How to find a property that matches your needs and budget

By Housey · Last reviewed 30th of May 2026

How to find a property that matches your needs and budget

Searching for a home in the UK is rarely a single moment of inspiration — it is an iterative process of narrowing preferences, testing assumptions against the market, and managing the gap between what you want and what you can actually afford. Most buyers begin with an idealised picture of their perfect property and discover that budget, location, tenure, and condition involve real trade-offs. Working through those trade-offs before you start viewing prevents wasted time, emotional decisions at viewings, and unwelcome discoveries after you have already committed.

Key points

- An Agreement in Principle (AIP) from a lender, showing the amount they are prepared to lend, should be obtained before making formal offers; most estate agents in England will ask to see one before accepting an offer.

- Leasehold properties — most flats and some new-build houses — carry ongoing financial obligations including service charges, ground rent (on older leases), and sinking fund contributions; a lease below 80 years significantly affects mortgage eligibility and resale value.

- The Energy Performance Certificate (EPC) rating (A–G) is a legal requirement at point of marketing in England and Wales; proposed Minimum Energy Efficiency Standards would require rental properties to meet EPC band C from 2028 — relevant if you are buying to let.

- Stamp Duty Land Tax (SDLT) in England is calculated in bands above the nil-rate threshold; check the current rates at GOV.UK as thresholds can change, and factor SDLT, solicitor's fees, survey costs, and removal costs into your total budget.

- The Environment Agency's free Check your long term flood risk tool should be consulted for any property you are seriously considering before instructing a solicitor.

Clarifying your needs before you search

Separating genuine needs from preferences before you register with agents or set portal alert filters is one of the most useful things a buyer can do. A need is a requirement whose absence makes the property unsuitable — the number of bedrooms, a ground-floor room for accessibility, or a particular school catchment. A preference is something you want but could live without — an en-suite bathroom, a south-facing garden, or a utility room.

Homeowner search checklist

Must-haves (non-negotiable):

Strong preferences (worth negotiating on price if absent):

Nice-to-haves (would not affect your decision):

Completing this exercise before viewing prevents decisions driven by a striking kitchen and helps you articulate your rationale clearly to estate agents.

Setting a realistic budget

Your budget is not just the maximum mortgage plus deposit. Total buying costs in England typically include:

- Stamp Duty Land Tax (SDLT): Calculated in bands; check GOV.UK for current rates. First-time buyers and purchasers of additional properties have different rate structures.

- Solicitor or licensed conveyancer fees: Typically £1,000–£2,500 plus disbursements (search fees, Land Registry fee, bank transfer charges). (Indicative UK costs, last reviewed 2026-05-30.)

- Survey fee: RICS Level 2 typically £400–£700; RICS Level 3 typically £600–£1,500 depending on property size and complexity. (Indicative UK costs, last reviewed 2026-05-30.)

- Mortgage arrangement and valuation fee: Varies by lender and product; some are added to the loan.

- Removal costs: £500–£3,000 or more depending on volume and distance. (Indicative UK costs, last reviewed 2026-05-30.)

- Immediate repair or improvement reserves: If the property needs urgent work, this comes from savings rather than the mortgage.

As a planning guide, budget for 3–4% of the purchase price in transaction costs above the price itself, before any renovation.

Decision tree: which type of property suits your situation?

- Choose a freehold house if you want full ownership of the building and land, are comfortable with sole maintenance responsibility, and do not want service charges or a management company.

- Consider a leasehold flat if budget or location requires it — but check the lease length (aim for above 85 years remaining), review at least two years of service charge accounts, and ask your solicitor about any major works planned or held in the reserve fund.

- Consider a new-build if low maintenance and a developer's structural warranty (NHBC Buildmark or equivalent) are priorities and you are comfortable with an estate-management environment; note that new-builds often carry a premium and estate charges even when freehold.

- Consider an older property (pre-1919) if character, room size, and location matter most — but expect higher survey and ongoing maintenance costs. Commission at minimum a RICS Level 2, and a Level 3 for Victorian or Edwardian stock.

