First-Time Buyer Guide: Expert Advice for Your Property Purchase

By Housey · Last reviewed 10th of May 2026

First-Time Buyer Guide: Expert Advice for Your Property Purchase

Navigating your first property purchase in England or Wales means working through a sequence of legal, financial, and structural decisions that most buyers encounter for the first time simultaneously. The process typically begins months before you view a single property and runs through to the day you collect the keys — with several points where the wrong decision can cost thousands of pounds or cause significant delays. Understanding what each stage involves, which professionals to instruct, and what to watch for gives you a meaningful advantage in a competitive market.

Key points

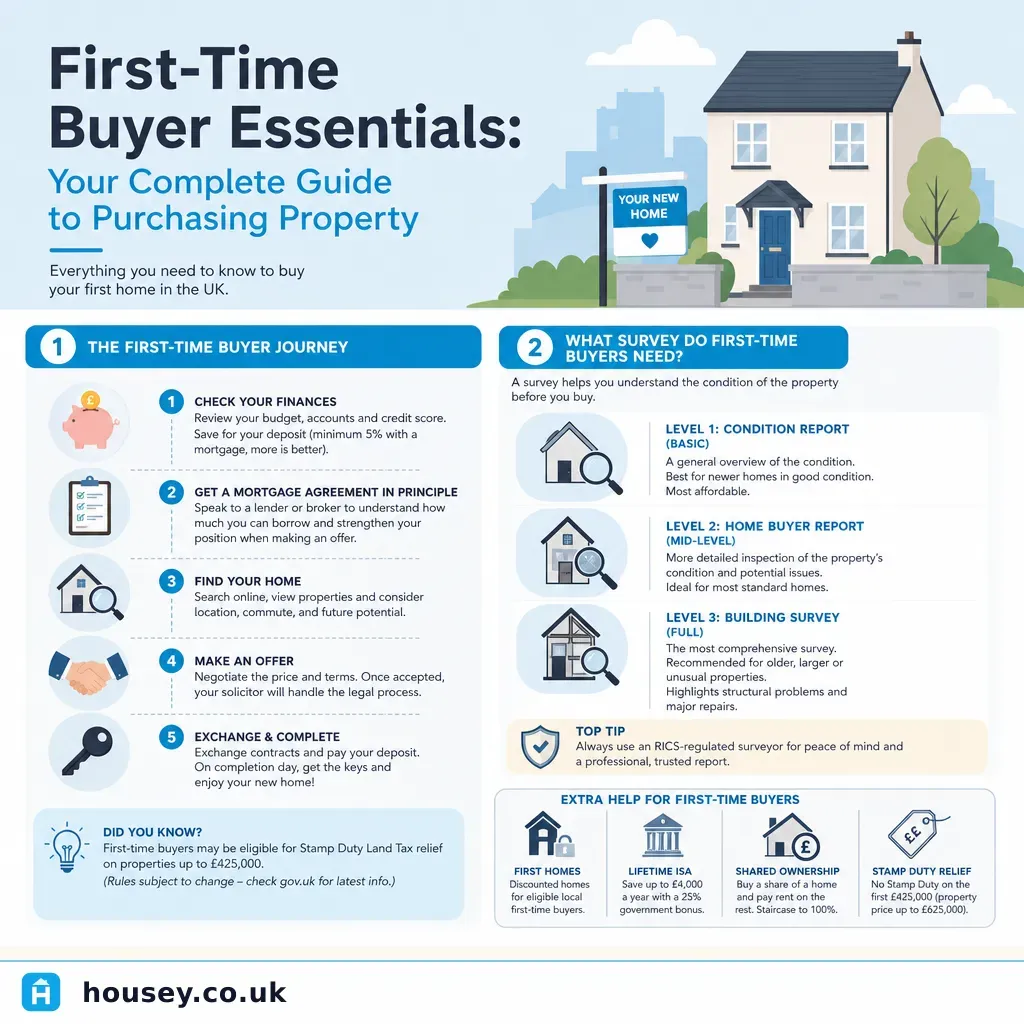

- First-time buyer Stamp Duty Land Tax (SDLT) relief applies on properties up to £500,000, with no SDLT payable on the first £300,000 of the purchase price (as of 1 April 2025, when the temporary higher £425,000 nil-rate threshold ended).

- A Lifetime ISA (LISA) pays a 25% government bonus — up to £1,000 per year — on savings used toward a first home worth £450,000 or less; the account must be open for at least 12 months before use.

- Exchange of contracts is the point at which the transaction becomes legally binding; either party withdrawing after exchange is liable for substantial financial penalties.

