Government-backed property schemes: support programmes for first-time home buyers

By Housey · Last reviewed 7th of May 2026

Government-backed property schemes: support programmes for first-time home buyers

Getting onto the property ladder has become significantly harder for many UK households, prompting successive governments to introduce programmes designed to reduce the deposit hurdle or lower the purchase price for eligible buyers. Several well-known schemes have closed in recent years, while others remain open — understanding the difference is essential before you factor any government support into your buying plans or financial calculations.

Key points

- The Lifetime ISA (LISA) pays a 25% government bonus on contributions of up to £4,000 per year — a maximum of £1,000 per year — and can be used to buy a first home priced at £450,000 or less.

- The First Homes scheme provides eligible first-time buyers with a minimum 30% discount on new-build homes; the discount is preserved in the title on resale, with some local authorities setting the discount at 40% or 50%.

- Shared Ownership allows buyers to purchase an initial share of between 10% and 75% of a property from a housing association, paying rent on the remainder, with the option to buy further shares over time (staircasing).

- The Help to Buy Equity Loan (England) closed to new applications on 31 March 2023; the Help to Buy ISA closed to new applicants on 30 November 2019, though existing account holders can claim the bonus until 1 December 2030.

- Right to Buy — which allows eligible council tenants to purchase their home at a discount — remains available in England but was abolished in Scotland (2016) and Wales (2019).

Current government-backed schemes at a glance

Always check GOV.UK or the relevant devolved authority for current eligibility, as rules, price caps, and availability can change with Budget announcements and policy updates.

Scheme | Status (May 2026) | Who it is for | Core benefit | Key restriction |

|---|---|---|---|---|

Lifetime ISA (LISA) | Open | First-time buyers aged 18–39 | 25% government bonus on up to £4,000/yr | Property must cost £450,000 or less; early withdrawal penalty applies |

Shared Ownership | Open | First-time buyers; income limits may apply | Part-buy, part-rent; deposit based on share purchased | Leasehold; service charges and rent add to monthly costs |

First Homes scheme | Open | First-time buyers meeting local or key worker criteria | 30–50% discount on new-build market price | Discount preserved on resale; local price caps apply |

Freedom to Buy | Check GOV.UK | First-time buyers and home movers | Access to 95% LTV mortgage products | Lender participation and rates vary |

Help to Buy Equity Loan | Closed (March 2023) | — | — | No new applications |

Help to Buy ISA | Closed (Nov 2019) | Existing account holders only | 25% bonus, maximum £3,000 total | Bonus must be claimed by 1 December 2030 |

Right to Buy | Open (England only) | Eligible council tenants in England | Discount on purchase of council home | Abolished in Scotland and Wales; eligibility rules apply |

Lifetime ISA: how it works in practice

The Lifetime ISA is open to UK residents aged 18–39. You can contribute up to £4,000 per year and the government adds a 25% bonus — up to £1,000 per year — directly into the account. To use it towards a home purchase, the property must be your first home, priced at £450,000 or less, and purchased with a mortgage. You must have held the LISA for at least 12 months before using it.

If you withdraw funds for any purpose other than a qualifying first-home purchase or retirement after age 60, a 25% government withdrawal charge applies. In some interest-rate environments this can leave you with less than you originally deposited, so a LISA is a long-term commitment rather than a flexible savings account. The £450,000 price cap means LISAs are most practical for buyers in lower-cost areas or those purchasing at the lower end of local markets.

Shared Ownership: part-buy, part-rent

Shared Ownership is available through housing associations on new-build and some resale properties. The minimum purchasable share was reduced from 25% to 10% for properties entering the scheme after 2021. Key features:

- Your deposit and mortgage are based on the share you purchase, not the full property value

- You pay a subsidised rent to the housing association on the remaining share

- You can buy additional shares over time (staircasing) up to full ownership

- Service charges, ground rent (where applicable), and leasehold conditions add to monthly costs

Selling a Shared Ownership property involves more steps than a standard sale. The housing association usually has a right of first refusal to find an eligible buyer before you can sell on the open market. Factor this into your long-term plans.

First Homes scheme: what the discount means

Eligible buyers receive a new-build property at a minimum 30% discount below open-market value. That discount is locked into the title — when you sell, the next buyer must also receive at least the same percentage discount, which restricts the resale price. Local authorities may set higher discounts (40% or 50%) and can apply local connection or key worker requirements. Availability depends on which developers in your area are participating.

What not to assume about government schemes

"Help to Buy is still available" — The Help to Buy Equity Loan closed in England in March 2023. References to it still appear in older articles and conversations. Check GOV.UK before building any scheme into your financial plans.

