First-Time Homebuyer's Guide to Moving and Property Inspections

By Housey · Last reviewed 18th of May 2026

First-Time Homebuyer's Guide to Moving and Property Inspections

Buying your first home in the UK means navigating two parallel tracks simultaneously: the legal and financial process of acquiring the property, and the practical task of organising your move. Most first-time buyers underestimate how early decisions — particularly around surveys and conveyancing — can affect the cost, timeline, and outcome of the purchase. The stakes are high: once you exchange contracts in England and Wales, withdrawing means losing your deposit.

Key points

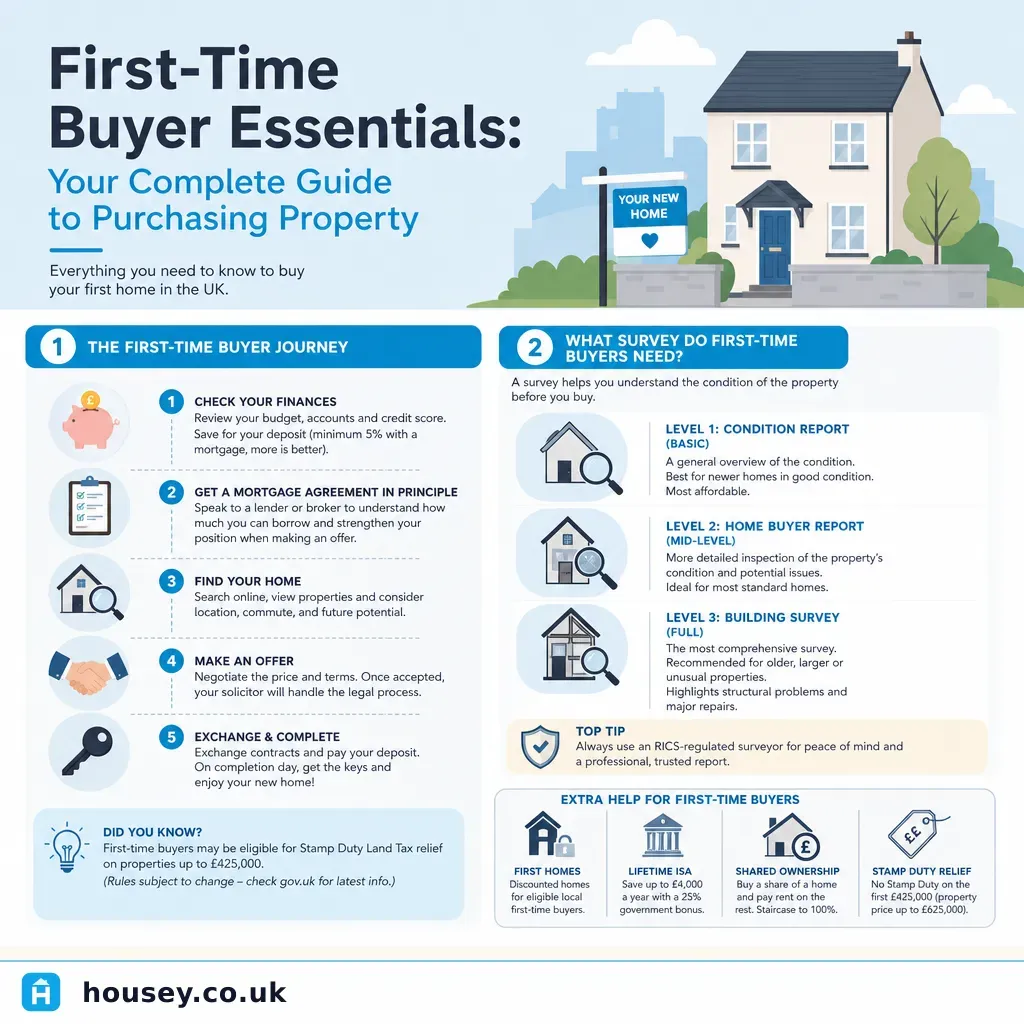

- A mortgage lender's valuation is not a property survey — it confirms the property is worth the loan amount to the lender, not that the building is in sound condition; instructing your own RICS Home Survey is strongly recommended for every purchase.

- RICS Home Surveys are offered at three levels: Level 1 (condition report), Level 2 (home survey), and Level 3 (building survey); the right choice depends on the property's age, construction, and condition.

- In England and Wales, exchange of contracts is the legally binding commitment — once exchanged, a buyer who withdraws loses their deposit, typically 10% of the purchase price.