- A mortgage in principle (Agreement in Principle) is not a binding mortgage offer and may be revised after full application and credit checks.

- The Property Information Form (TA6) completed by the seller covers disputes, alterations, and known defects — review it carefully before exchange and raise any unclear points with your conveyancer.

Understanding your budget before you start viewing

Before registering with estate agents, establish what you can borrow and what your total buying costs will be — including costs beyond the purchase price itself.

Typical buying costs to budget for:

- SDLT: First-time buyers pay no SDLT on the first £300,000 of a qualifying property purchase (properties up to £500,000). Between £300,001 and £500,000 the rate is 5%. Properties above £500,000 do not qualify for first-time buyer relief. Check the GOV.UK SDLT calculator for your specific purchase price.

- Conveyancing fees: Typically £1,000–£2,500 including disbursements (searches, Land Registry fees), depending on property value and complexity.

- Survey fees: From approximately £400–£500 for a RICS Level 2 Home Survey to £600–£1,500 or more for a Level 3 Building Survey, depending on property size and location.

- Mortgage arrangement fees: Many products charge £500–£2,000, which can often be added to the loan (though interest then accrues on that amount).

- Buildings insurance: Required from exchange of contracts.

Indicative UK costs, last reviewed 2026-05-10. Actual figures vary by property, location, and provider.

A Lifetime ISA is worth considering if you have not yet saved your full deposit. You can contribute up to £4,000 per year and receive a 25% bonus from HMRC — up to £1,000 annually — provided the property costs £450,000 or less and the account has been open for at least 12 months. Withdrawing funds for any purpose other than first home purchase or retirement before age 60 incurs a withdrawal penalty. See GOV.UK Lifetime ISA guidance for current rules.