"Shared Ownership is similar to buying outright" — Shared Ownership properties are almost always leasehold. Monthly outgoings include a mortgage payment, a rent payment, and a service charge. Factor all three into your affordability assessment.

"The LISA bonus is unconditional" — The 25% bonus is only yours when used for a qualifying first-home purchase or after age 60. Withdrawing for other reasons triggers a charge that can erode your own savings. Read the terms before opening an account.

"Right to Buy works anywhere in the UK" — Right to Buy was abolished in Scotland in 2016 and in Wales in 2019. It remains available in England for eligible council tenants, but eligibility rules and discount levels have been subject to reform. Confirm the current position with your local authority.

"A government scheme removes the need for professional advice" — All property purchases require conveyancing and — if bought with a mortgage — a lender's valuation. A separate RICS survey is advisable regardless of scheme. Government support does not simplify the legal or physical due-diligence process.

Important limitations

This article contains general information about UK government-backed property schemes as of May 2026. Eligibility, price caps, discount levels, and availability can change with government policy and Budget announcements. This is not financial, legal, or mortgage advice. Before relying on any scheme, speak to a qualified independent mortgage adviser or financial adviser and instruct a solicitor experienced in scheme-specific transactions.

What to ask a qualified professional

Ask a mortgage adviser or independent financial adviser:

- Which lenders currently offer products compatible with this scheme, and what rates are available at my loan-to-value ratio?

- How does using a Lifetime ISA interact with the conveyancing process and overall timescale?

- Am I better placed using a LISA or saving a larger deposit to access a lower LTV mortgage product?

Ask your solicitor or conveyancer:

- What additional legal steps apply to a Shared Ownership or First Homes transaction, and how might these affect the timeline?

- What restrictions in the title — including those connected to the scheme — do I need to understand before exchanging contracts?

- Who is the housing association or local authority involved, and what rights do they retain over the property after purchase?

When to get professional help

Instruct a qualified mortgage adviser before committing to any government scheme — eligibility, lender availability, and the interaction between schemes and standard mortgage products can affect both cost and timeline significantly. Instruct a conveyancing solicitor early, as Shared Ownership and First Homes transactions often involve additional legal steps and take longer than standard open-market purchases.

If your survey reveals significant defects on a property you intend to buy through any scheme, seek an assessment from a RICS Home Survey professional before proceeding.

How Housey can help

Whether you are purchasing through a government scheme or on the open market, Housey connects you with qualified professionals for the services you need. Request quotes for a RICS Level 2 survey or a conveyancing solicitor and compare responses from vetted UK providers in one place.

Frequently asked questions

Can I use a Lifetime ISA with Shared Ownership?

In most cases, yes. A Lifetime ISA can be used for a Shared Ownership purchase provided the full open-market value of the property — not just the share being purchased — is £450,000 or less. Your solicitor and mortgage adviser should confirm this applies to your specific transaction, as the rules can interact in ways that affect conveyancing timescales and documentation.

What happens to the First Homes discount when I sell?

The discount is preserved in the title. When you sell a First Home, the buyer must receive at least the same percentage discount below market value that you received. This restricts the resale price and may affect how much equity you realise at sale. Factor this into your long-term financial planning before purchasing through the scheme.

Is Shared Ownership available across the UK?

Shared Ownership is widely available in England. Scotland, Wales, and Northern Ireland each operate equivalent or similar part-ownership schemes administered through devolved governments or housing associations, but the specific rules, eligibility criteria, and available discounts differ. Check the relevant devolved government website for the scheme applicable to your area.

Do I still need a survey if buying through a government scheme?

Yes. A mortgage lender's valuation is not a substitute for an independent RICS survey, regardless of the scheme used. For new-build properties purchased through First Homes or Shared Ownership, a snagging inspection or RICS assessment before legal completion is advisable to identify defects while the developer remains obligated to address them.

Will using a government scheme affect my conveyancing timeline?

Shared Ownership and First Homes transactions typically involve additional legal steps — including the housing association's or local authority's legal team reviewing documentation — which can add several weeks to a standard conveyancing timeline. Instruct your solicitor as early as possible and budget for a longer process than a straightforward open-market purchase.

Sources and further reading

- Lifetime ISA — GOV.UK

- Shared Ownership scheme — GOV.UK

- First Homes scheme guidance — GOV.UK

- Help to Buy equity loan — GOV.UK

- Right to Buy: buying your council home — GOV.UK

Useful next reads

Buying & Moving

Buying & MovingGovernment Property Support Schemes: Help to Buy Eligibility and Benefits

Help to Buy: Equity Loan in England closed in March 2023 and is no longer available to new buyers.