- Ask a solicitor before proceeding with shared ownership, Help to Buy equity loan, or part-buy-part-rent structures; the legal obligations and exit conditions differ materially from a standard purchase.

- Ask a valuation surveyor if you are unsure whether the asking price reflects current market value; a RICS Registered Valuer can provide an independent assessment.

What not to assume when matching a property to your needs

Don't assume the EPC reflects your actual energy bills. An EPC D property with uninsulated solid walls will cost significantly more to heat than an EPC C modern flat, even if both are the same size. Ask about the wall type, heating system, and any insulation already fitted; the Energy Saving Trust provides guidance on expected running cost improvements from common retrofit measures.

Don't assume all flats are standard leasehold. Some flats are sold with a share of the freehold, and commonhold is a third tenure option. Ask your solicitor to explain the precise tenure and any management company structure before exchange.

Don't assume a well-presented property needs no survey. A 1970s concrete system-built or timber-framed house may look perfectly fine but is a non-standard construction that can be harder to mortgage, insure, and resell. A RICS survey identifies the construction type; ask the surveyor specifically if you have any suspicion.

Don't assume the agent's description of transport links matches your actual commute. Walk or drive the route at the time of day you would realistically travel; check train timetables for your specific route rather than relying on best-case journey planner estimates.

Don't assume mobile signal and broadband are acceptable without checking. Use Ofcom's checker tool to verify coverage and available broadband speeds at the specific address before viewing, particularly in rural or semi-rural locations.

When to get professional help

The survey and conveyancing fees are modest compared to the cost of discovering a serious problem after exchange. Commission at minimum a RICS Level 2 Home Survey on any property you make an offer on, and use a qualified solicitor or licensed conveyancer for all legal work.

Specific situations requiring professional input:

- If the survey flags potential structural movement, commission a separate structural engineer's report before exchanging contracts.

- If the EPC is F or G and you intend to let the property, take legal advice on Minimum Energy Efficiency Standards compliance obligations before committing.

- If the lease is below 80 years, ask your solicitor about the cost and process of a lease extension before making an offer.

- If you want an independent view on whether the asking price is fair, a valuation survey from a RICS Registered Valuer gives you an objective baseline for negotiation.

How Housey can help

Housey connects buyers and homeowners with local professionals at key stages of the property journey. When you want an independent view of a property's value or condition, our valuation survey specialists provide RICS-accredited assessments. If you are selling and want your home to perform well on portals, professional property photography and floorplans consistently attract more serious buyers and support a stronger asking price.

Frequently asked questions

Do I need an Agreement in Principle before viewing properties?

You do not need one to arrange a viewing, but most estate agents will ask for one before accepting an offer as evidence that you can fund the purchase. Obtaining an AIP before you start viewing seriously makes the process smoother and signals to agents and vendors that you are a credible buyer. Obtaining one typically involves a soft or hard credit search, depending on the lender.

How many properties should I view before making an offer?

There is no fixed rule, but viewing at least five to eight comparable properties in your target area before making an offer gives you a realistic sense of market value and condition at different price points. Making an offer on the first property you view can work out but increases the risk of overpaying or missing problems you would have learned to spot with more experience.

Can I negotiate the asking price in the UK?

Yes, and many UK buyers do. How much room there is depends on how long the property has been on the market, the level of local demand, and what the survey reveals. Survey findings are the most common and most accepted basis for a post-offer price reduction. Your solicitor or estate agent can advise on what reduction is realistic in the current local market.

What is the difference between a mortgage valuation and a survey?

A mortgage valuation is carried out for the lender's benefit — it confirms the property is adequate security for the loan and does not give the buyer a detailed picture of condition. A RICS Level 2 or Level 3 survey is carried out for you as the buyer, assessing condition, identifying defects, and recommending further investigations. Always commission an independent survey in addition to any lender valuation.

Sources and further reading

- Stamp Duty Land Tax: residential property rates — GOV.UK

- Check your long term flood risk — Environment Agency / GOV.UK

- RICS Home Survey Standard — RICS

- Energy Performance Certificates — GOV.UK

- Ofcom checker: broadband and mobile coverage — Ofcom

- Citizens Advice: buying a home — Citizens Advice

Useful next reads

Buying & Moving

Buying & MovingPre-Purchase Property Assessment: Strategies and Buyer Advisory

A pre-purchase property assessment in the UK typically combines an independent RICS Home Survey, conveyancing searches, and specialist inspections for damp or electrical condition where needed.

