Understanding Homeowner Insurance Coverage for Water Damage Claims

By Housey · Last reviewed 19th of May 2026

Understanding Homeowner Insurance Coverage for Water Damage Claims

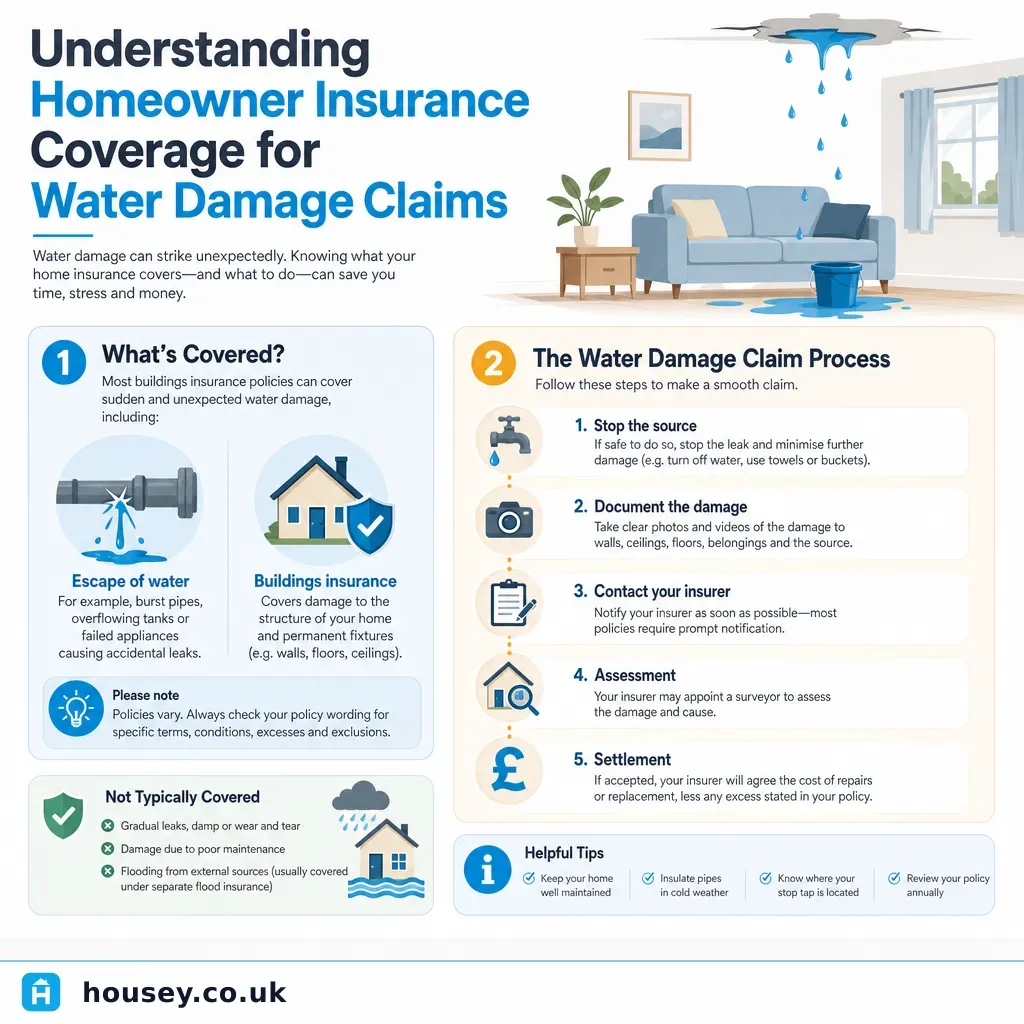

Water damage is one of the most common reasons UK homeowners make an insurance claim, but whether a claim succeeds depends critically on how the damage occurred, when it was reported, and what policy you hold. The difference between a successful claim and a rejected one often comes down to details — how quickly you acted, whether the cause counts as sudden or gradual, and whether you have the right type of cover in place.

Key points

- "Escape of water" is the standard insurance term for water damage from burst pipes, leaking appliances, or overflowing tanks — it is covered by most UK buildings insurance policies as a named peril.

- Gradual or seeping leaks caused by maintenance failures, wear and tear, or rot are typically excluded from buildings insurance cover.

- External flooding (surface water, rivers, coastal) is usually a separate peril; properties in high flood-risk zones may rely on the Flood Re scheme for affordable cover.

- Buildings insurance covers the structure; contents insurance covers belongings — most comprehensive water damage scenarios require both policies to respond.

- If your buildings sum insured is set below the true rebuild cost, insurers may apply a proportional reduction (known as "average") to any claim payout.

What types of water damage are typically covered?

Most UK buildings insurance policies cover sudden, accidental water damage to the fabric of the building. Understanding the difference between covered and excluded causes is essential before you make or challenge a claim.

Cause of water damage | Typically covered? | Key condition | Notes |

|---|---|---|---|

Burst pipe (sudden) | Yes | Report promptly | Standard named peril on most policies |

Frozen and burst pipe | Yes | Reasonable precautions taken | Leaving a home unheated for extended periods may invalidate a claim |

Leaking appliance (sudden fault) | Yes | Appliance properly maintained | Check policy for accidental damage inclusion |

Gradual or slow leak | No | — | Excluded as a maintenance failure |

Storm-driven rain entering | Yes | Via storm damage to roof or windows | Damage must result from the storm event itself |

External flooding (river, surface water) | Depends on policy | Flood cover included | Check policy wording; Flood Re may apply to eligible properties |

Escape of water from neighbour's flat | Often covered | Trace and access clause may help | Liability usually lies with the neighbour's insurer |

Condensation or damp (gradual) | No | — | Excluded as wear and tear |

What to do immediately when water damage occurs

Acting quickly reduces damage and protects your claim. Work through this checklist before calling a contractor:

Homeowner water damage checklist

Red flags that suggest your claim may be disputed

These situations do not automatically mean a claim will be rejected, but they commonly lead to insurers requesting additional evidence or disputing liability:

- The damage has been visible or present for weeks or months before it was reported.

