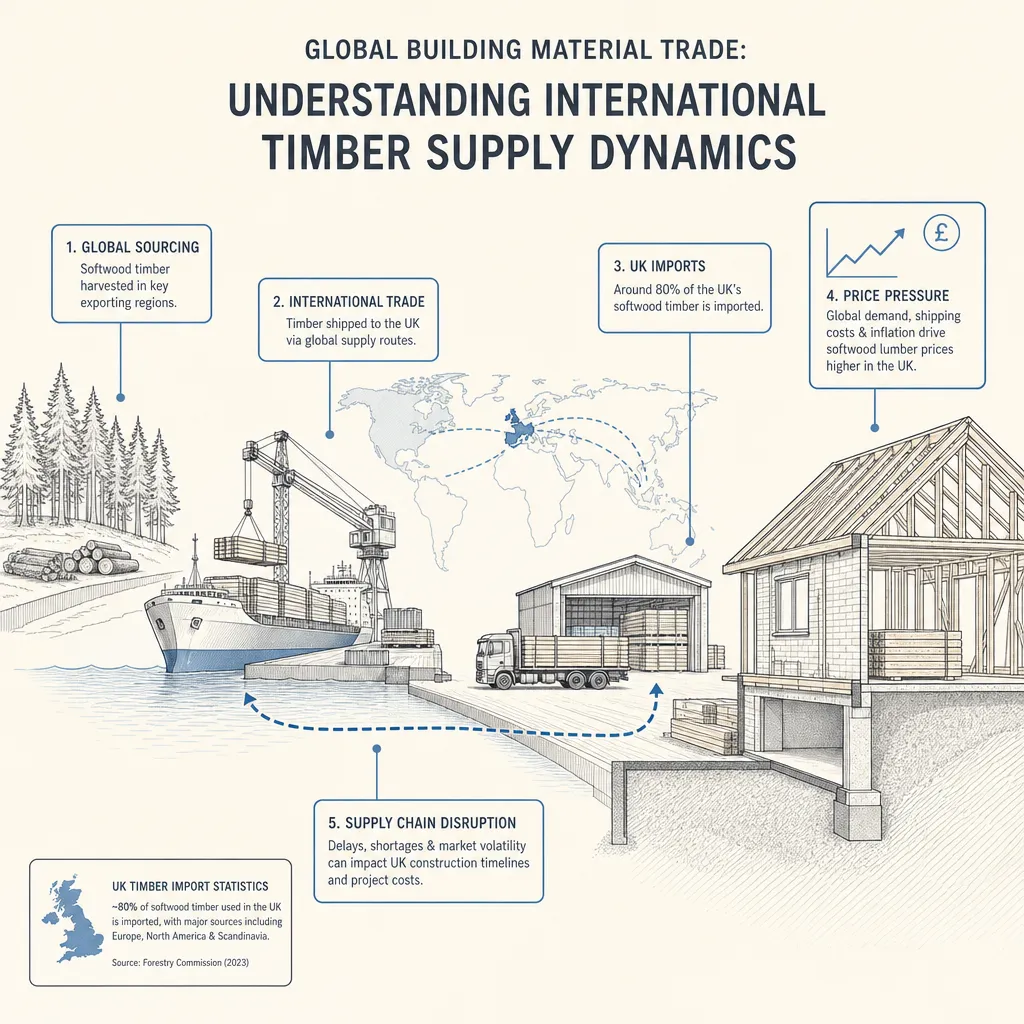

Global Building Material Trade: Understanding International Timber Supply Dynamics

By Housey · Last reviewed 31st of May 2026

Global Building Material Trade: Understanding International Timber Supply Dynamics

The UK's construction sector is deeply exposed to international commodity markets — a fact that becomes most visible when a housebuilder or self-builder receives revised quotes mid-project. Timber, the most widely used structural material in UK housing, is sourced predominantly from overseas, making domestic project budgets sensitive to events far outside any homeowner's control. Understanding the forces that shape global timber supply helps you plan more confidently and negotiate with greater precision.

Key points

- The UK imports approximately 80% of its structural timber, primarily from Scandinavia, the Baltic states, and Canada, according to the Timber Trade Federation.

- UK Government sanctions imposed in 2022 removed Russia and Belarus as viable timber supply sources for European markets, tightening Scandinavian availability and contributing to price pressure across the continent.

- Structural timber prices in the UK more than doubled between 2020 and mid-2021 before partially correcting; BCIS price indices show costs remain elevated relative to pre-pandemic baselines.

- Currency movements between GBP and EUR directly affect import costs — a 10% sterling depreciation roughly translates to a 10% increase in the sterling price of Swedish and Finnish timber.

