eligibility criteria, and timing constraints means that making the right choices requires more than a quick comparison website search. Whether you are a first-time buyer weighing up a fixed versus tracker rate, or a home mover navigating your existing mortgage while purchasing a new property, understanding the landscape before you apply can save thousands of pounds and prevent delays at a critical point in the transaction.

Key points

- Most UK mortgage lenders assess affordability using income multiples of 4–4.5 times annual salary, though some specialist lenders go higher subject to specific criteria.

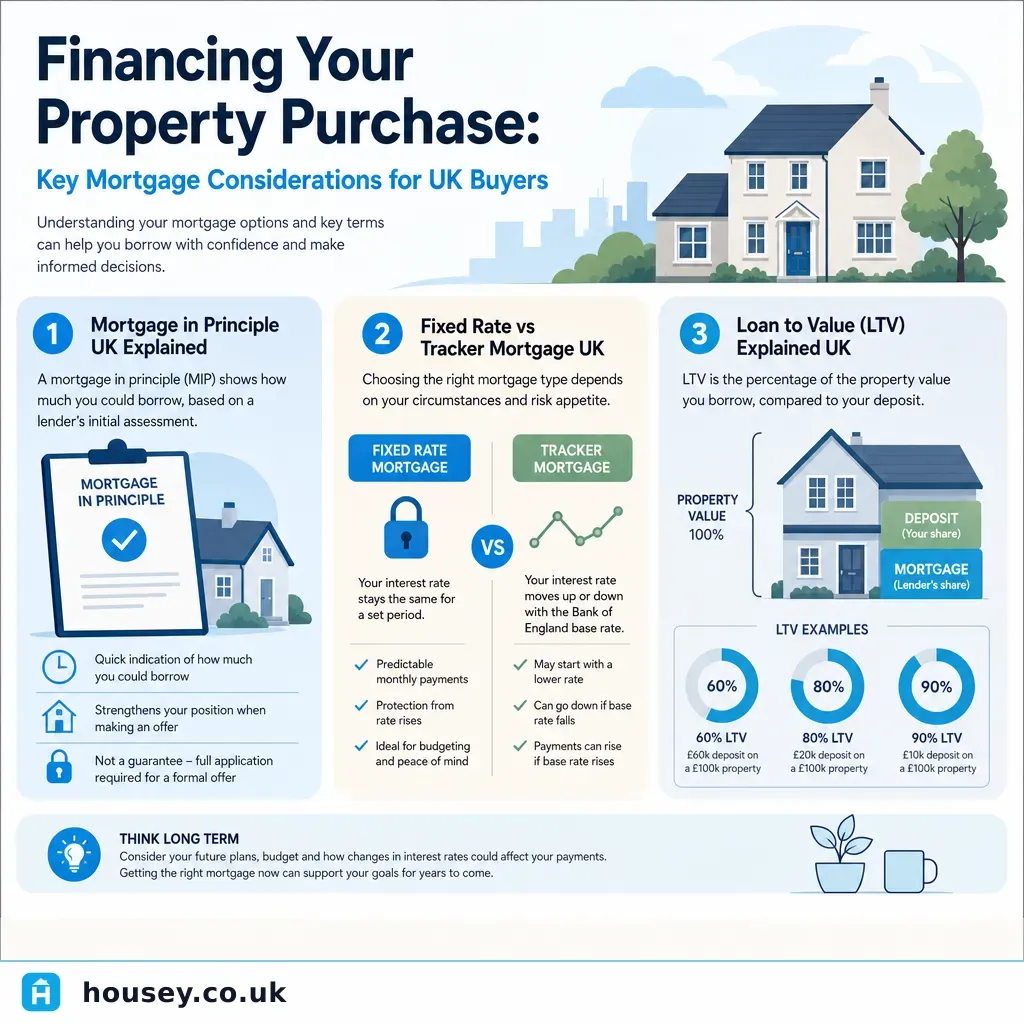

- A mortgage in principle (also called an Agreement in Principle or Decision in Principle) is not a formal offer; estate agents often require one before accepting offers on a property.

