Government Property Support Schemes: Help to Buy Eligibility and Benefits

By Housey · Last reviewed 7th of May 2026

Government Property Support Schemes: Help to Buy Eligibility and Benefits

Many first-time buyers in the UK still search for Help to Buy without realising the flagship equity loan programme closed to new applicants in England in late 2022, with legal completions ending in March 2023. Understanding which government schemes are currently open, what eligibility rules apply, and how each one affects the conveyancing process is an essential first step before you commit to a purchase. The landscape of government-backed support has shifted significantly since 2019, and the schemes that remain carry specific conditions that affect your mortgage, your deposit, and the legal structure of your purchase.

Key points

- Help to Buy: Equity Loan in England closed to new applicants on 31 October 2022; all legal completions were required by 31 March 2023. No new applications are possible under this scheme.

- The Lifetime ISA (LISA) remains open: the government adds a 25% bonus on contributions of up to £4,000 per tax year (maximum £1,000 annual bonus), and the property must cost no more than £450,000.

- The First Homes scheme offers a minimum 30% discount on new-build purchase prices for eligible first-time buyers, key workers, and locally connected buyers in England; local authorities can increase the discount to 40% or 50%.

- Shared Ownership allows eligible buyers to purchase a share of between 10% and 75% of a property and pay rent on the remainder, with the option to buy additional shares over time through a process called staircasing.

- Scotland and Wales operate distinct devolved schemes — including Help to Buy Scotland and Help to Buy Wales — with different eligibility criteria, property price caps, and timelines from the English arrangements.

What was Help to Buy and is it still available?

Help to Buy: Equity Loan was a government programme under which buyers received an equity loan of up to 20% of the purchase price of a new-build home (40% in London), interest-free for the first five years. Buyers provided a minimum 5% deposit and took a mortgage for the remaining portion.

The scheme in England is now definitively closed. The deadline for new applications was 31 October 2022 and the final legal completion deadline was 31 March 2023. No new equity loans are being issued.

Help to Buy: ISA was a separate savings scheme, also closed to new applicants since 30 November 2019. Existing holders can continue saving until 30 November 2029 and must claim the government bonus — 25% on savings up to £12,000, maximum bonus £3,000 — before 1 December 2030. Your conveyancer handles the bonus claim at completion.

Help to Buy Scotland and Help to Buy Wales are separate devolved programmes with their own eligibility criteria and timelines. Check the Scottish Government's mygov.scot and the Welsh Government's website for current information.

Government schemes currently available to UK buyers

The table below summarises the main national schemes as of May 2026. Always verify the current status and eligibility criteria on GOV.UK or the relevant devolved government website before making any financial decisions, as scheme rules can change at short notice.

Scheme | Who it is for | How it works | Key limit (England) | Status |

|---|---|---|---|---|

Lifetime ISA | First-time buyers aged 18–39 | 25% government bonus on up to £4,000/year; use savings for deposit | £450,000 property cap | Open |

First Homes | First-time buyers, key workers, locally connected (England) | Minimum 30% discount on new-build; discount protected by title covenant | Varies by LPA | Open (England) |

Shared Ownership | First-time buyers; certain existing owners | Buy 10–75% share; pay rent on remainder; staircase to full ownership | Varies by scheme | Open |

Right to Buy | Secure council tenants (England) | Purchase council home at discount based on tenancy length | N/A | Open (England) |

Help to Buy ISA | Existing holders only (closed Nov 2019) | Bonus claimed at completion | £250,000 (£450,000 London) | Closed to new; save until Nov 2029 |

Help to Buy Equity Loan | Closed | Government equity loan on new-build | — | Closed (England, March 2023) |

Scheme status and eligibility rules are subject to change. Verify the current position on GOV.UK, the Scottish Government, or Welsh Government websites before relying on this information.

Lifetime ISA: eligibility and how it works

The Lifetime ISA is the principal government savings bonus available to first-time buyers in 2026.

- Eligibility: you must be aged 18–39 to open a LISA. Once open, you can contribute and earn the bonus until you turn 50.

- Contribution limit: up to £4,000 per tax year, earning a maximum government bonus of £1,000 per year.

- Property price cap: the property must cost no more than £450,000. If the purchase price exceeds this, the LISA cannot be used and a 25% withdrawal charge applies.