- JCT construction contracts can include fluctuation provisions that pass material price increases through to the client after a base date; check whether your contract includes or excludes these clauses.

Where UK structural timber comes from

The UK has limited domestic softwood production — primarily Sitka spruce from Forestry Commission estates and commercial plantations in Scotland, Wales, and Northern England. Domestic supply accounts for roughly 20% of UK structural timber use; the remainder is imported.

Source region | Main species | Typical product | Dependency risk |

|---|---|---|---|

Scandinavia (Sweden, Finland) | Norway spruce, Scots pine | Sawn structural timber, C16/C24 graded | High — largest single import source |

Baltic states (Latvia, Estonia, Lithuania) | Scots pine, Norway spruce | Sawn timber, engineered wood products | High — price-sensitive, currency-exposed |

Canada (British Columbia) | Douglas fir, Hem-fir | Large-section structural timber, glulam | Moderate — affected by wildfires and pine beetle |

Central Europe (Austria, Germany) | Norway spruce | Engineered wood (CLT, LVL, glulam) | Growing — engineered product imports increasing |

UK domestic (Scotland, Wales) | Sitka spruce | Sawn structural, pallet wood | ~20% of supply — growing slowly |

What disrupts global timber supply

Geopolitical events

The sanctions on Russian and Belarusian timber exports introduced in 2022 removed a significant source of European softwood. While UK builders had not relied heavily on direct Russian imports, the knock-on pressure on Swedish and Finnish supply — as the rest of Europe scrambled to replace its eastern sources — contributed to price inflation across the continent.

Extreme weather and forest health

Canadian wildfires and the decades-long mountain pine beetle epidemic in British Columbia have reduced harvestable timber significantly. The ongoing US-Canada softwood lumber dispute, with recurring tariffs, further constrains North American supply from reaching international markets.

Post-pandemic demand surges

The 2020–2021 pandemic triggered simultaneous demand spikes in North America and Europe as DIY renovation boomed and housing starts accelerated. Sawmill capacity that had been cut during the 2008–2013 downturn could not be quickly restored, creating a classic supply-demand gap that pushed prices to record levels.

How supply dynamics affect UK self-builders and renovators

Contract and quote timing

Timber-intensive projects — timber-frame homes, large extensions with engineered floor joists, loft conversions using structural ridge beams — are most exposed to market movements. A quote given in January may use different market rates than the actual material purchase in March if supply is volatile. Ask contractors whether their quote is fixed-price or subject to material price fluctuation, and check whether a JCT fluctuation clause applies.

Which contract type should you choose?

- Choose a fixed-price contract if market prices are rising and you want budget certainty — but expect the contractor to price in a risk premium for the uncertainty they absorb.

- Choose a fluctuation contract if prices are stable or falling and you want to benefit from lower actual costs — accepting that you bear the downside risk of any rise.

- Ask a quantity surveyor or project manager for advice if the project value exceeds approximately £50,000 or the programme extends beyond six months from quote to completion.

- Check the BCIS materials cost index (published quarterly) for a current benchmark before signing any contract.

Substitution options

When softwood prices spike, builders sometimes use alternatives:

- I-joists or metal web joists instead of solid timber floor joists — often cost-competitive and more dimensionally stable in service

- Concrete block and beam instead of timber ground floors in some new-build contexts

- Steel universal beams for large spans where timber would previously have been used

These substitutions can affect insulation specifications and Building Regulations compliance under Part A (structure) and Part L (energy efficiency), so always check the implications with your structural engineer or building designer before agreeing to any change.

What not to assume

- Don't assume your quote price locks in the material cost. Many smaller builders quote on current prices and may apply for a variation order if materials rise substantially before purchase.

- Don't assume UK-sourced timber is unaffected by global markets. Scottish Forestry Commission pricing tracks European market benchmarks closely.

- Don't assume C16 and C24 graded timber is always equivalent. Both are strength-class grades under BS EN 338, but moisture content, treatment level, and dimensional accuracy vary between suppliers and should be specified in writing.

- Don't assume timber-frame suppliers hold large stocks. Most operate on short lead times; placing a materials order in advance of the main contract can sometimes secure current pricing.

When to get professional help

A quantity surveyor or cost consultant can benchmark material costs against current indices and advise on appropriate contract terms for volatile market conditions. If your project budget is sensitive to price swings of more than 5–10%, professional cost planning is worth the fee.