- Fixed-rate mortgage deals typically last 2, 3, or 5 years, after which you revert to the lender's Standard Variable Rate (SVR) unless you remortgage.

- The loan-to-value (LTV) ratio — the proportion of the property price you borrow — directly affects the interest rate you can access; lower LTV generally means better rates and more product choice.

- A lender-instructed valuation is separate from a RICS home survey; it protects the lender, not the buyer.

Mortgage types available to UK buyers

Mortgage type | How the rate works | Best for | Watch out for |

|---|---|---|---|

Fixed rate | Interest rate fixed for a set term (e.g. 2 or 5 years) | Buyers who want certainty on monthly payments | Early repayment charges if you sell or remortgage within the term |

Tracker | Tracks Bank of England base rate plus a margin | Buyers comfortable with rate changes; when base rate is expected to fall | Payments rise if base rate rises |

Discount variable | Lender's SVR minus a set percentage | Short-term certainty with some flexibility | SVR can change at any time; check the lender's history |

Offset | Links a savings account to the mortgage; interest calculated on balance minus savings | Higher earners with significant savings | Usually a higher headline rate; complexity in day-to-day management |

Standard Variable Rate (SVR) | Lender's default rate after an initial deal ends | Rarely best value; a fallback position only | Usually the highest rate available from that lender |

Loan-to-value and how it affects your mortgage

Your LTV is the loan amount as a percentage of the property's value. A property worth £300,000 with a £240,000 mortgage has an 80% LTV.

Most lenders offer their best rates at 60%, 75%, and 80% LTV thresholds. First-time buyers with a 5–10% deposit typically access products at 90–95% LTV, which carry higher rates and fewer available deals.

If a lender's own valuation comes in below the agreed purchase price, the effective LTV increases — sometimes pushing you into a higher-rate band or requiring a larger deposit than expected. This is one of the most common mid-transaction financial surprises, which is why arranging a valuation survey early in the process can be valuable.

What affects your mortgage eligibility

Income and employment: Employed applicants typically need 3 months' payslips and a P60. Self-employed applicants usually need 2–3 years of HMRC Self Assessment tax returns (SA302s) and corresponding tax year overviews. Zero-hours contracts, probationary periods, and recent career changes can all affect eligibility.

Credit history: Missed payments, defaults, County Court Judgements (CCJs), or Individual Voluntary Arrangements (IVAs) reduce the pool of available lenders and rates. Applying for new credit shortly before a mortgage application can temporarily lower your credit score.

Existing financial commitments: Student loans, car finance, personal loans, and credit card balances all feature in affordability assessments alongside income.

Deposit source: Lenders require evidence of where your deposit comes from. Gifted deposits from family members typically require a signed declaration from the donor confirming the money is a gift, not a loan.

The mortgage offer timeline

- Mortgage in principle (AIP/DIP): A soft or hard credit check; valid for 60–90 days; often required by estate agents before accepting offers.

- Full mortgage application: Submitted after offer accepted; lender instructs a valuation of the property.

- Lender valuation: Usually completed within 1–2 weeks; can delay the offer if the property is unusual or requires further assessment.

- Formal mortgage offer: Typically issued 2–4 weeks after full application, though complex cases take longer.

- Mortgage offer validity: Most offers are valid for 6 months (sometimes 3 months for new builds). If exchange does not happen within this period, you may need to re-apply.

What to ask before accepting a mortgage product

- What is the initial interest rate, and how long does it last?

- What is the lender's SVR once the deal ends?

- Are there early repayment charges, and if so, how much and for how long do they apply?

- What are the arrangement and product fees, and can I add them to the loan?

- What is the maximum overpayment I can make without triggering a charge?

- Is the product portable — can I transfer it to a new property if I move before the deal ends?

- What happens if interest rates change between my application and completion?

Important limitations

This article provides general information about UK mortgage products and the property buying process as of May 2026. Mortgage products, eligibility criteria, rates, and lender policies change frequently. Nothing here constitutes financial advice. Always speak to a qualified, FCA-authorised mortgage broker or independent financial adviser before making mortgage decisions. The right product depends on your personal circumstances, credit history, income structure, and the specific property you are buying.