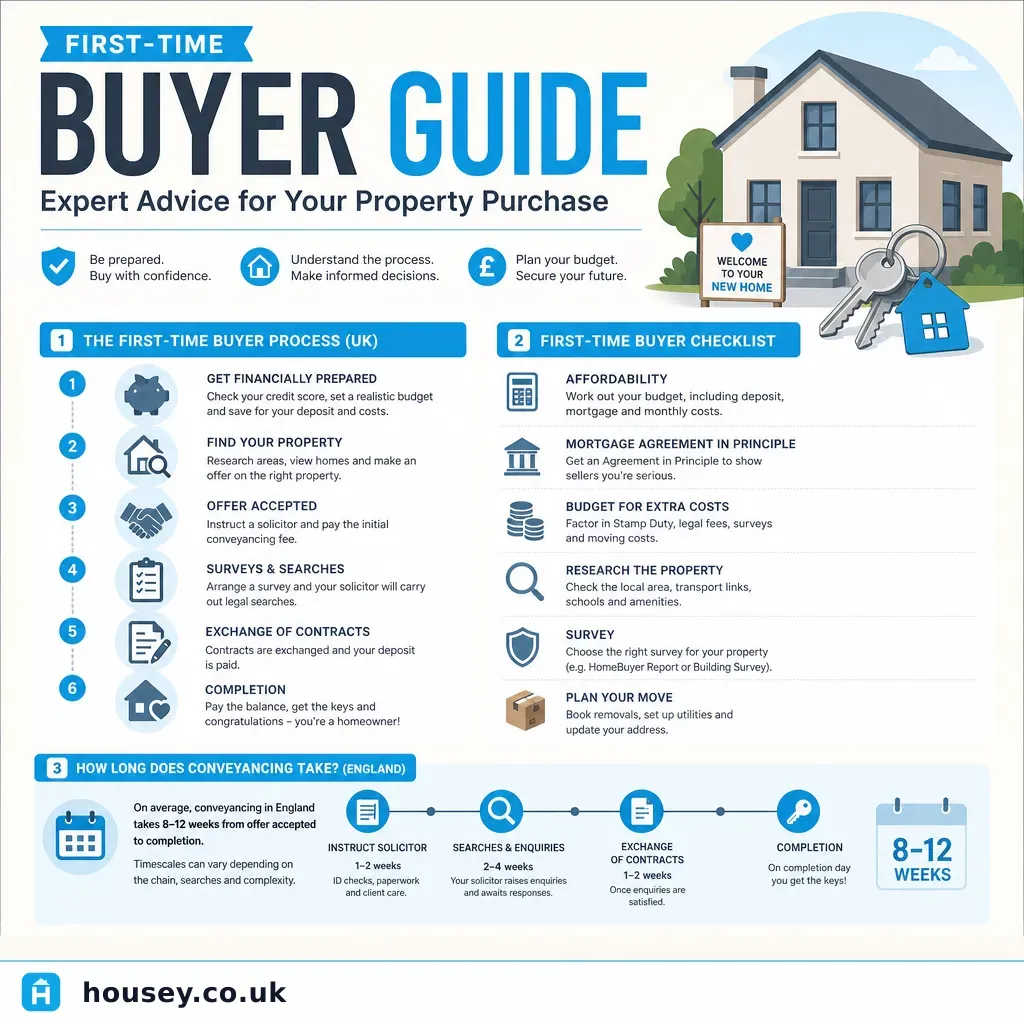

The offer-to-completion process: key stages

1. Mortgage in principle

Before making a formal offer, obtain a mortgage in principle (AIP) from a lender or mortgage broker. An AIP confirms a lender is likely to lend you a stated amount, but it is not a binding offer. Confirm with your broker whether the AIP involves a hard or soft credit search, as a hard search leaves a footprint on your credit file.

2. Making an offer and instructing professionals

In England and Wales, an accepted offer is not legally binding on either party — either side can withdraw before exchange without penalty, though you lose any survey or search costs incurred. Instruct a conveyancer or solicitor promptly once your offer is accepted, and commission a RICS survey before exchange to identify any structural or condition issues.

3. Conveyancing: searches and enquiries

Your conveyancer will carry out searches (local authority, drainage, environmental, and others as relevant), raise enquiries with the seller's solicitor, and review the title deeds and contract. This stage typically takes 8–12 weeks, though complex chains or slow local authority searches can extend it to four months or more.

4. Choosing the right survey

A survey is not the same as a mortgage valuation. The lender's valuation is conducted for the lender's benefit only — to confirm the property provides adequate security for the loan. A RICS Home Survey is conducted for your benefit and gives you a view of the property's condition before you are legally committed.

Survey type | Best for | Not ideal for | Typical output |

|---|---|---|---|

RICS Level 2 Home Survey | Conventional homes built after approximately 1900 in reasonable condition, standard construction | Pre-1900 homes, visibly defective, altered, or unusual properties | Traffic-light condition ratings, key risks, legal issues flagged |

RICS Level 3 Building Survey | Pre-1900 homes, unusual construction, properties with visible defects, extensions, or significant alterations | Straightforward modern homes where Level 2 is usually sufficient and proportionate | Detailed defect analysis, causes identified, estimated repair costs (often optional extra) |

Structural engineer's report | Where a specific structural concern — cracking, movement, suspected subsidence — is identified | General condition assessment; not a substitute for a RICS survey | Specific engineering assessment, remedial recommendations |

Check your surveyor's registration via RICS Find a Surveyor before instructing.

5. Exchange and completion

Exchange makes the transaction legally binding. Both parties sign identical contracts and the buyer transfers a deposit — typically 10% of the purchase price — to their solicitor. Completion, usually one to four weeks after exchange, is when the remaining funds transfer and you legally become the owner.

First-time buyer checklist

Use this at each stage to avoid common oversights.

Before making an offer:

After offer accepted:

Before exchange:

Before completion:

Red flags to watch for during the buying process

Several situations should prompt you to pause and seek advice before proceeding:

- Survey flags a Condition Rating 3 defect: Serious or urgent findings require specialist follow-up before exchange — from a structural engineer, damp specialist, or roofing contractor depending on the issue type.

- Seller cannot provide key documentation: Missing FENSA certificates (replacement windows), building regulations completion certificates, or planning permissions for extensions can create complications at remortgage or future sale.

- Title issues raised by your conveyancer: Restrictive covenants, uncertain boundaries, or rights of way require clear explanation before exchange, and may require specialist legal advice.

- Pressure to exchange without a completed survey: Urgency should not override prudent due diligence.

- The property has fallen through with previous buyers: Ask the estate agent why earlier sales did not proceed — the answer can be instructive.

- Leasehold with a short lease: Leases below approximately 80 years can make a property harder to mortgage and more expensive to extend. Check the lease length early in the process.

Important limitations

This article provides general information about the first-time buyer process in England and Wales. Rules differ in Scotland (where the seller provides a Home Report before marketing) and Northern Ireland. SDLT thresholds, mortgage criteria, government scheme eligibility, and planning rules can change. Nothing in this guide constitutes legal, financial, structural, or surveying advice. A qualified conveyancer, independent mortgage adviser, and RICS-registered surveyor should be consulted for advice specific to your property and personal circumstances.

