First-Time Buyers in Action: The UK Homeownership Journey

By Housey · Last reviewed 10th of May 2026

First-Time Buyers in Action: The UK Homeownership Journey

The legal, financial, and practical steps involved in buying a first property in the UK follow a defined sequence — but the gap between knowing those steps exist and knowing what is expected of you at each one catches many buyers unprepared. Each stage has distinct documents, decisions, and professionals involved, and the consequences of delays or missteps range from a missed mortgage rate to losing a property after months of work. Whether you are a year away from buying or already attending viewings, understanding how the journey typically unfolds and where first-time buyers commonly encounter difficulties puts you in a significantly stronger position.

Key points

- The average time from offer accepted to legal completion in England and Wales is 12–16 weeks, though leasehold purchases, slow chains, or complex titles routinely extend this.

- Stamp Duty Land Tax (SDLT) relief for first-time buyers in England applies on purchases up to £500,000, with nil SDLT on the first £300,000 — check GOV.UK for current rates, as reliefs can and do change.

- A RICS Level 2 Home Survey is generally appropriate for conventional properties in reasonable condition; a RICS Level 3 Building Survey is recommended for older, altered, or visibly defective properties.

- A mortgage in principle (also called an Agreement in Principle) confirms a lender's conditional willingness to lend — it is not a mortgage offer, and the full application follows after an offer is accepted.

- Your conveyancer or solicitor handles the legal process, not your estate agent — choosing an experienced and responsive legal representative is one of the most consequential early decisions you will make.

How the purchase process typically works

The UK purchase process is sequential but not always linear. Understanding what is expected at each stage prevents costly delays.

Stage 1: Financial preparation. Before registering with estate agents, understand your borrowing capacity by speaking to a mortgage broker or direct lender. Gather payslips, your P60 (or self-assessment returns if self-employed), bank statements showing savings history, and identity documents. Obtain a mortgage in principle before making offers.

Stage 2: Viewing and making an offer. In England and Wales, neither party is legally committed until exchange of contracts — this is the "subject to contract" phase. Identify or instruct your conveyancer early, ideally before or at the same time as your offer, so searches can begin promptly. Scotland operates differently: formal offers are made through a solicitor and acceptance is typically legally binding.

Stage 3: Survey and mortgage valuation. Your mortgage lender will commission a mortgage valuation — this is for the lender's benefit and does not assess condition in useful detail for the buyer. Commission your own independent RICS survey. Defects identified before exchange give you negotiating leverage or the option to withdraw; defects found after completion are yours to fund.

Stage 4: Conveyancing. Your conveyancer handles local authority, drainage, and environmental searches, title register checks, and contract review. Exchange of contracts is the legally binding commitment — from this point you cannot pull out without forfeiting your deposit, typically 10% of the purchase price.

Stage 5: Completion. Mortgage funds transfer to the seller, keys are released, and you become the legal owner. SDLT must be filed and any tax paid within 14 days of completion.

Three illustrative UK first-time buyer scenarios

These are composite examples representing common UK first-time buyer situations. They are not accounts of specific individuals.

Scenario 1: 1990s semi-detached in the Midlands

A couple in their early 30s buy jointly — a 1995-built semi-detached in Leicestershire for £240,000 with a 10% deposit saved in a Lifetime ISA (LISA). They appoint a conveyancer before their offer is accepted, so searches begin immediately on acceptance. They commission a RICS Level 2 Home Survey, which flags minor pointing issues on the rear elevation. They use the report to negotiate a small reduction on the asking price. SDLT is nil on the first £300,000 for first-time buyers at the rates applicable to them. Total time from offer to completion: 14 weeks. Additional costs beyond the deposit: survey fee (approximately £450–600), conveyancing fees including disbursements (approximately £1,200–1,600).

Indicative UK costs, last reviewed 2026-05-10.

Scenario 2: Leasehold flat in Greater Manchester

A first-time buyer in their late 20s buys a 2008-built leasehold flat in Salford for £185,000. Remaining lease: 112 years — comfortably above the 80-year threshold below which future mortgage eligibility can be affected. The conveyancer requests three years of service charge accounts and the current buildings insurance certificate. The managing agent is slow to respond, delaying exchange by three weeks. A RICS Level 2 survey confirms no visible structural concerns or cladding issues in the communal areas. Total time from offer to completion: 18 weeks.

Scenario 3: Victorian terrace in South Yorkshire — cash purchase

A first-time buyer inherits enough to purchase a 1902-built two-bedroom terraced house outright for £135,000. With no mortgage valuation required, the buyer commissions a RICS Level 3 Building Survey — the right choice for a pre-1919 property where hidden defects in the structure, roof timbers, or damp-proofing are more likely. The report identifies evidence of rising damp in a rear ground-floor room. The buyer obtains two specialist remediation quotes and negotiates a £3,500 reduction before exchange. Completion occurs 8 weeks after offer acceptance.

Documents to prepare before and after your offer

Being ready with documents early reduces delays and signals reliability to your solicitor and lender.