When this becomes urgent

Seek professional advice without delay if:

- Your lender's valuation comes in significantly below the agreed purchase price, threatening your LTV ratio or requiring a larger deposit than you hold.

- Your mortgage offer expires before exchange of contracts, requiring a re-application with potential rate or criteria changes.

- You experience a change in employment, income, or credit status after submitting a full mortgage application.

- Your lender withdraws the mortgage offer due to a change in their lending criteria or your circumstances.

What to ask a qualified professional

Before instructing a mortgage broker or applying directly to a lender, ask:

- Are you a whole-of-market broker, or do you work with a panel of lenders only?

- Are you FCA-authorised, and what is your FCA registration number?

- How is your fee structured — fixed fee, percentage of the loan, or commission from the lender?

- What documentation will you need from me upfront?

- How long do you expect the application and formal offer process to take for my circumstances?

- What happens if my financial situation changes between application and completion?

When to get professional help

If your financial situation is complex — self-employment, multiple income streams, recent credit issues, a non-standard property type, or a high LTV requirement — a whole-of-market broker will have access to lenders and products not available directly. FCA-authorised mortgage brokers are regulated and must provide suitable advice. You can verify a broker's registration on the FCA Register at register.fca.org.uk.

If a lender's valuation comes in below the purchase price, seek advice from your broker and your conveyancing solicitor before deciding how to proceed.

How Housey can help

Housey connects homeowners with experienced conveyancing solicitors and providers of valuation surveys across the UK. A conveyancing solicitor works alongside your mortgage broker to ensure the legal and financial strands of your purchase progress in parallel, reducing the risk of delays at the critical exchange stage.

Frequently asked questions

How much can I borrow for a UK mortgage?

Most lenders use an income multiple of 4–4.5 times your annual gross salary, or combined salary for joint applications. Some lenders consider higher multiples for higher earners or certain professions. Affordability is assessed on your full financial picture — including existing debts, credit commitments, and outgoings — not just income alone.

How long does it take to get a mortgage offer?

From submitting a full application, most borrowers receive a formal mortgage offer within 2–4 weeks, though complex cases, unusual properties, or high lender volumes can extend this. A mortgage in principle can typically be obtained within 24–48 hours online or through a broker.

What is the difference between a mortgage valuation and a home survey?

A mortgage valuation is instructed by the lender to confirm the property is adequate security for the loan — it protects the lender, not you. A home survey such as a RICS Level 2 or Level 3 assesses the property's condition for your benefit and may identify defects affecting your purchase decision or negotiating position.

Can I get a mortgage if I am self-employed?

Yes, though lenders typically require 2–3 years of accounts or SA302 tax returns and corresponding tax year overviews from HMRC. Some lenders are more flexible than others for self-employed applicants; a whole-of-market mortgage broker can identify the most suitable products for your income structure.

Sources and further reading

- Mortgages: your rights as a consumer — Financial Conduct Authority

- Buying a home: mortgages explained — MoneyHelper

- Stamp Duty Land Tax — GOV.UK

- Monetary policy: Bank Rate — Bank of England

- RICS Home Survey Standard — Royal Institution of Chartered Surveyors

Useful next reads

Buying & Moving

Buying & MovingCommon Legal Questions From Property Purchasers and Legal Advisors

Conveyancing in England and Wales typically takes 8–16 weeks.

Buying & Moving

Buying & MovingFirst-Time Buyer Essentials Checklist

Buying your first home involves obtaining a mortgage in principle, making an offer, instructing a solicitor, arranging a survey, and exchanging contracts before completion.

Buying & Moving

Buying & MovingIdentifying and Resolving Delays in Property Transactions

Delays in UK property transactions most often arise from slow local authority searches, incomplete identity documents, mortgage hold-ups, leasehold complications, or a problem elsewhere in the chain.

Buying & Moving

Buying & MovingWhen to Engage a Structural Engineer During Home Purchase

Instruct a structural engineer before exchange if your RICS survey flags movement, cracking rated condition 3, or suspected subsidence.

Buying & Moving

Buying & MovingUnderstanding Property Conveyancing in England and Wales

Conveyancing is the legal process of transferring property ownership in England and Wales.