What to ask a qualified professional

Mortgage broker or independent financial adviser:

- Are there first-time buyer mortgage products or government schemes I should consider for my situation?

- What is the total cost of this mortgage over its full term, including all fees and charges?

- How will this mortgage affect my ability to overpay, remortgage early, or move within five years?

Conveyancer or solicitor:

- What do the search results show, and are any results unusual for this area or property type?

- Are there title issues I should understand before exchange?

- What does the seller's Property Information Form reveal about alterations, disputes, or known defects?

- Are there any restrictions on what I can do with this property?

RICS surveyor:

- What is the most serious defect identified, and what does it indicate about the property's overall condition?

- Is there anything in this report that would affect your view of the agreed purchase price?

- Which defects are urgent and which are long-term maintenance items I can address in time?

When to get professional help

If your survey contains a Condition Rating 3 finding (serious or urgent defect), seek specialist advice from a structural engineer, damp specialist, or roofing contractor before exchange. If your conveyancer raises a title issue that requires specialist legal input, instruct them to obtain it before you proceed. For mortgage or financial questions, an FCA-regulated independent mortgage adviser provides personalised guidance that a lender's own sales team cannot.

How Housey can help

Housey connects first-time buyers with qualified UK professionals at each stage of the purchase process. You can request quotes from RICS-regulated home surveyors for a Level 2 or Level 3 survey, find conveyancing solicitors for the legal transfer, or locate a RICS Level 2 survey specialist if you are purchasing a conventional property in reasonable condition.

Frequently asked questions

Do I need a survey if I am getting a mortgage?

Your lender will commission a mortgage valuation for their own protection, but this rarely identifies defects and gives you limited recourse if problems emerge later. A separate RICS Home Survey — Level 2 or Level 3 depending on the property — is strongly recommended for your own protection before exchange of contracts.

How long does conveyancing take in England?

Most straightforward conveyancing takes 8–12 weeks from offer acceptance to exchange. Complex chains, leasehold properties, slow local authority searches, or title issues can push this to four months or more. Scotland uses a different system where the seller provides a Home Report before the property goes on the market.

Can a sale fall through after exchange of contracts?

No — exchange makes the contract legally binding on both parties. A buyer who withdraws after exchange forfeits their deposit. A seller who withdraws is liable for damages. Before exchange, either party can withdraw without legal penalty, though you may lose survey and conveyancing search costs already incurred.

What is a completion date?

Completion is the day the remaining purchase funds transfer from your solicitor to the seller's solicitor, and you legally become the owner. Keys are released once your solicitor confirms funds are received. The completion date is usually agreed at the point of exchange and is typically one to four weeks later.

Should I use a local conveyancer or an online firm?

You are not required to use a local firm. Online conveyancers can be lower cost. What matters most is that the firm is regulated by the Solicitors Regulation Authority (SRA) or the Council for Licensed Conveyancers (CLC), communicates clearly and promptly, and has experience with your property's tenure — particularly important for leasehold properties.

Sources and further reading

- Stamp Duty Land Tax: first-time buyers relief — HM Revenue & Customs

- Lifetime ISA — HM Revenue & Customs / GOV.UK

- Buying or selling your home — Citizens Advice

- RICS Home Surveys — Royal Institution of Chartered Surveyors

- How to buy a home — Money and Pensions Service (Money Helper)

Useful next reads

Buying & Moving

Buying & MovingFirst-Time Buyer Essentials: Your Complete Guide to Purchasing Property

Buying your first UK home involves six key stages: securing a mortgage Agreement in Principle, making an offer, instructing a solicitor, commissioning an independent RICS survey, exchanging contracts (the legally binding point), and completing.

Buying & Moving

Buying & MovingFirst-Time Homebuyer's Guide to Moving and Property Inspections

First-time buyers in the UK should know that a lender's mortgage valuation is not a property survey and does not protect the buyer.

Buying & Moving

Buying & MovingFirst-Time Buyer Guide: Key Steps for Purchasing Your Home in the UK

Buying your first home in England or Wales involves securing a mortgage in principle, instructing a solicitor early, commissioning your own survey separately from the lender's valuation, and understanding that the purchase is not legally binding until exchange of contracts.

Buying & Moving

Buying & MovingFirst-time home buyer guide: essential property services and purchasing checklist

Buying your first home in the UK typically takes 12–16 weeks from offer acceptance to completion.

Buying & Moving

Buying & MovingThe Complete Property Buying Guide: From Search to Purchase

Buying a property in England and Wales typically takes 3–6 months from accepted offer to completion.