- How the bonus is applied: at completion, your conveyancer requests the LISA funds and bonus from your provider and applies them to the purchase price.

- Withdrawal penalty: if you withdraw LISA funds for any reason other than a qualifying first-home purchase, terminal illness, or reaching age 60, a 25% charge applies to the total amount withdrawn — including the bonus itself — meaning you may receive back less than your original contributions.

- Mortgage requirement: the purchase must use a repayment mortgage; cash purchases do not qualify.

The LISA is available from banks, building societies, and investment platforms. If your purchase is more than two or three years away, a stocks and shares LISA may offer better long-term returns, though it carries investment risk.

First Homes scheme

First Homes is an English government programme requiring developers to sell qualifying new-build homes at a minimum 30% discount to eligible buyers. The discount is registered as a covenant at HM Land Registry, meaning all future sales must also be made at the same or greater percentage discount to another qualifying buyer — it stays with the home permanently.

Eligibility criteria (England):

- First-time buyers only, as defined by HMRC.

- Combined household income must not exceed £80,000 per year (£90,000 in London).

- Local authorities may apply additional criteria such as a local connection to the area or key-worker status.

- The full market price before discount is typically capped at £250,000 (£420,000 in London), though local authorities can set lower caps.

Availability depends on the developer's planning obligations for a specific site. Ask the developer or check with your local planning authority about whether First Homes plots are included in any development you are considering.

Shared Ownership: how it works in practice

Shared Ownership allows you to buy a share in a property and pay rent on the portion you do not own. It is available primarily through housing associations in England, Scotland, and Wales, each with their own rules.

Worked example — a realistic UK scenario:

Consider a property with a full market value of £280,000 in the East Midlands. Under Shared Ownership, you might purchase a 40% share for £112,000 while paying subsidised rent on the remaining 60% (£168,000) to the housing association. A 10% deposit on your purchased share would be £11,200. Monthly outgoings would include your mortgage repayment on £100,800 plus the rent charge on the unsold share, plus service charges.

Over time, you can buy additional shares — typically in 10% increments — through staircasing. A RICS-registered valuer must assess the property at each staircasing transaction. Once you own 100%, the rent ceases.

Key questions to raise with your conveyancer or solicitor before exchange:

- What are the full monthly costs, including mortgage repayment, rent, service charges, and any estate charges?

- Are there restrictions on subletting, alterations, or improvements?

- What is the minimum staircasing increment and how is the property valued at each step?

- Is the lease long enough for mortgage lenders — typically 85 years or more remaining is preferred?

- What happens to the rent when you staircase upward?

Decision tree: which scheme suits your situation?

- First-time buyer aged 18–39 with a purchase more than 12 months away? Open a Lifetime ISA as soon as possible to start accumulating the annual bonus.

- Existing Help to Buy ISA holder? Continue saving until November 2029 and confirm the bonus claim process with your conveyancer before exchange.

- Buying a new-build in England with a household income under £80,000? Ask the developer whether First Homes plots are available on this site.

- Can only afford a small initial share of a property? Explore Shared Ownership via housing associations. GOV.UK's Share to Buy directory lists available properties.

- Secure council tenant? Check Right to Buy eligibility; the discount depends on tenancy length and property type.

- Buying in Scotland or Wales? Check the Scottish Government and Welsh Government websites for current devolved scheme availability.

- None of the above apply? Speak to a whole-of-market mortgage broker who can advise on lender-specific low-deposit products.

Important limitations

This article provides general information about UK government property schemes as of May 2026. Scheme rules, eligibility criteria, property price caps, and open or closed status are subject to government announcements and may change at short notice. Nothing in this article constitutes financial, legal, mortgage, or investment advice.

Before making any decision based on a government scheme:

- Verify the current status and eligibility criteria on GOV.UK, the Scottish Government, or Welsh Government websites.

- Speak to a regulated independent financial adviser (IFA) or whole-of-market mortgage broker.

- Engage a qualified conveyancer or solicitor to review all documentation, covenants, and lease terms before exchange.

- For Shared Ownership and First Homes purchases, the covenant structure and resale restrictions must be fully understood before committing.

What to ask a qualified professional

When speaking to a mortgage broker, financial adviser, or conveyancer about government property schemes, ask:

- Which schemes are currently open and taking new applications?

