How Home Security Improvements Can Reduce Insurance Costs

By Housey · Last reviewed 30th of May 2026

How Home Security Improvements Can Reduce Insurance Costs

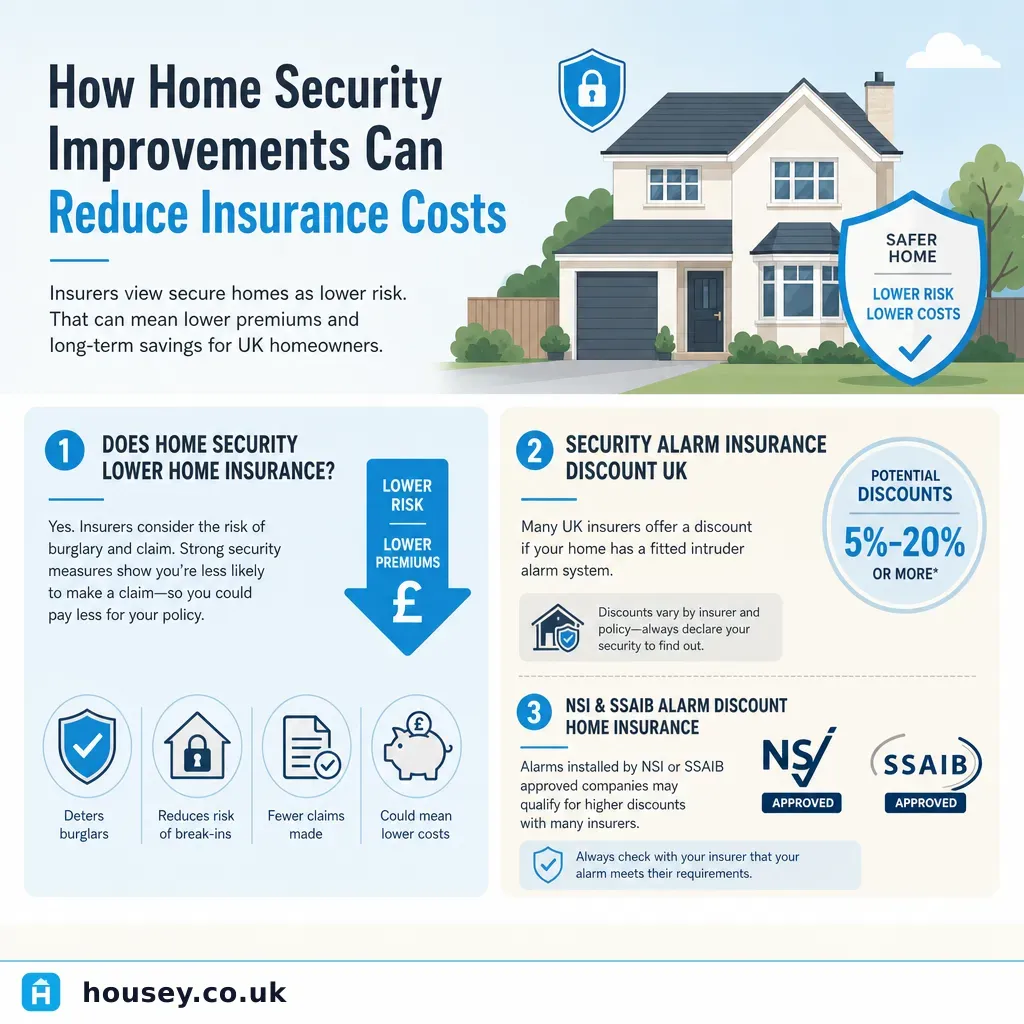

Home security upgrades and insurance pricing are closely linked in the UK — insurers view better-protected properties as lower risk and often price policies accordingly. The question typically arises at policy renewal, after a local incident, or when planning a renovation, and getting it right can make a meaningful difference to your annual premium.

Key points

- Many UK insurers offer premium reductions of 5–15% for homes with NSI or SSAIB-approved intruder alarms.