Consider seeking professional cost advice when:

- The project value exceeds £100,000

- The programme extends more than six months from quote to practical completion

- The project uses a timber-frame or heavily engineered-timber structural system

- Quotes from multiple contractors vary by more than 20% without a clear explanation

How Housey can help

Housey connects UK homeowners with local professionals for the planning and build stages of residential projects. Whether you are commissioning a structural design, managing a contractor tender, or reviewing contract terms for a self-build or extension, Housey can help you find qualified, accredited professionals in your area.

Frequently asked questions

Does the UK produce enough timber for domestic construction needs?

No. The UK imports approximately 80% of its structural timber, mainly from Scandinavia and the Baltic states. Domestic production — primarily Sitka spruce from Scottish and Welsh forests — supplies roughly 20% of structural timber demand, though the Forestry Commission and private landowners are gradually expanding planting to improve this share over the long term.

How do I protect my project budget from timber price rises?

The most direct protection is a fixed-price contract with your builder or timber-frame supplier that explicitly covers materials. For larger projects, a quantity surveyor can model sensitivity to price moves and recommend appropriate contract terms. Monitoring the BCIS materials cost index quarterly also provides early warning of directional market shifts.

Are engineered wood products like CLT and glulam affected by the same supply issues?

Yes. Engineered products are manufactured predominantly in Austria, Germany, and Scandinavia using the same softwood raw material, following structural timber price trends closely. They may carry longer lead times — particularly for bespoke glulam or CLT panels — which adds programme risk when markets are tight.

What is C16 and C24 graded timber?

These are European strength-class grades under BS EN 338. C16 is the lower strength class, used for lighter structural applications such as studwork; C24 is higher strength and required for more heavily loaded members. Your structural engineer or building designer will specify which grade is required for each element of the project.

Sources and further reading

- UK timber trade statistics and market data — Timber Trade Federation

- BCIS materials cost indices — BCIS (Building Cost Information Service)

- UK sanctions on Russia: timber and wood products — GOV.UK

- UK forestry statistics — timber production and supply — Forestry Research (Forestry Commission)