- Given this property's price and my income, am I eligible for the LISA bonus, and will the withdrawal charge apply in any scenario?

- If I am buying Shared Ownership, what are the full monthly costs including rent, service charges, and any estate charges?

- What covenant will the First Homes discount place on the title, and how does this affect future saleability and remortgaging?

- How long does the conveyancing process typically take for a Shared Ownership or Help to Buy ISA purchase compared with a conventional transaction?

- What happens to my eligibility if the purchase price changes between exchange and completion?

When to get professional help

Speak to a regulated mortgage broker and a conveyancer or solicitor before committing to any government-assisted purchase. In particular:

- If you are uncertain whether you meet the eligibility criteria for any scheme — get independent confirmation before proceeding.

- If you are considering Shared Ownership and need to understand all costs, lease terms, and staircasing rights.

- If you hold a Help to Buy ISA and need to confirm the bonus claim process before exchange.

- If the property is a First Homes property — the legal implications of the discount covenant require proper legal advice.

- If you are buying in Scotland or Wales where scheme rules differ materially from England.

How Housey can help

When you are ready to progress with your purchase, Housey can help you find qualified professionals. Compare quotes from regulated conveyancing solicitors to handle scheme documentation and legal work. Before exchange, protect yourself with a RICS home survey or RICS Level 2 survey to understand the property's condition. An EPC is also required for most property transactions in England, Wales, and Scotland.

Frequently asked questions

Is Help to Buy still available in England?

No. Help to Buy: Equity Loan in England closed to new applicants on 31 October 2022, with a final legal completion deadline of 31 March 2023. No new equity loans are being issued. The main government-backed options for first-time buyers in England in 2026 are the Lifetime ISA, First Homes, and Shared Ownership. Check GOV.UK for any new scheme announcements.

What is the Lifetime ISA property price limit?

As of May 2026, the LISA property price cap is £450,000. If the property costs more than this, the LISA cannot be used for the purchase and a 25% government withdrawal charge applies to any funds accessed for that purpose. Because the charge is levied on the total withdrawal including the bonus, you may receive back less than your original contributions in some circumstances.

Can I use Shared Ownership to buy an older property?

Shared Ownership is primarily associated with new-build properties, but a resales market exists where existing Shared Ownership owners sell their share. Availability varies by area and housing association. Your conveyancer should check the remaining lease length, staircasing provisions, and service charge history carefully before you exchange contracts.

What is the minimum share I can buy under Shared Ownership?

For new Shared Ownership properties in England delivered under the Affordable Homes Programme since 2021, the minimum initial share is 10%, reduced from the previous 25%. Older resale properties may still carry a 25% minimum as set out in their original lease. Confirm the minimum share with the housing association before applying.

Do government schemes affect stamp duty?

Yes. First-time buyer Stamp Duty Land Tax relief applies in England on properties up to £500,000 — verify the current threshold on GOV.UK as it has changed in recent years. For Shared Ownership, buyers can elect to pay SDLT on the full market value at the outset or only on the share purchased. A conveyancer should advise on the most appropriate treatment for your circumstances.

Are there equivalent schemes in Scotland and Wales?

Yes. Scotland has historically offered Help to Buy (Scotland) and the Low-cost Initiative for First Time Buyers (LIFT). Wales has operated Help to Buy — Wales for new-build properties. Both devolved programmes have different eligibility criteria, property price caps, and timelines from English arrangements. Check the Scottish Government's mygov.scot and Welsh Government's gov.wales for current availability.

Sources and further reading

- Help to Buy: Equity Loan (closed scheme) — GOV.UK

- Lifetime ISA — GOV.UK

- First Homes scheme: guidance — GOV.UK

- Shared Ownership scheme — GOV.UK

- Right to Buy: buying your council home — GOV.UK

- Help to Buy (Scotland) — Scottish Government

- Buying a shared ownership home — Citizens Advice

Useful next reads

Buying & Moving

Buying & MovingGovernment-backed property schemes: support programmes for first-time home buyers

UK first-time buyers can access several government-backed programmes including the Lifetime ISA (25% bonus on savings up to £4,000 per year), Shared Ownership (part-buy, part-rent), and the First Homes scheme (discounts of 30–50% on new builds).