Before making an offer:

After offer accepted:

What to ask before choosing your conveyancer

- Are you a solicitor or a licensed conveyancer, and which body regulates you?

- Will the same person handle my case from start to finish, or will it pass between staff?

- What is your experience with leasehold transactions?

- What is included in the quoted fee, and what disbursements am I likely to pay on top?

- What is your current typical timeframe from instruction to exchange?

- Are you on the approved panel for my mortgage lender?

- How will you communicate with me — online portal, email, or phone?

Important limitations

This article provides general information about the first-time buyer journey in England and Wales. The process differs in Scotland — where formal offers are made through a solicitor and acceptance is typically legally binding — and in Northern Ireland. Property law, SDLT rates, and available grant and ISA schemes change over time and vary by individual circumstance. Nothing in this article constitutes legal, financial, conveyancing, or surveying advice. A solicitor, licensed conveyancer, regulated mortgage broker, or RICS-registered surveyor should advise you on your specific situation before you make any legal commitments.

When this becomes urgent

Seek professional advice immediately — rather than relying on general information — if:

- A survey report flags structural movement, significant damp, or an urgent roof defect.

- You discover the lease has fewer than 85 years remaining after you have made an offer.

- Your conveyancer reports an unresolved title defect, missing building regulations approval, or an outstanding planning enforcement notice.

- Your mortgage offer differs materially from your agreement in principle — for example, a lower loan amount or a retention pending remedial works.

- The seller is unable or unwilling to provide documentation your conveyancer has requested within a reasonable timeframe.

What to ask a qualified professional

Ask your solicitor or conveyancer:

- Have you found anything unusual in the title register, planning history, or lease terms?

- What searches have you run, and have any returned concerns?

- When do you expect exchange to be ready, and what could delay it?

- Is there anything in the management pack (leasehold) I should be aware of before exchange?

Ask your RICS surveyor:

- Which defects are urgent and which are routine maintenance items?

- Should I commission specialist reports on anything flagged — for example, a structural assessment or damp specialist's inspection?

- Could any findings affect the mortgage offer or buildings insurance terms?

Ask your mortgage broker:

- Is a fixed-rate or tracker mortgage more appropriate for my circumstances?

- What early repayment charges apply, and when might they affect me?

- What protection products should I consider alongside the mortgage?

When to get professional help

Professional input is non-negotiable in these specific situations:

- If the survey flags structural movement, significant damp, or a roof in urgent need of repair — obtain specialist assessments before exchange.

- If the lease has fewer than 85 years remaining — seek advice from a leasehold specialist solicitor before committing.

- If planning history, extension works, or building regulations compliance is uncertain — your conveyancer should obtain relevant documentation or indemnity insurance before exchange.

- If the property is in a designated flood zone or has a confirmed history of subsidence — your insurer, lender, and surveyor all need to be informed before you proceed.

- If you are using a gifted deposit — your solicitor must handle source-of-funds verification correctly to satisfy anti-money-laundering requirements.

How Housey can help

Housey connects first-time buyers with vetted UK property professionals at every stage of the purchase journey. Request quotes for conveyancing, an independent RICS Level 2 survey or RICS Home Survey, and a valuation survey — and compare responses in one place before you instruct.

Frequently asked questions

How long does buying a first home typically take in the UK?

In England and Wales, the average time from offer accepted to completion is typically 12–16 weeks, though leasehold purchases, slow chains, or complex titles can extend this to six months or more. Scotland's process can move more quickly once a formal offer is accepted. Being organised with documents and appointing a responsive conveyancer from the start reduces delays significantly.

Do I need my own survey if I am getting a mortgage?

Your mortgage lender commissions a valuation for its own benefit — it does not assess condition in useful detail for the buyer. Commission your own independent RICS survey: Level 2 for a conventional modern property, Level 3 for an older or visibly defective one. The cost of a survey is far less than the cost of discovering a significant defect after completion.

What is the difference between exchange of contracts and completion?

Exchange is the legally binding moment — both parties commit, and you pay a deposit (usually 10% of the purchase price). If you withdraw after exchange, you forfeit that deposit. Completion is the day funds transfer to the seller and keys are released. The gap between exchange and completion is usually one to four weeks, agreed between both parties' conveyancers.

Can I buy a property without a solicitor or conveyancer?

There is no legal obligation in England and Wales, but in practice most mortgage lenders require a conveyancer on their approved panel. Self-conveyancing is complex, risky, and inadvisable for first-time buyers who are unfamiliar with title searches, contract conditions, and Land Registry requirements. The cost of a conveyancer is modest relative to the risks of errors.

What is a gifted deposit and how does it affect my purchase?

A gifted deposit is money given by a family member — usually a parent — with no expectation of repayment. Mortgage lenders and your solicitor require a signed gift letter confirming this, alongside the donor's bank statements showing the source of funds. This is a legal anti-money-laundering requirement, not an optional formality, and it must be handled correctly by your solicitor before exchange.