Buying & Moving

Buying & MovingFirst-Time Buyer Properties: Finding Your First Home

First-time buyers in the UK can access support including the Lifetime ISA, which adds a 25% government bonus on savings of up to £4,000 per year.

Buying & Moving

Buying & MovingThe Complete Property Buying Guide: From Search to Purchase

Buying a property in England and Wales typically takes 3–6 months from accepted offer to completion.

Buying & Moving

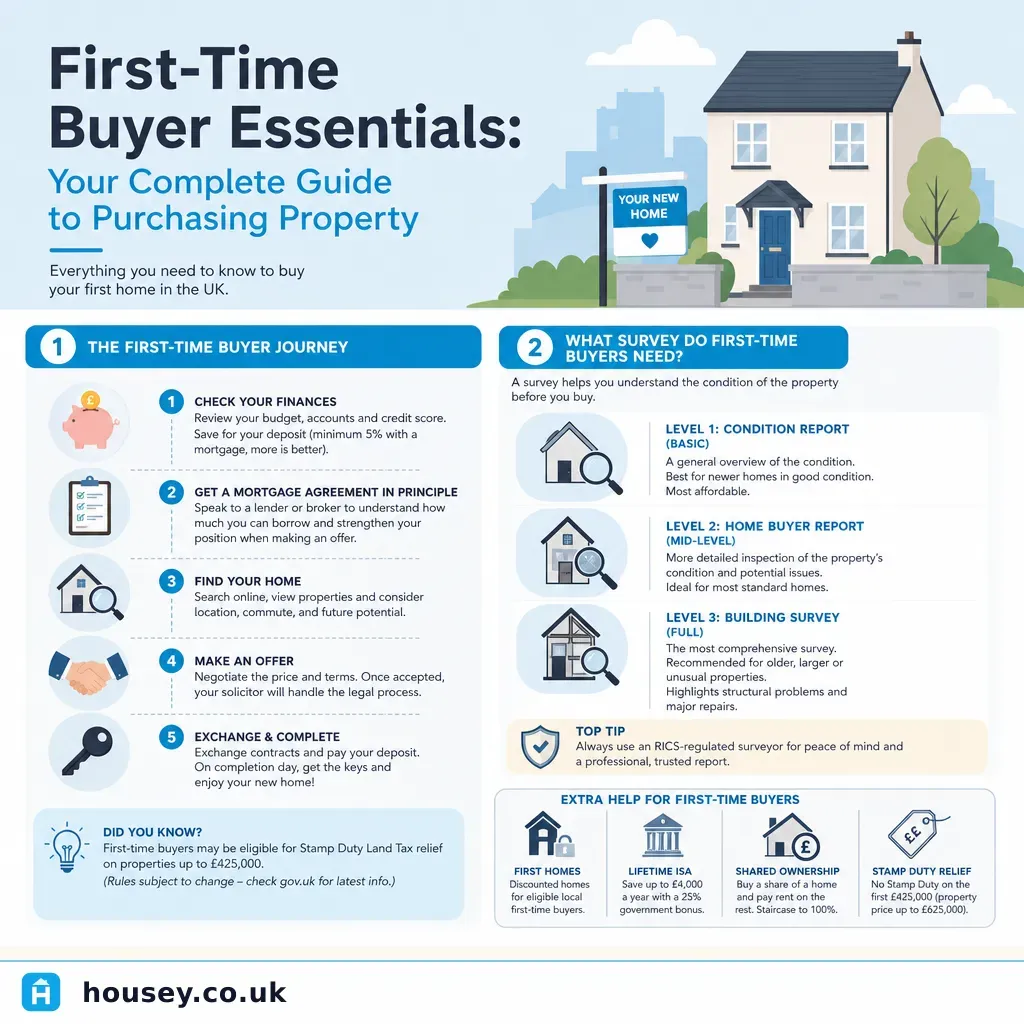

Buying & MovingFirst-Time Buyer Essentials: Your Complete Guide to Purchasing Property

Buying your first UK home involves six key stages: securing a mortgage Agreement in Principle, making an offer, instructing a solicitor, commissioning an independent RICS survey, exchanging contracts (the legally binding point), and completing.

Buying & Moving

Buying & MovingFirst-Time Homebuyer's Guide to Moving and Property Inspections

First-time buyers in the UK should know that a lender's mortgage valuation is not a property survey and does not protect the buyer.