- BS EN 338: Structural timber — strength classes — BSI Group

Useful next reads

Planning & Pre-Build

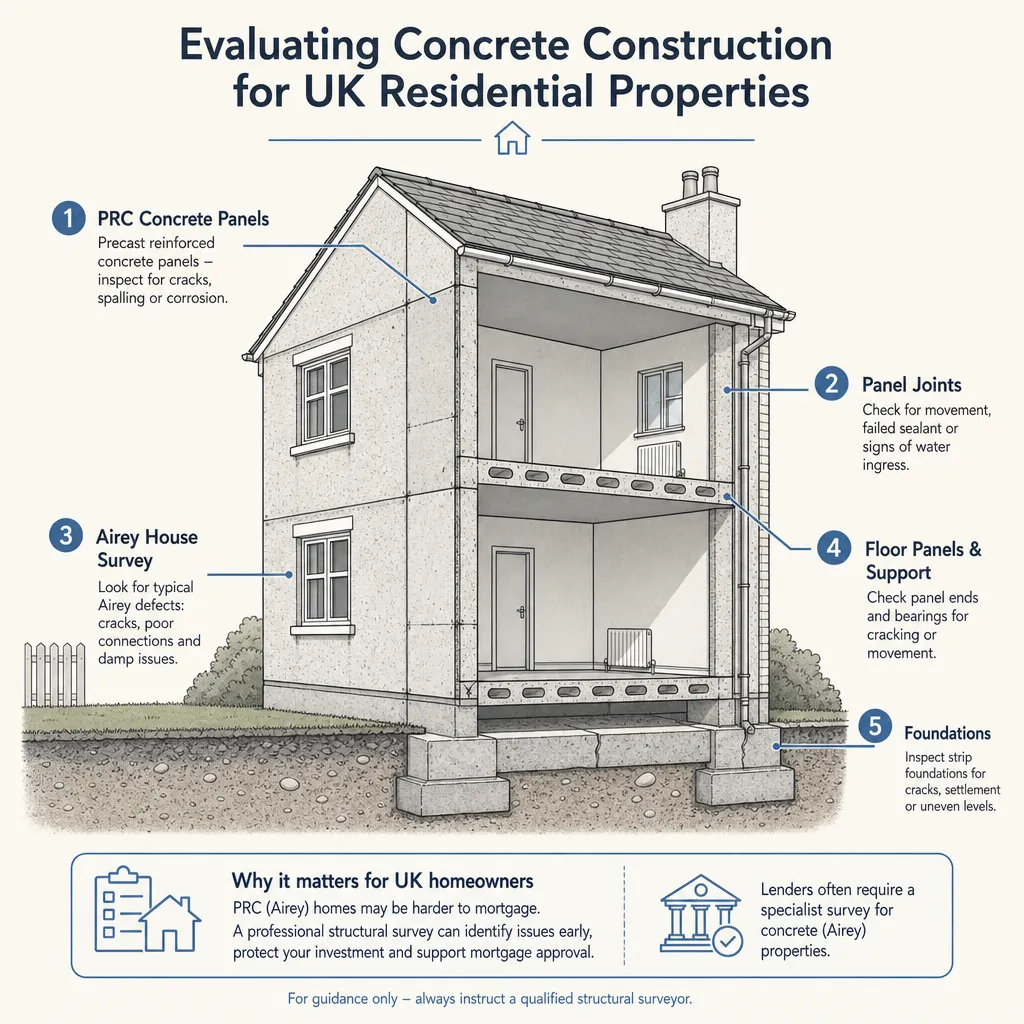

Planning & Pre-BuildEvaluating Concrete Construction for UK Residential Properties

Concrete construction in UK homes covers post-war non-traditional housing — such as Airey and Wimpey No-Fines properties — typically classified as non-standard by mortgage lenders, and modern systems including ICF and block cavity wall, which are generally standard.

Planning & Pre-Build

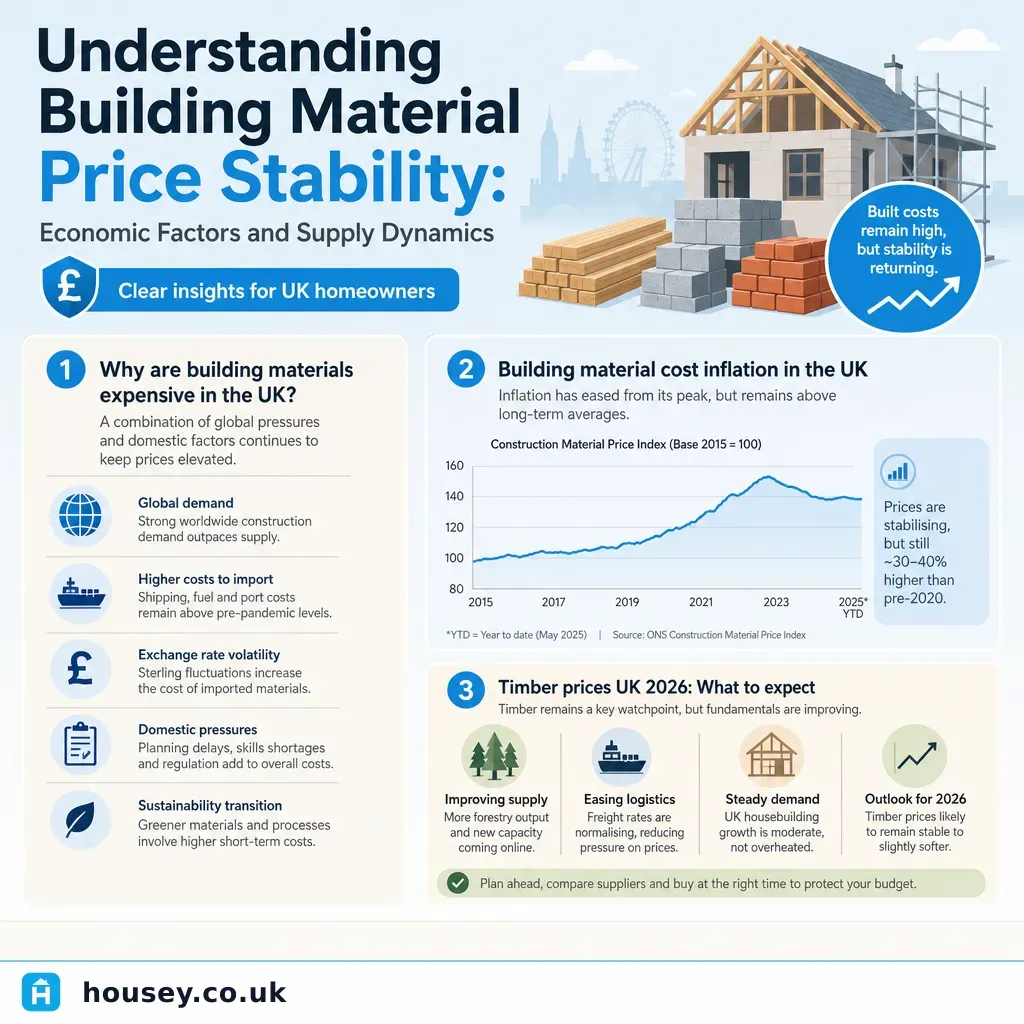

Planning & Pre-BuildUnderstanding Building Material Price Stability: Economic Factors and Supply Dynamics

Building material prices in the UK are shaped by global commodity markets, energy costs, exchange rates, and domestic construction demand.