- First-time buyers in England benefit from Stamp Duty Land Tax (SDLT) relief on purchases up to £500,000; check GOV.UK for current thresholds, which have changed in recent Budgets.

- Keys on completion day are typically not released until solicitors confirm funds have cleared — often early-to-mid afternoon — so plan removal bookings with flexibility built in.

Understanding property surveys as a first-time buyer

The single most common mistake first-time buyers make is treating the mortgage valuation as a property inspection. They serve entirely different purposes.

Lender's valuation vs RICS Home Survey

| Lender's valuation | RICS Level 2 Survey | RICS Level 3 Survey |

|---|---|---|---|

Purpose | Confirms property is suitable security for the loan | Assesses condition; flags defects with traffic-light ratings | In-depth assessment of condition, construction, and defects |

Who it protects | The lender | The buyer | The buyer |

Typical indicative cost (2026-05-18) | Often included in mortgage or £150–£400 | £400–£900 | £630–£1,500+ |

Defect advice included? | No | Yes | Yes — with detailed commentary |

Best suited to | All mortgage applications | Conventional post-1930s homes in reasonable condition | Older, larger, unusual, or visibly defective properties |

Indicative UK costs, last reviewed 2026-05-18. Costs vary by property size, type, and location.

Which survey should a first-time buyer choose?

Use this decision tree to identify the most suitable starting point:

- Post-1930s estate house or modern flat, conventional construction, no visible defects → RICS Level 2 Home Survey is usually sufficient.

- Victorian or Edwardian terrace, pre-1919 solid-wall construction, or any property with visible damp, cracks, or evidence of past alterations → RICS Level 3 Building Survey is more appropriate.

- Brand-new property from a developer → An independent snagging survey is strongly recommended alongside the developer's own sign-off; a snagging inspector is not the same as a RICS surveyor.

- Property with a specific visible defect — cracked brickwork, uneven roofline, sticking doors — → Consider instructing a structural engineer's report alongside or instead of a general survey.

- Leasehold flat → Clarify with the surveyor what is and is not in scope; a Level 2 survey on a flat typically covers the interior but may not assess the roof or external structure unless specifically instructed.

The conveyancing process

Conveyancing is the legal transfer of property ownership. In England and Wales, it typically runs from offer acceptance to completion in 8–16 weeks, though chain length, mortgage complexity, and title issues can extend this considerably.

Key stages:

- Instruct a conveyancer — as soon as your offer is accepted; do not wait for the survey results.

- Searches — your conveyancer orders local authority, water, drainage, and environmental searches. These take one to six weeks depending on the local authority.

- Mortgage offer — your lender instructs a valuation and, once satisfied, issues a formal mortgage offer. Check the offer carefully against the actual property.

- Exchange of contracts — the legally binding step. Your deposit (usually 10%) is transferred. A completion date is agreed. You cannot withdraw without financial penalty after this point.

- Completion — remaining funds are transferred via solicitors; keys are released once the seller's solicitor confirms receipt.

Coordinating your move with completion day

Completion day in a chain rarely runs to an exact schedule. Each linked buyer and seller must complete in sequence before the next can proceed, so key release often falls in the early-to-mid afternoon.

Practical steps for first-time buyers:

- Book a removal company provisionally as soon as you have an expected completion date, but wait until after exchange to confirm on a fixed date.

- Ask your conveyancer to call or message you as soon as funds are confirmed on the day.

- Have a contingency plan if the chain is delayed — most removal companies can hold a van if given early notice.

- Do not arrange utility switchovers, deep cleans, or tradespeople for the property on completion day unless you have confirmed access time with your conveyancer.

Important limitations

This article provides general information only. Property law, conveyancing processes, SDLT rates, lender requirements, and survey recommendations vary by property and individual circumstance, and can change. Nothing in this article constitutes legal advice. Always instruct a conveyancer regulated by the Solicitors Regulation Authority (SRA) or the Council for Licensed Conveyancers (CLC) for legal work, and a RICS-registered surveyor for any property assessment. The right survey type for your purchase depends on the specific property's age, construction, and condition — a guide cannot replace a professional assessment.

What to ask a qualified professional

Questions for your conveyancer

- What searches will you order, and are there known local issues — flood risk, mining history, or planning constraints — I should be aware of for this area?

- Are you on my mortgage lender's approved conveyancer panel? If not, the lender may instruct their own solicitor at additional cost.

- What are your total fees including all disbursements, searches, and Land Registry fees — and is VAT included?

- What is your typical communication turnaround time, and will I have a named contact throughout the transaction?

