Home Hunting Strategies and Property Evaluation Guidance

By Housey · Last reviewed 9th of May 2026

Home Hunting Strategies and Property Evaluation Guidance

Finding the right property in the UK is rarely straightforward — the difference between a sound purchase and a costly one often comes down to how systematically you approach your search and what you look for during viewings. Whether you are a first-time buyer or an experienced mover, a structured approach to property hunting and evaluation can save significant time, money, and stress before exchange of contracts.

Key points

- A mortgage in principle (MIP) from a lender is usually required before making an offer, and demonstrates to sellers that you are a finance-ready buyer.

- Leasehold properties require additional checks — including remaining lease length (under 80 years can affect mortgage eligibility), ground rent, service charges, and any pending Section 20 notices for major works.

- The Environment Agency flood map shows indicative flood risk zones; properties in Flood Zone 3 may face higher insurance premiums and restrictions on further development.

- A RICS Level 2 HomeBuyer Report or Level 3 Building Survey is entirely separate from the lender's mortgage valuation — the valuation assesses security for the lender, not condition for the buyer.

- Property chains — sequences of interdependent sales — significantly affect timeline reliability; chain-free properties typically complete faster and with lower collapse risk.

How to structure your property search

Start with constraints, not preferences. Most buyers find it more effective to define non-negotiables — commute time, school catchment area, minimum bedrooms, maximum total cost including stamp duty and legal fees — before browsing listings. This prevents scope creep and the viewing fatigue that comes from spending time on properties outside your practical criteria.

Useful tools for your search:

- Rightmove, Zoopla, and OnTheMarket list the majority of UK properties for sale. Setting up email alerts for your criteria ensures you see new listings promptly.

- Local estate agents often list properties before they appear on portals — registering directly can give early access.

- HM Land Registry Price Paid Data (available on GOV.UK) shows what comparable properties sold for recently in any postcode, providing a factual baseline for price assessment and negotiation.

- Ofcom's coverage checker confirms mobile signal and broadband availability at specific addresses — a practical consideration for remote working.

Once you have a shortlist, map properties geographically. Consider proximity to transport links, flood risk zones (Environment Agency flood map), noise sources (road, rail, flight paths), and the aspect of main rooms and the garden.

What to evaluate when viewing a property

The first viewing is usually emotional; the second should be analytical. If you are seriously interested, arrange a second visit at a different time of day to assess light levels, noise, and street activity.

During viewings, look specifically at:

- Walls and ceilings: Cracks, fresh plasterwork in localised areas (which can indicate attempts to conceal defects), damp patches, tide marks, and discolouration near window reveals or external walls.

- Windows and doors: Sticking or difficulty opening can indicate structural movement or settlement.

- Roof: Check from outside for missing or slipped tiles, a sagging ridgeline, moss growth, and the condition of flashings around chimneys and dormers.

- Loft space: If accessible, look for daylight gaps, insulation coverage, signs of damp, rodent activity, or previous water ingress.

- Boiler and heating: Ask about boiler age, service history, and whether there is a current Gas Safe certificate. Check radiator coverage and hot water pressure.

- Electrics: Ask when the last Electrical Installation Condition Report (EICR) was carried out and whether the consumer unit (fuse board) is modern.

- Extensions or conversions: Ask whether Building Regulations completion certificates and any necessary planning permissions were obtained — missing documentation can cause problems at conveyancing.

Property evaluation decision tree

Use this to determine the right level of investigation before making an offer:

- New build property? → Request the NHBC Buildmark warranty or equivalent. Consider an independent new-build snagging survey before legal completion.

- Pre-1919 solid-wall construction? → Commission a RICS Level 3 Building Survey. Damp penetration, thermal performance, and structural condition are more complex to assess in older stock.

- Extended or significantly altered? → Request planning permissions, Building Regulations completion certificates, and any party wall agreements from the seller's solicitor.

- Leasehold (flat or new-build house)? → Ask your solicitor to review remaining lease length, annual ground rent and service charges, and any pending major works or Section 20 notices.

- In a flood risk zone? → Check the Environment Agency flood map. Request flood history disclosures through your solicitor and obtain flood insurance quotes before proceeding.

- Visible cracks or signs of movement? → Do not rely solely on a RICS Level 2 survey. Consider a RICS Level 3 Building Survey or a specialist structural engineer's report.

- Non-standard construction? → Prefabricated, steel-frame, or large-panel system properties can be difficult to mortgage and insure — check with your lender before progressing.

How to compare properties objectively

When you have seen several properties, comparing them fairly from memory alone is difficult. A simple scoring system surfaces trade-offs that get lost in the emotional experience of viewings.