Planning & Pre-Build

Planning & Pre-BuildSourcing Reclaimed and Salvaged Building Materials for Period Renovation

Reclaimed materials — including original bricks, flooring, roof tiles, lime mortar, and architectural salvage — are often the best match for period properties and may be required by conservation officers or planning conditions.

Planning & Pre-Build

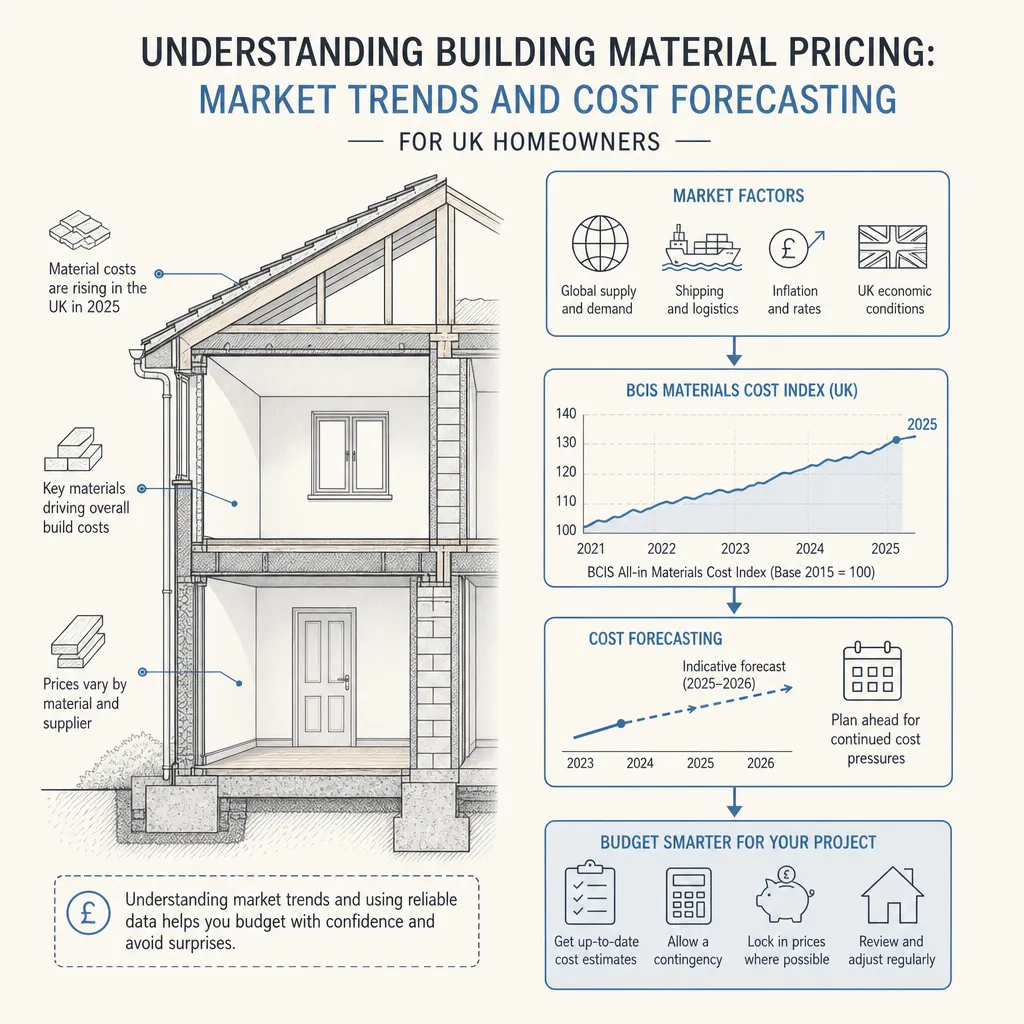

Planning & Pre-BuildUnderstanding Building Material Pricing: Market Trends and Cost Forecasting

Building material prices in the UK are driven by global commodity markets, energy costs, and supply-chain conditions, and can shift substantially within a single project's timeline.

Planning & Pre-Build

Planning & Pre-BuildChanges to Loft Conversion Rules: Permitted Development and Planning Updates

In England, most loft conversions on standard houses qualify as Permitted Development under Class B of the GPDO 2015, allowing up to 40 cubic metres (terraced) or 50 cubic metres (detached or semi-detached) without a planning application — if conditions are met.