Buying & Moving

Buying & MovingFirst-Time Buyer Properties: Finding Your First Home

First-time buyers in the UK can access support including the Lifetime ISA, which adds a 25% government bonus on savings of up to £4,000 per year.

Buying & Moving

Buying & MovingThe Complete Property Buying Guide: From Search to Purchase

Buying a property in England and Wales typically takes 3–6 months from accepted offer to completion.

Buying & Moving

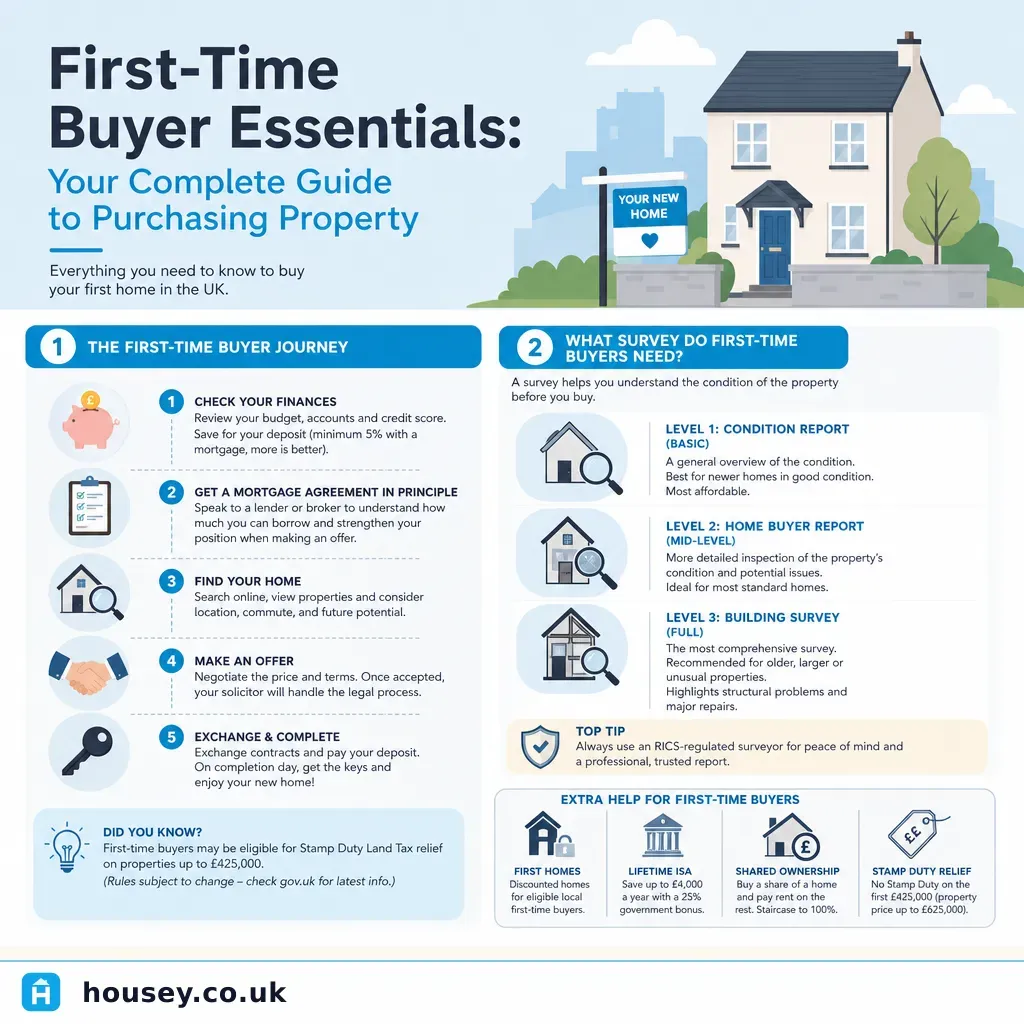

Buying & MovingFirst-Time Buyer Essentials: Your Complete Guide to Purchasing Property

Buying your first UK home involves six key stages: securing a mortgage Agreement in Principle, making an offer, instructing a solicitor, commissioning an independent RICS survey, exchanging contracts (the legally binding point), and completing.

Buying & Moving

Buying & MovingFirst-Time Homebuyer's Guide to Moving and Property Inspections

First-time buyers in the UK should know that a lender's mortgage valuation is not a property survey and does not protect the buyer.