- What happens if the seller withdraws after exchange of contracts — how does the deposit protection work?

Questions for your surveyor

- What level of survey do you recommend for this specific property type, age, and condition, and why?

- Does the survey include the roof, loft space, and visible structure — or only the interior?

- If you find a significant defect, will you recommend a specialist report before I exchange contracts?

- How quickly will I receive the report, and will you be available to discuss the findings?

- Are you RICS-registered and does your firm carry professional indemnity insurance?

When to get professional help

A regulated professional is non-negotiable in the following situations:

- Before exchanging contracts — a RICS-registered surveyor for the inspection and an SRA or CLC-regulated conveyancer for the legal work are both essential, not optional

- If the survey flags a serious defect — structural movement, damp penetration, roof failure, or drainage problems — instruct a specialist engineer or obtain a specialist report before proceeding; do not exchange blind

- If the lease on a leasehold property is under 80 years — leasehold extension law is complex and significantly affects value; instruct a specialist conveyancer and consider engaging a RICS-registered valuer

- If you are buying a listed building — seek a heritage architect or specialist surveyor alongside a conveyancer experienced in listed property transactions

- If SDLT liability is complex — for example, shared ownership, mixed-use property, or Help to Buy — take specific tax advice rather than relying on a general guide

How Housey can help

Housey connects first-time buyers with RICS-registered surveyors for RICS Home Surveys and valuation surveys, regulated solicitors for conveyancing, and vetted removal companies. You can compare quotes from multiple providers and get guidance on which services you need, all from a single platform.

Frequently asked questions

Do I need a survey if the lender arranges a valuation?

Yes. The lender's valuation is conducted for the lender's protection, not yours. It will not identify structural defects, damp, roof deterioration, or condition issues that could cost you thousands to remedy after purchase. Instructing your own RICS-registered surveyor is strongly recommended for any property, and is particularly important for older, larger, or non-standard construction.

Can I use survey results to renegotiate the asking price?

Yes, this is common practice. If a survey reveals significant defects not reflected in the asking price, buyers often renegotiate the price or ask the seller to remedy defects before completion. Your conveyancer or estate agent can manage the conversation. Sellers can decline, at which point you can proceed with full knowledge of the defects, withdraw, or seek a specialist's assessment of remediation costs.

How long before completion should I book a removal company?

Book provisionally as soon as you have an expected completion date — typically around the time exchange is approaching. Confirm the booking once exchange has taken place and a firm date is agreed. During peak periods such as July and August or school half-terms, booking earlier reduces the risk of preferred companies being fully committed.

What is a snagging survey on a new-build property?

A snagging survey identifies cosmetic and minor construction defects in a new-build, carried out by an independent inspector before or shortly after legal completion. It provides a documented list to take to the developer. Most reputable builders address genuine defects under the NHBC Buildmark warranty or equivalent scheme, though they are not legally obliged to respond to every item on the list.

Sources and further reading

- Buying a home: surveys and reports — GOV.UK

- RICS Home Survey Standard — RICS

- Stamp Duty Land Tax for first-time buyers — GOV.UK

- Buying a home — Citizens Advice

- Conveyancing: the legal process of buying and selling property — GOV.UK

Useful next reads

Buying & Moving

Buying & MovingFirst-Time Buyer Essentials: Your Complete Guide to Purchasing Property

Buying your first UK home involves six key stages: securing a mortgage Agreement in Principle, making an offer, instructing a solicitor, commissioning an independent RICS survey, exchanging contracts (the legally binding point), and completing.

Buying & Moving

Buying & MovingFirst-Time Homebuyer: Essential Guidance for UK Property Purchase

Buying your first home in the UK involves securing a mortgage in principle, making an offer, instructing a solicitor for conveyancing, commissioning a RICS Home Survey, then exchanging and completing contracts.

Buying & Moving

Buying & MovingEssential guidance for first-time property owners in the UK

As a new UK homeowner, your first responsibilities are buildings insurance from exchange, utility transfers, council tax registration, and gathering key documents including the title register and EPC.

Buying & Moving

Buying & MovingFirst-Time Buyer Guide: Key Steps for Purchasing Your Home in the UK

Buying your first home in England or Wales involves securing a mortgage in principle, instructing a solicitor early, commissioning your own survey separately from the lender's valuation, and understanding that the purchase is not legally binding until exchange of contracts.

Buying & Moving

Buying & MovingFirst-time home buyer guide: essential property services and purchasing checklist

Buying your first home in the UK typically takes 12–16 weeks from offer acceptance to completion.