Property comparison template:

Criterion | Property A | Property B | Property C |

|---|---|---|---|

Price vs. budget |

|

|

|

Commute time (mins) |

|

|

|

School catchment fit |

|

|

|

Overall condition (1–5) |

|

|

|

Garden / outdoor space |

|

|

|

Parking provision |

|

|

|

Leasehold / freehold |

|

|

|

Extension potential |

|

|

|

Flood risk zone |

|

|

|

Estimated survey risk |

|

|

|

Score each criterion 1–5 and total. This will not make the decision for you, but it creates a structured basis for comparison and surfaces practical trade-offs before you commit to commissioning surveys.

Red flags to watch for during a property search

The following do not automatically mean you should walk away, but each warrants further investigation before exchange:

- Fresh paint or new plaster in localised areas — especially in basements, ground-floor walls, or bathrooms — can indicate attempts to conceal active damp or recent mould remediation.

- Low asking price relative to comparables — check recent sold prices on HM Land Registry; significant underpricing sometimes reflects a condition problem the seller is aware of.

- Title complications: Flying freeholds, chancel repair liability, restrictive covenants, and missing planning consents are not visible during viewings but will emerge in your solicitor's searches.

- Unmortgageable features: Non-standard construction, a short lease, and certain cladding types can make a property difficult to insure or finance — verify with your lender early.

- A very pressured timeline: Rushing to exchange rarely serves buyers. Ensure your solicitor has adequate time to complete all searches and raise enquiries properly.

- Reluctance to allow a survey: Uncommon, but worth noting if a seller attempts to discourage an independent inspection.

What to ask the estate agent before making an offer

- How long has the property been on the market, and has the asking price been reduced?

- How many offers have been received, and at what level relative to the asking price?

- Is the seller chain-free, and what is their onward situation?

- Why is the seller moving?

- Have any surveys been carried out by previous interested buyers, and are the results available?

- What fixtures, fittings, and appliances are included in the sale?

When to get professional help

A RICS-qualified surveyor should inspect any property you are seriously considering before exchange of contracts. The mortgage valuation is not a substitute — it protects the lender's security interest, not your understanding of the property's condition.

Consider additional specialist input in these situations:

- Visible structural cracks, suspected movement, or subsidence history → structural engineer or RICS Level 3 Building Survey

- Pre-2000 construction with potential asbestos-containing materials → asbestos survey by an accredited analyst

- Suspected damp or timber decay → specialist damp and timber survey

- Drainage concerns, previous flooding, or drains close to a proposed extension → CCTV drain survey

- Listed building or Conservation Area property → heritage consultant or specialist planning advice before committing

How Housey can help

Housey helps UK homeowners connect with qualified professionals across the home-buying process — from RICS surveyors and structural engineers to drainage and asbestos specialists. Use Housey's service request tool to describe your property type and location and receive quotes from relevant local professionals.

Frequently asked questions

Do I need a survey if the property looks in good condition?

A property can appear well-presented while concealing significant defects — poor damp-proofing, inadequate insulation, faulty electrics, or hidden structural movement. The mortgage valuation does not assess condition for the buyer. Most buyers commissioning a RICS Level 2 or Level 3 survey do so precisely because visible condition is an unreliable guide to actual defect risk.

What is the difference between freehold and leasehold?

Freehold means you own the property and the land outright. Leasehold means you own the property for a fixed term under a lease. Leasehold properties — most commonly flats and some new-build houses — carry additional obligations including ground rent, service charges, and potentially major works contributions. Check remaining lease length carefully; below 80 years can affect mortgage eligibility and is costly to extend.

What does 'subject to contract' mean after an offer is accepted?

In England and Wales, an accepted offer is not legally binding until exchange of contracts. Either party can withdraw without penalty before that point. This differs from Scotland, where the offer and acceptance process (missives) creates a binding contract at an earlier stage. Confirm with your solicitor what stage you are at before treating the purchase as secure.

How many properties should I view before making an offer?

There is no fixed rule, but buyers who view fewer than four or five comparable properties often lack the reference points needed to judge whether a price is fair or a condition is typical for the area. Viewing a range — including some slightly outside your exact criteria — helps calibrate expectations and strengthens your negotiating position.

Sources and further reading

- HM Land Registry Price Paid Data — GOV.UK

- Environment Agency Flood Map for Planning — Environment Agency

- Ofcom Connected Nations Coverage Checker — Ofcom

- RICS Home Survey Standard — RICS

- Leasehold Advisory Service — LEASE

Useful next reads

Buying & Moving

Buying & MovingPre-Purchase Property Assessment: Strategies and Buyer Advisory

A pre-purchase property assessment in the UK typically combines an independent RICS Home Survey, conveyancing searches, and specialist inspections for damp or electrical condition where needed.