- Secured by Design (SBD) accreditation on doors and windows is recognised by a wide range of mainstream insurers as reducing break-in risk.

- BS 3621 five-lever mortice locks on external doors are often a policy condition — not meeting this standard can invalidate a claim, not merely affect a discount.

- CCTV and video doorbells may support a premium reduction, but typically attract smaller discounts than a monitored certificated alarm.

- Always confirm your insurer's exact qualifying criteria before spending money — not all products or installers will meet their standards.

What security measures typically qualify for discounts

Insurers assess risk based on the likelihood and potential severity of a claim. Upgrades that demonstrably reduce break-in risk are most likely to influence premiums. The three main categories are:

Alarm systems: Intruder alarms installed by firms certificated by the National Security Inspectorate (NSI) or the Security Systems and Alarm Inspection Board (SSAIB) attract the largest discounts. Monitored systems — where an alarm receiving centre alerts keyholders or police — are viewed more favourably than bells-only alarms. Many insurers will not discount self-installed smart alarms, even well-known brands, without formal certification.

Locks and physical security: Most standard home insurance policies in the UK require British Standard BS 3621 locks on external doors as a policy condition. Upgrading to multi-point locking systems on composite doors, fitting window locks, and securing outbuildings can all help. This is often a requirement before your insurer will pay a theft claim, not simply a discount trigger.

CCTV and video doorbells: Visible cameras deter opportunist theft and can assist police recovery. Discounts for CCTV vary widely by insurer. Registering cameras and serial numbers on the national Immobilise database is free and can support future claims.

Security measures and their typical insurance impact

Indicative discount ranges, last reviewed 2026-05-30. Insurers' criteria vary — always check your policy documentation.

Security measure | Typical insurer response | Estimated discount range | Key certification |

|---|---|---|---|

NSI/SSAIB monitored alarm | Usually reduces premium | 5–15% | NSI Gold or SSAIB certificate |

NSI/SSAIB bells-only alarm | Often reduces premium | 2–8% | NSI or SSAIB installation certificate |

Self-installed smart alarm | Varies; often no discount | 0–5% | Insurer-specific — confirm before buying |

BS 3621 locks on all external doors | Condition of cover | Avoids excess loading | BS 3621 mark on lock body |

Secured by Design doors or windows | Recognised by many insurers | 2–10% | SBD certificate from manufacturer |

Monitored CCTV | Increasingly recognised | 2–8% | Insurer-specific |

Neighbourhood Watch membership | Minor benefit | 1–3% | Neighbourhood Watch certificate |

NSI, SSAIB, and Secured by Design: what the certifications mean

The National Security Inspectorate (NSI) and the Security Systems and Alarm Inspection Board (SSAIB) are the two main UK certification bodies for security installers. An alarm installed by an NSI or SSAIB-certificated firm should come with documentation confirming the alarm grade under EN 50131 (typically Grade 2 or Grade 3). This paperwork is what most insurers will ask to see at renewal or claims stage.

Secured by Design (SBD) is a police-backed initiative administered by Police Crime Prevention Initiatives. Products carrying SBD accreditation — doors, windows, locks, and hardware — have passed independent testing. Many new-build developers apply for SBD accreditation; for existing properties, SBD-accredited replacement windows and doors are widely available from mainstream manufacturers.

Smart security and new technology

Smart alarms, video doorbells, and connected cameras have proliferated in recent years. Products from well-known consumer brands can offer genuine deterrence, but few carry NSI or SSAIB certification. Some insurers are beginning to recognise professionally monitored smart systems, but practice varies widely by provider.

Before purchasing any smart security device, contact your insurer with the exact product model and ask whether it qualifies for a premium reduction. This takes a few minutes and could influence your choice between a monitored professional system and a self-installed consumer device.

Homeowner security upgrade checklist

Before calling an installer or renewing your policy, work through this list:

What to ask your insurer before fitting security

- What alarm grade and certification standard do you require for a premium discount?

- Do you recognise both NSI and SSAIB certification, and to what grade?

- Will a self-installed monitored system qualify for a reduction?