Buying & Moving

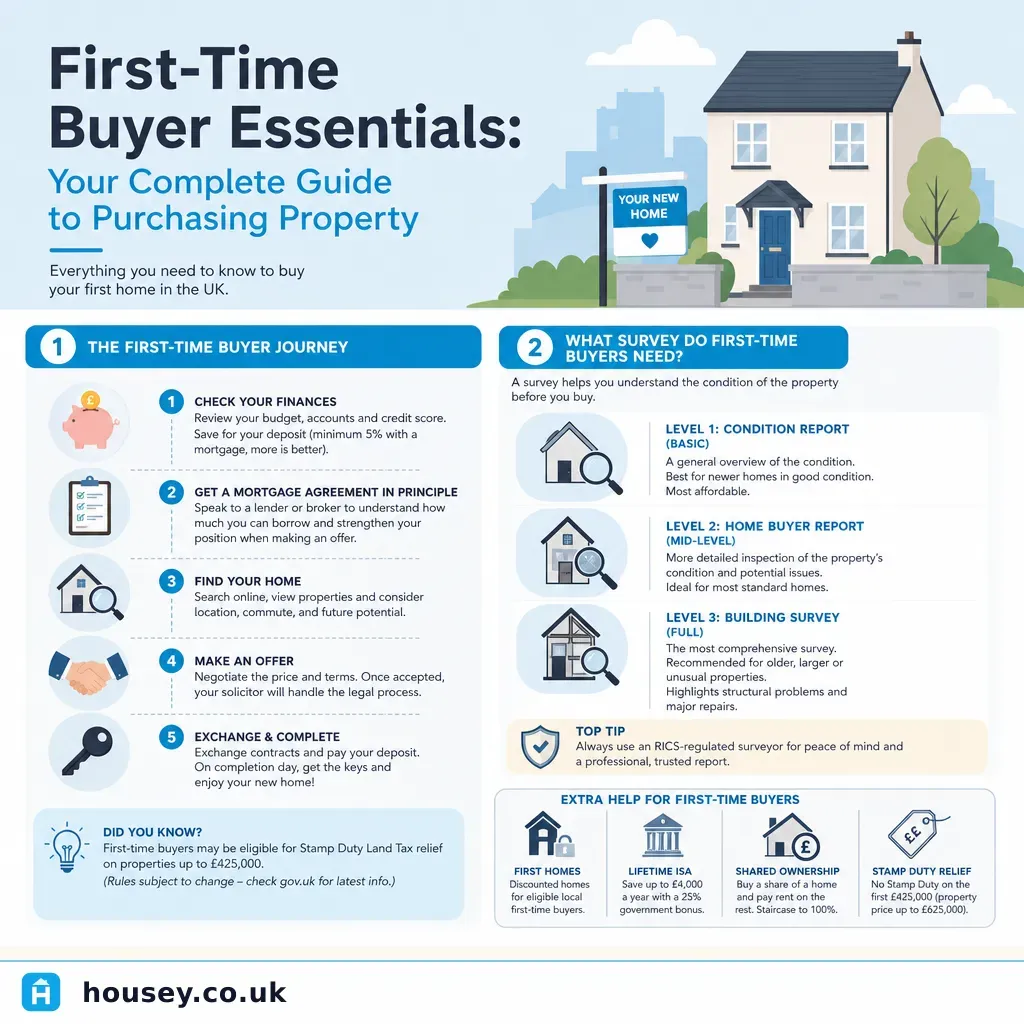

Buying & MovingFirst-Time Buyer Essentials: Your Complete Guide to Purchasing Property

Buying your first UK home involves six key stages: securing a mortgage Agreement in Principle, making an offer, instructing a solicitor, commissioning an independent RICS survey, exchanging contracts (the legally binding point), and completing.