Buying & Moving

Buying & MovingComplete Guide to Purchasing Property in the UK

Buying property in England and Wales typically takes 12 to 16 weeks from offer acceptance to completion.

Buying & Moving

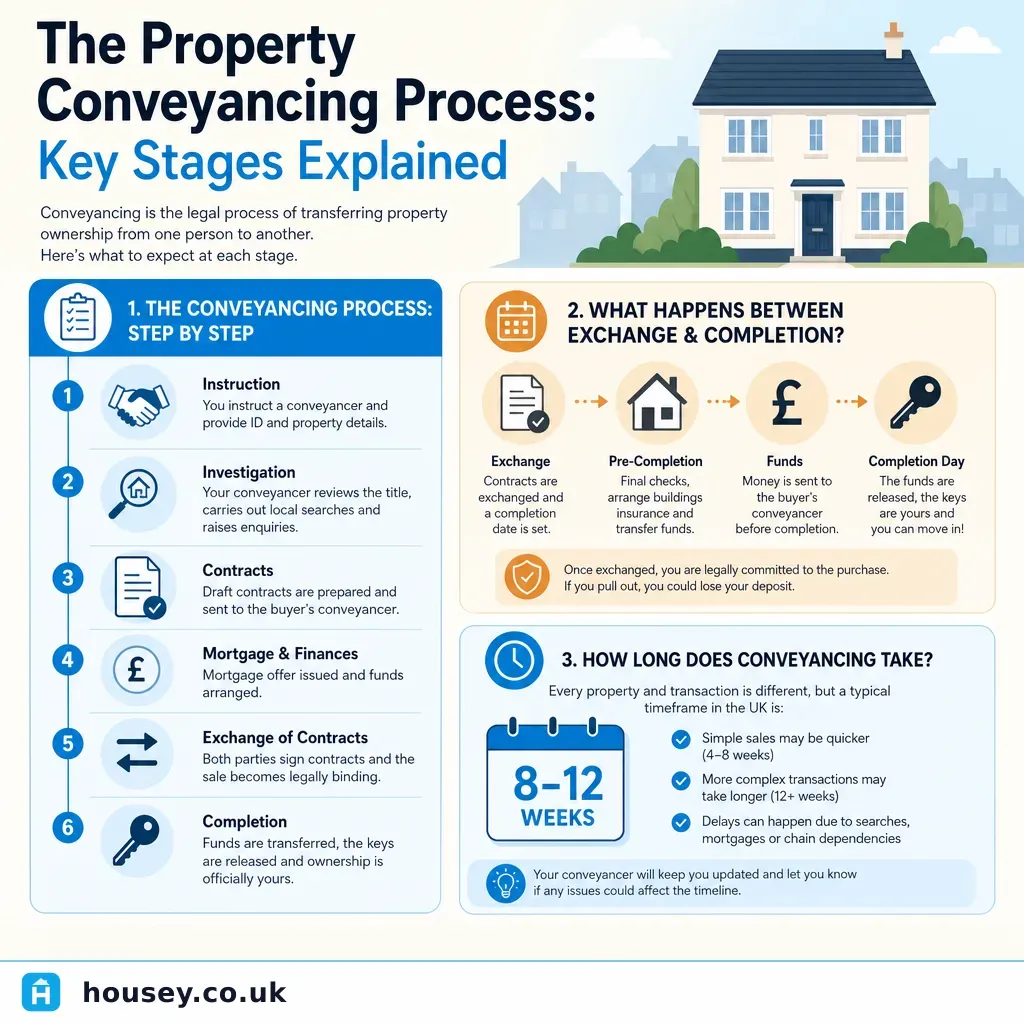

Buying & MovingThe Property Conveyancing Process: Key Stages Explained

The conveyancing process in England and Wales runs from instruction through to registration at HM Land Registry, typically in five stages: instruction, pre-contract searches and enquiries, exchange of contracts, completion, and post-completion.

Buying & Moving

Buying & MovingHow to find a property that matches your needs and budget

Finding the right property starts with separating non-negotiable needs from preferences, then building a realistic budget that includes SDLT, survey fees, and legal costs — typically 2–4% of the purchase price on top.

Buying & Moving

Buying & MovingWhat buyers need to know about single-storey homes

Bungalows offer accessibility, extension potential, and single-level living, but their full-footprint roof, ground-level damp risks, and often-lower EPC ratings require specific attention during the buying process.