- If I fit Secured by Design windows or doors, will that reduce my premium at renewal?

- What is the minimum lock standard I must maintain as a policy condition?

- Can a mid-policy security upgrade be reflected in my premium immediately?

- What documentation will you need to apply the discount?

When to get professional help

For most security upgrades, the main professional you need is an NSI or SSAIB-certificated alarm installer. Locate registered firms via the NSI approved company search or the SSAIB registered companies directory.

If your security review surfaces fire safety questions, professional advice is worth seeking. Red flags that indicate you should consult a qualified assessor:

- The property is a house in multiple occupation (HMO), where fire alarm obligations differ from a standard home.

- You are a landlord unsure of your duties under the Smoke and Carbon Monoxide Alarm (Amendment) Regulations 2022.

- A conversion or extension has changed the property's internal layout and potentially its fire escape routes.

- Your insurer has asked for evidence of a fire safety assessment as a condition of cover.

How Housey can help

If your security review raises questions about fire detection or safety — particularly after a conversion or in a rented property — Housey can connect you with qualified assessors for a professional fire risk assessment, helping you meet both insurer requirements and your legal obligations as a landlord or HMO owner.

Frequently asked questions

Does fitting a burglar alarm always reduce my home insurance premium?

Not automatically. Most mainstream UK insurers require the alarm to be installed and maintained by an NSI or SSAIB-certificated firm to qualify for a discount. Self-installed smart alarms may not qualify. Always confirm your insurer's specific requirements before committing to a purchase.

Can I get a discount mid-policy after fitting new security?

Often yes. Contact your insurer with evidence of the upgrade — such as an NSI or SSAIB installation certificate — and ask for the premium to be reviewed. Some insurers will adjust immediately; others apply changes only at renewal. Get any confirmation in writing.

What locks do I need to avoid an insurance policy loading?

Most UK home insurers require five-lever mortice deadlocks meeting BS 3621 on final-exit doors and key-operated locks on accessible windows. Check your policy's security conditions carefully — failing to meet these standards can invalidate a theft claim even while you are paying the full premium.

Is smart home security treated differently by insurers?

Currently, yes. Most UK insurers give larger discounts for traditionally certificated systems than for consumer smart-home devices. This is gradually changing as professional monitoring becomes more common in smart systems, but practice varies widely. Always confirm with your insurer before buying.

Sources and further reading

- Smoke and Carbon Monoxide Alarm (Amendment) Regulations 2022 — GOV.UK

- NSI: find an approved company — National Security Inspectorate

- SSAIB: find a registered company — SSAIB

- Secured by Design: product accreditation — Police Crime Prevention Initiatives

- Immobilise: national property register — Immobilise

Useful next reads

Surveys & Inspections

Surveys & InspectionsHome Security Systems and Protective Measures for UK Residential Properties

Effective home security in the UK combines physical deterrents — quality door locks and security lighting — with electronic systems such as intruder alarms and CCTV.

Surveys & Inspections

Surveys & InspectionsEnhancing Fire Safety in Your Property: Essential Steps and Compliance

Fire safety in UK properties is governed by Building Regulations Approved Document B and, for non-domestic and multi-occupied residential buildings, the Regulatory Reform (Fire Safety) Order 2005.

Surveys & Inspections

Surveys & InspectionsHow to Prepare Your Property Against Flooding and Water Damage

Preparing your property against flooding involves checking your flood risk zone, improving drainage, fitting flood barriers and air-brick covers, and reviewing your buildings insurance.

Surveys & Inspections

Surveys & InspectionsFire Safety in Buildings: Assessment, Compliance, and Risk Management

The Regulatory Reform (Fire Safety) Order 2005 requires most non-domestic and multi-occupied residential buildings to have a written fire risk assessment carried out by a competent person.

Surveys & Inspections

Surveys & InspectionsUnderstanding Homeowner Insurance Coverage for Water Damage Claims

UK buildings insurance typically covers sudden water damage such as burst pipes, escape of water from appliances, and storm-damaged roofs.