First-Time Buyer Properties: Finding Your First Home

By Housey · Last reviewed 18th of May 2026

First-Time Buyer Properties: Finding Your First Home

Buying your first home in the UK involves overlapping decisions about budget, schemes, legal process, and property condition that often arrive simultaneously. The regulatory framework for first-time buyers — tax reliefs, government lending support, and survey requirements — has changed substantially since 2022, and eligibility rules are more nuanced than headlines suggest. Understanding what applies to your specific circumstances before you begin searching will save time and reduce the risk of a costly mistake later in the process.

Key points

- First-time buyers in England pay no Stamp Duty Land Tax (SDLT) on the first £300,000 of a purchase price (as of 1 April 2025, when the temporary £425,000 threshold expired); separate tax rules apply in Scotland (LBTT) and Wales (LTT).

- The Lifetime ISA (LISA) allows eligible first-time buyers to save up to £4,000 per year and receive a 25% government bonus (up to £1,000 per year) toward a first home purchase; the property must cost no more than £450,000.

- You are only a first-time buyer for HMRC purposes if you have never previously owned a residential property anywhere in the world — not just in the UK.

- A mortgage lender's valuation does not assess the condition of the property; you must commission a separate RICS survey if you want a structural and condition report.

- An Energy Performance Certificate (EPC) must be provided by the seller before marketing; a rating below E makes the property unlettable if you later wish to rent it out.

What counts as a first-time buyer in the UK?

For SDLT relief purposes, HMRC defines a first-time buyer as someone who has never previously owned, or had a legal interest in, a residential property anywhere in the world. This means:

- If you buy jointly with a partner who has previously owned property, neither of you qualifies for first-time buyer SDLT relief on that purchase.

- Inheriting a property counts as having owned one, even if you never lived there.

- Having owned property overseas disqualifies you.

- Being named on a mortgage as a guarantor (but not as a legal owner) does not usually affect eligibility — but confirm this with your conveyancer.

Always verify your first-time buyer status with your solicitor or conveyancer before relying on a tax relief.

Government schemes for first-time buyers

The landscape of first-time buyer support in England has shifted significantly since 2022. Check GOV.UK for current availability before making decisions based on any scheme.

Scheme | How it works | Key eligibility rules | Current status |

|---|---|---|---|

Lifetime ISA (LISA) | Save up to £4,000/year; government adds 25% (up to £1,000/year) | Must be 18–39 to open; property must cost ≤£450,000; must have held for 12 months | Available — check GOV.UK |

Shared Ownership | Buy a share (usually 10–75%) and pay subsidised rent on the rest; staircase to full ownership over time | Household income typically ≤£80,000/year (≤£90,000 in London) | Available via housing associations — check GOV.UK |

First Homes | New-build homes at a minimum 30% discount on open market value | Local connection or key worker priority in many areas; resale restrictions apply | Available in some developments — check with local planning authority |

Mortgage Guarantee Scheme | Government guarantee enabling lenders to offer 95% LTV mortgages to buyers with 5% deposits | Check GOV.UK for current availability and participating lenders | Check GOV.UK for current status |

Help to Buy Equity Loan | Government lent up to 20% (40% in London) of property value interest-free for five years | Closed to new applicants March 2023 — no longer available | Closed |

Which property type suits your first purchase?

- Choose a leasehold flat if you need to maximise budget in a city and are comfortable paying service charges. Check the lease length carefully — fewer than 80 years remaining can affect mortgage lending and future saleability, and extension costs rise sharply below this threshold.

- Choose a freehold house if you prefer to own the land, want more control over external works, and your budget extends to it. Freehold avoids the ongoing lease and service-charge obligations of leasehold.

- Choose a new-build if you want a chain-free purchase, modern energy efficiency ratings, and the reassurance of a 10-year structural warranty such as NHBC Buildmark — but be prepared to pay a premium over comparable second-hand stock.

- Choose an older terraced or semi-detached property if you want more space for your budget and are prepared for some ongoing maintenance. A survey is particularly important for pre-1980s properties.

- Ask a RICS surveyor before proceeding if the property shows signs of damp, cracks, past alterations, or unusual construction — defects discovered after exchange can be very costly to address.

- Check with your conveyancer if the property is leasehold, has a short lease, or involves shared ownership — the legal complexity differs from a straightforward freehold purchase.