Buying & Moving

Buying & MovingHome Hunting Strategies and Property Evaluation Guidance

To find and evaluate the right home, define your non-negotiable criteria before browsing, use HM Land Registry sold prices to check comparables, and inspect properties systematically for structural, damp, and electrical issues.

Buying & Moving

Buying & MovingComplete Guide to Purchasing Property in the UK

Buying property in England and Wales typically takes 12 to 16 weeks from offer acceptance to completion.

Buying & Moving

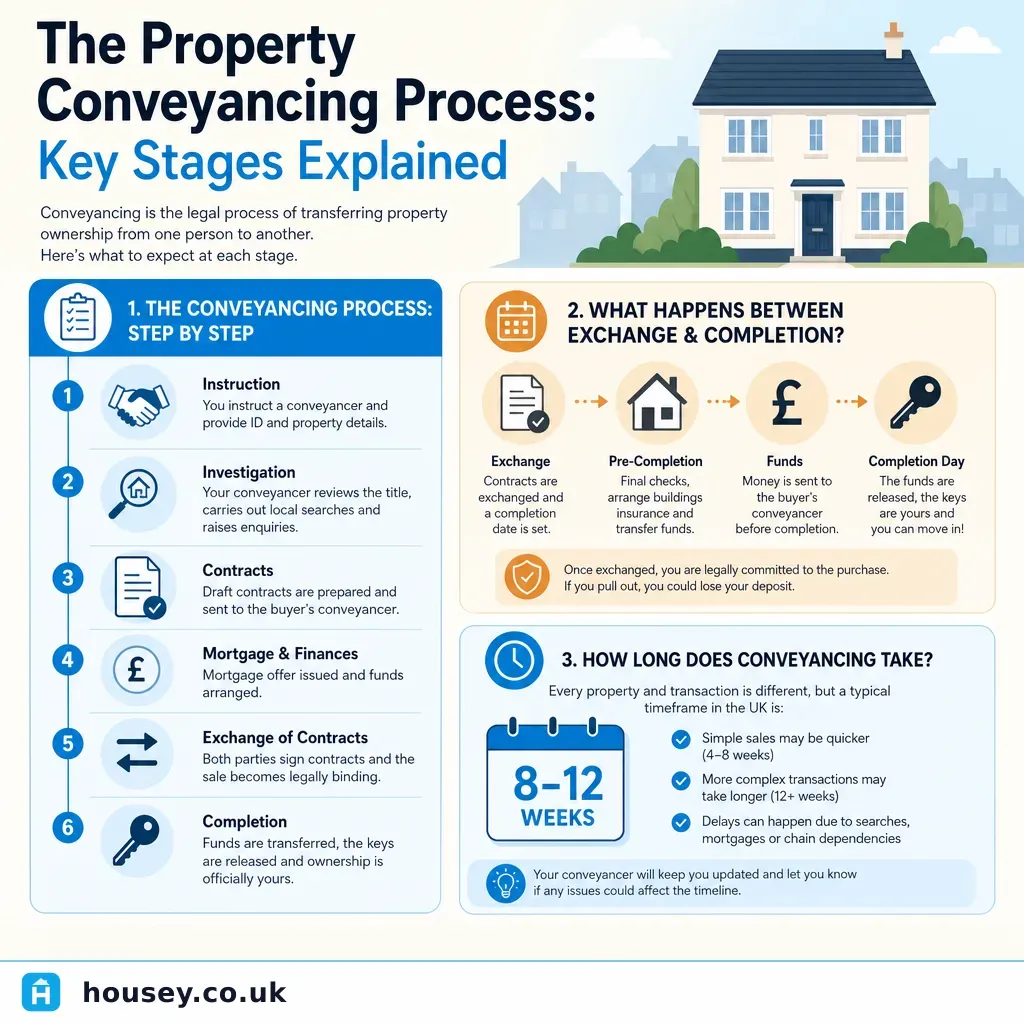

Buying & MovingThe Property Conveyancing Process: Key Stages Explained

The conveyancing process in England and Wales runs from instruction through to registration at HM Land Registry, typically in five stages: instruction, pre-contract searches and enquiries, exchange of contracts, completion, and post-completion.