Sources and further reading

- Stamp Duty Land Tax: first-time buyers relief — GOV.UK: official SDLT first-time buyer relief rates and conditions

- Buying a home: step-by-step guidance — Citizens Advice: independent guidance on the purchase process in England and Wales

- RICS Home Survey Standards — RICS: official guidance on Level 2 and Level 3 survey scope and use

- Find a solicitor — The Law Society: regulated solicitor search for conveyancing

- First-time buyers: financial guidance — MoneyHelper (backed by HM Government): impartial financial guidance for first-time buyers

Useful next reads

Buying & Moving

Buying & MovingGovernment Property Support Schemes: Help to Buy Eligibility and Benefits

Help to Buy: Equity Loan in England closed in March 2023 and is no longer available to new buyers.

Buying & Moving

Buying & MovingSelecting and Working With Professional Moving Services

Choose a removal company that is a British Association of Removers (BAR) member, has its own employed staff and vehicles, and provides a written quote after a survey.

Buying & Moving

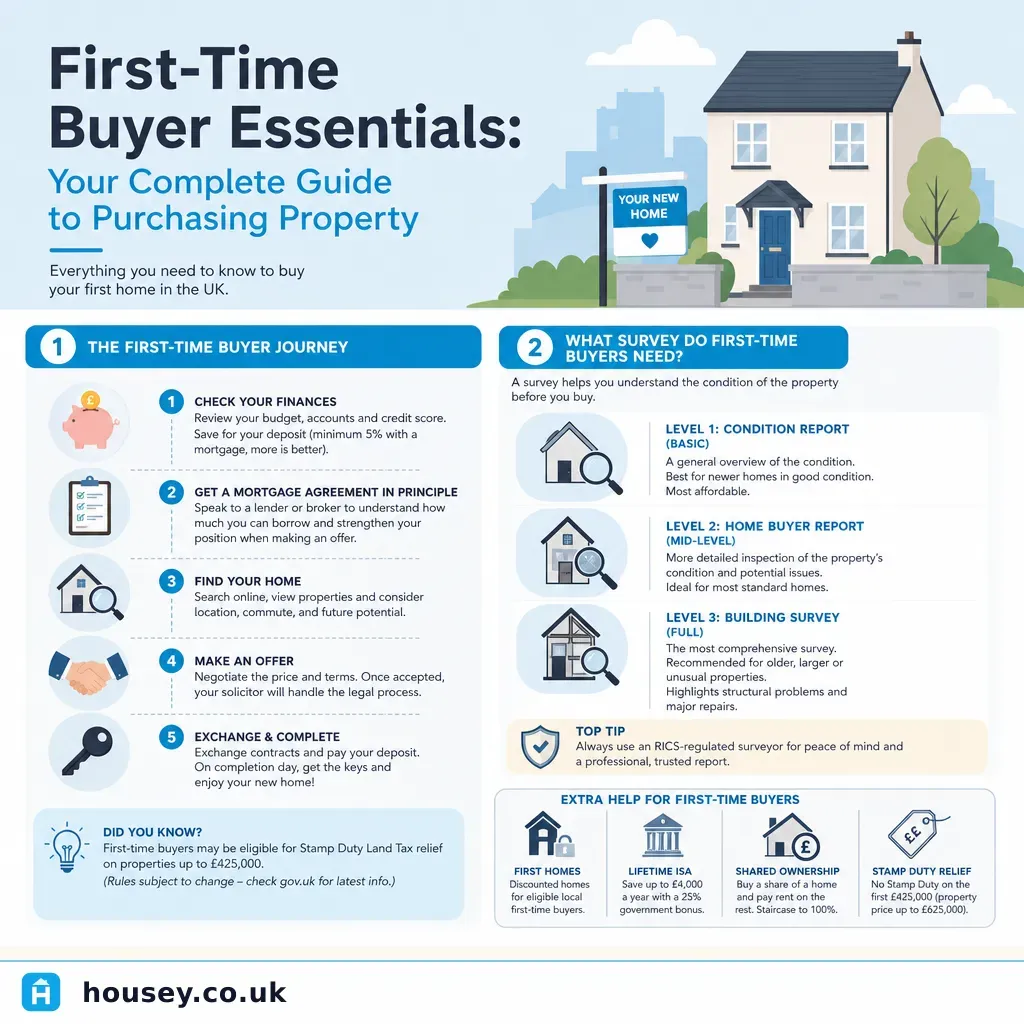

Buying & MovingFirst-Time Buyer Essentials: Your Complete Guide to Purchasing Property

Buying your first UK home involves six key stages: securing a mortgage Agreement in Principle, making an offer, instructing a solicitor, commissioning an independent RICS survey, exchanging contracts (the legally binding point), and completing.

Buying & Moving

Buying & MovingFirst-Time Homebuyer's Guide to Moving and Property Inspections

First-time buyers in the UK should know that a lender's mortgage valuation is not a property survey and does not protect the buyer.

Buying & Moving

Buying & MovingComplete Guide to Purchasing Property in the UK

Buying property in England and Wales typically takes 12 to 16 weeks from offer acceptance to completion.