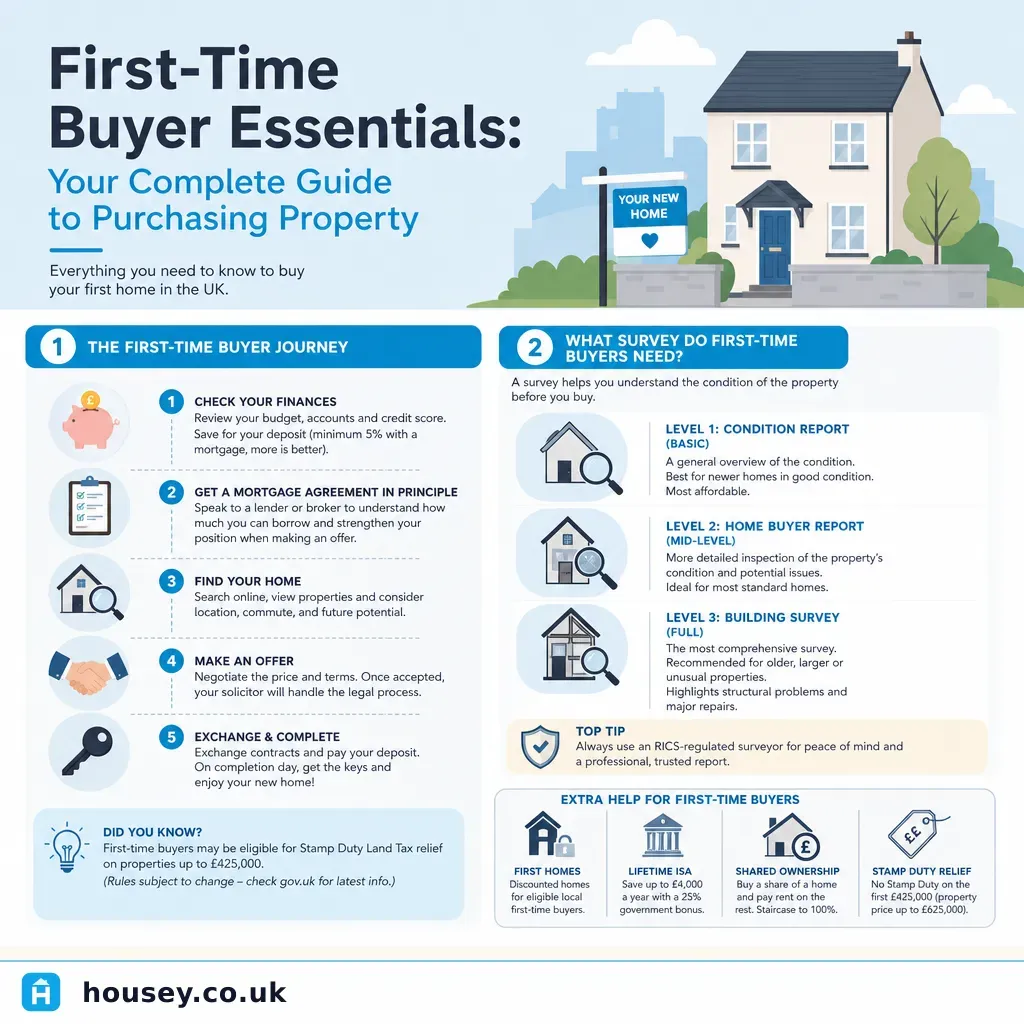

What surveys do first-time buyers need?

A mortgage lender's valuation is a brief inspection to confirm the property is worth the purchase price — it is not a condition report and will not reveal structural defects. You should commission a separate survey depending on the property's age and condition.

- RICS Level 1 (Condition Report): Basic traffic-light condition ratings with no detailed advice on repairs. Suited to modern, conventional properties in good condition with no visible defects.

- RICS Level 2 (Home Survey): Identifies material defects, gives maintenance advice, and highlights issues requiring further investigation. The most common choice for first-time buyers purchasing mainstream properties, including older homes in reasonable condition.

- RICS Level 3 (Building Survey): Full structural analysis with detailed defect descriptions and repair options. Recommended for Victorian or Edwardian properties, any home with visible damp or cracking, or properties that have had significant alterations.

Never skip a survey to save money at the purchase stage. The cost of a survey is small compared to discovering a structural defect after exchange.

First-time buyer checklist

Use this checklist to track your progress from preparation through to exchange:

Important limitations

This article provides general information about first-time buyer options in England. Rules differ in Scotland (Land and Buildings Transaction Tax applies instead of SDLT), Wales (Land Transaction Tax applies), and Northern Ireland (separate property law system). Scheme eligibility rules, tax thresholds, and government programmes change regularly. Nothing in this article constitutes legal, financial, or tax advice. Always confirm your eligibility and specific circumstances with a qualified solicitor or conveyancer and, where mortgage decisions are involved, a regulated independent financial adviser.

What to ask a qualified professional

Ask your solicitor or conveyancer:

- Do I qualify for first-time buyer SDLT relief based on my specific circumstances?

- Is there anything in the title register or leasehold documentation that could affect the property's use or future saleability?