- You cannot identify the precise cause or the date of the water ingress.

- There is evidence of long-term damp, staining, or maintenance neglect behind or around the damage.

- The property was left unoccupied for longer than the period stated in your policy (commonly 30 or 60 days).

- You arranged significant remedial work before the loss adjuster carried out an inspection.

- The cause is confirmed by a specialist as a slow or gradual leak rather than a sudden event.

Understanding rebuild costs and avoiding underinsurance

Buildings insurance is designed to cover the full cost of rebuilding your home from the foundations, not its market value. If your sum insured is too low — a common consequence of policies being auto-renewed without review — insurers may apply proportional reduction to a payout. For example, if your home would cost £300,000 to rebuild but you are insured for £200,000, a £30,000 water damage claim could be reduced to £20,000.

An insurance rebuild cost assessment carried out by a RICS-accredited surveyor gives you a current, compliant reinstatement figure, protecting you against underinsurance when you need it most.

When to get professional help

Seek professional advice if:

- A loss adjuster has disputed your claim or offered a settlement lower than you expect — a public loss assessor can represent your interests.

- There is evidence of damp, mould, or timber decay following water damage — a damp and timber survey can identify the extent before remediation begins.

- The water appears to have originated from a drain, sewer, or external pipe — a CCTV drain survey can pinpoint the source and establish where responsibility lies.

- You are unsure whether your buildings sum insured reflects current rebuild costs, particularly after an extension or renovation.

- The damage involves a party wall or neighbouring property, where liability may need to be apportioned formally.

How Housey can help

Getting the right assessment after water damage can protect your claim and prevent hidden problems from worsening. Housey connects you with insurance rebuild cost surveyors who can confirm your sum insured is correct, and damp and timber specialists who can assess secondary damage that may not be visible to the naked eye.

Frequently asked questions

Does buildings insurance cover escape of water from a neighbour's flat above mine?

In most cases, your own buildings insurance can respond to damage to your property even if the escape originated in a neighbour's flat. Your insurer will typically seek to recover costs from the neighbour's insurer under the principle of subrogation. If you are a leaseholder, check whether the freeholder's buildings policy covers the whole building — many leasehold blocks have a single policy applying to all units.

How long do I have to make a water damage claim?

There is no fixed legal deadline, but most policies include a condition requiring you to report damage as soon as reasonably practicable. The Financial Ombudsman Service considers whether any delay caused the insurer to suffer prejudice. As a practical rule, report as soon as you discover damage and certainly within days rather than weeks of the incident occurring.

What is the difference between buildings and contents insurance for water damage?

Buildings insurance covers the structure and permanent fixtures — walls, ceilings, floors, fitted kitchens, and bathrooms. Contents insurance covers moveable possessions — furniture, electronics, clothing, and often carpets. A burst pipe may damage the plasterwork (a buildings claim) and the sofa beneath it (a contents claim). Both policies may need to respond to a single incident.

Will making a water damage claim affect my renewal premium?

Most insurers treat escape of water claims as part of your claims history, which can lead to higher premiums or a higher excess at renewal. Under FCA conduct rules (ICOBS), insurers must treat customers fairly. It is worth comparing quotes at renewal and explaining the circumstances of the claim to brokers who can access specialist markets.

Sources and further reading

- Home insurance guidance for consumers — Association of British Insurers

- Flood Re: the UK flood reinsurance scheme — Flood Re

- Making a home insurance claim — Citizens Advice

- FCA ICOBS: Insurance Conduct of Business Sourcebook — Financial Conduct Authority

- Reinstatement cost assessments of buildings — RICS

Useful next reads

Surveys & Inspections

Surveys & InspectionsHow Home Security Improvements Can Reduce Insurance Costs

Installing NSI or SSAIB-approved intruder alarms, BS 3621 locks, and CCTV can reduce UK home insurance premiums by 5–15% depending on your insurer.

Surveys & Inspections

Surveys & InspectionsHome Security Systems and Protective Measures for UK Residential Properties

Effective home security in the UK combines physical deterrents — quality door locks and security lighting — with electronic systems such as intruder alarms and CCTV.

Surveys & Inspections

Surveys & InspectionsEnhancing Fire Safety in Your Property: Essential Steps and Compliance

Fire safety in UK properties is governed by Building Regulations Approved Document B and, for non-domestic and multi-occupied residential buildings, the Regulatory Reform (Fire Safety) Order 2005.

Surveys & Inspections

Surveys & InspectionsHow to Prepare Your Property Against Flooding and Water Damage

Preparing your property against flooding involves checking your flood risk zone, improving drainage, fitting flood barriers and air-brick covers, and reviewing your buildings insurance.

Surveys & Inspections

Surveys & InspectionsFire Safety in Buildings: Assessment, Compliance, and Risk Management

The Regulatory Reform (Fire Safety) Order 2005 requires most non-domestic and multi-occupied residential buildings to have a written fire risk assessment carried out by a competent person.