- What is the remaining lease term, and are there any planned major works, service charge disputes, or ground rent review clauses?

Ask a mortgage broker:

- Which lenders will accept my income type and deposit size?

- Am I eligible for any first-time buyer mortgage products or guarantee schemes?

- How does my Lifetime ISA interact with the mortgage product I am considering?

Ask a RICS surveyor:

- What survey level do you recommend for this specific property, and why?

- Did the inspection reveal any defects that require specialist investigation before I exchange contracts?

When to get professional help

You will need professional help at several stages of a first-time purchase — conveyancing and mortgage advice are not optional. Instruct a surveyor if you notice any of the following during viewings:

- Cracks in internal or external walls, particularly diagonal cracks through brickwork

- Damp patches, staining, or a persistent musty smell

- Evidence of roof damage or sagging roof lines

- Signs of past flooding such as tide marks or recent replastering at low level

- Bowing or bulging brickwork

- Significant extensions or alterations without visible documentation

How Housey can help

Housey can connect you with qualified professionals at every stage of your first purchase — compare quotes for a conveyancing solicitor or licensed conveyancer, book a RICS Level 2 survey for mainstream properties, or commission a valuation survey to confirm the purchase price is fair. You can also check what an Energy Performance Certificate (EPC) means for a property's running costs and future compliance.

Frequently asked questions

Can I use a Lifetime ISA toward any property?

A Lifetime ISA can be used toward a first residential property costing up to £450,000. You must have held the account for at least 12 months before using it. Using funds for any other purpose before age 60 incurs a 25% withdrawal penalty, which effectively removes the government bonus plus a proportion of your own savings. Check GOV.UK for full current terms.

What is an Agreement in Principle and do I need one before making an offer?

An Agreement in Principle (AIP) — sometimes called a Decision in Principle — is a conditional indication from a lender of how much they may be willing to lend. Estate agents often ask for one before accepting an offer. Getting an AIP is free and does not bind you to a lender, though some involve a credit check that may leave a soft or hard footprint on your credit file.

What is leasehold reform and does it affect my purchase?

The Leasehold and Freehold Reform Act 2024 introduced changes to leasehold properties in England and Wales, including changes to enfranchisement valuations and lease extension rights. Legislation is being implemented in stages. Confirm the current position with your conveyancer before purchasing a leasehold property, particularly if the lease has fewer than 85 years remaining.

What are the typical legal fees for a first-time buyer?

Indicative UK costs, last reviewed 2026-05-18. Conveyancing fees for a purchase typically range from £1,000 to £2,500 including disbursements such as search fees, Land Registry fees, and bank transfer charges. Quotes vary significantly — compare at least three before instructing. VAT is charged on legal fees.

Do I need a solicitor or can I use a licensed conveyancer?

Both are authorised to conduct residential conveyancing in England and Wales. Solicitors are regulated by the Solicitors Regulation Authority (SRA); licensed conveyancers are regulated by the Council for Licensed Conveyancers (CLC). For a straightforward purchase, a licensed conveyancer can be equally effective and sometimes less expensive. For complex transactions — short leases, shared ownership, unregistered title — a solicitor with relevant property experience may be preferable.

Sources and further reading

- Stamp Duty Land Tax relief for first-time buyers — GOV.UK

- Lifetime ISA — GOV.UK

- Affordable home ownership schemes — GOV.UK

- RICS Home Survey Standard — RICS

- Leasehold and Freehold Reform Act 2024 — legislation.gov.uk

- Buying a home — Citizens Advice

Useful next reads

Buying & Moving

Buying & MovingGovernment Property Support Schemes: Help to Buy Eligibility and Benefits

Help to Buy: Equity Loan in England closed in March 2023 and is no longer available to new buyers.

Buying & Moving

Buying & MovingFirst-Time Buyer Essentials: Your Complete Guide to Purchasing Property

Buying your first UK home involves six key stages: securing a mortgage Agreement in Principle, making an offer, instructing a solicitor, commissioning an independent RICS survey, exchanging contracts (the legally binding point), and completing.

Buying & Moving

Buying & MovingGovernment-backed property schemes: support programmes for first-time home buyers

UK first-time buyers can access several government-backed programmes including the Lifetime ISA (25% bonus on savings up to £4,000 per year), Shared Ownership (part-buy, part-rent), and the First Homes scheme (discounts of 30–50% on new builds).

Buying & Moving

Buying & MovingThe Complete Property Buying Guide: From Search to Purchase

Buying a property in England and Wales typically takes 3–6 months from accepted offer to completion.

Buying & Moving

Buying & MovingShared Ownership vs Renting: Making the Right Choice for You

Shared ownership lets you buy a share of a property — typically 10% to 75% — and pay subsidised rent on the rest, building equity over time.