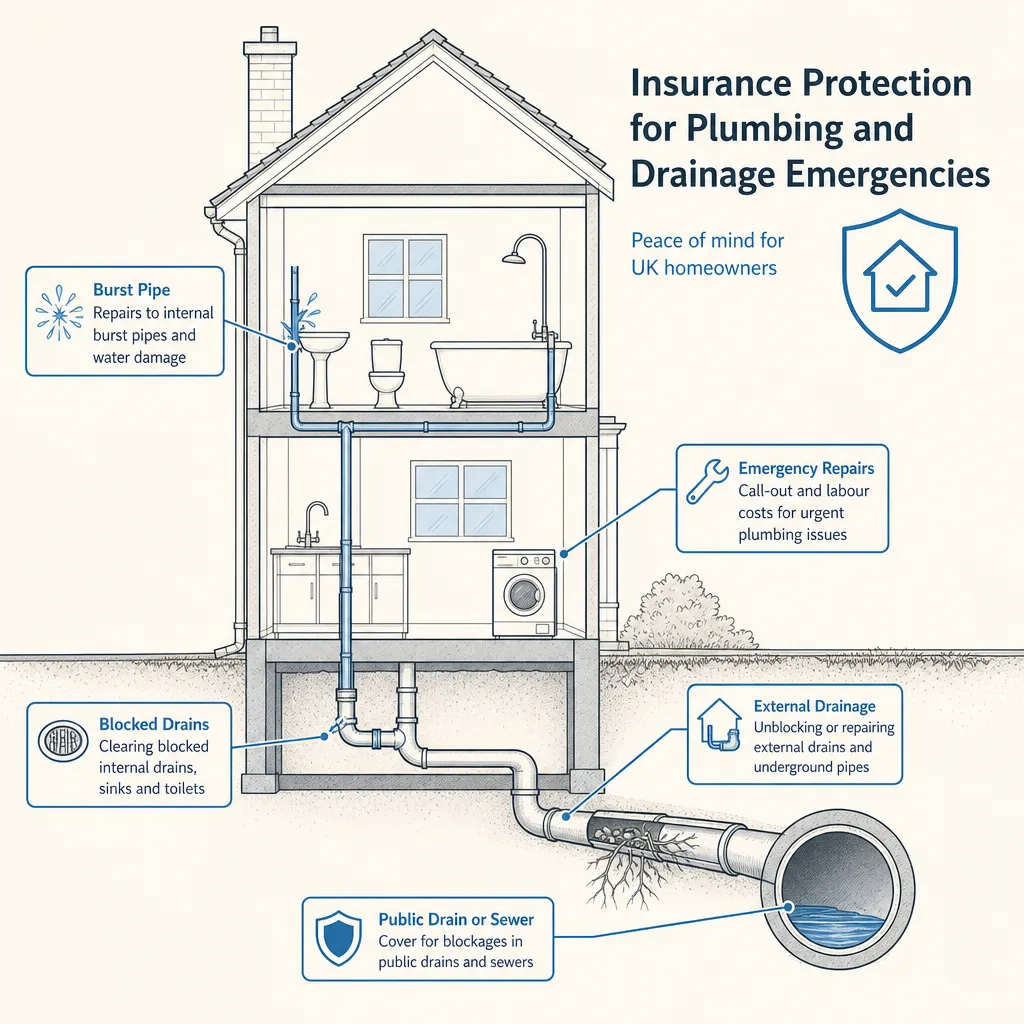

Insurance Protection for Plumbing and Drainage Emergencies

By Housey · Last reviewed 11th of May 2026

Insurance Protection for Plumbing and Drainage Emergencies

Plumbing and drainage problems rarely give advance warning — a burst pipe on a winter weekend or a blocked main drain can cause thousands of pounds of damage before a tradesperson arrives. Understanding the difference between standard home insurance and a separate home emergency policy before a problem occurs means you can act quickly and avoid disputes over what your insurer will pay. This distinction matters whether you own a Victorian terrace with ageing lead pipework, a 1970s semi with a history of root intrusion, or a modern new-build where cover arrangements are still being established.

Key points

- Standard buildings insurance typically covers sudden and accidental escape of water (for example, a burst pipe) but generally excludes gradual leaks, wear and tear, and blockages that develop over time.

- Home emergency cover is a distinct product — often sold as a policy add-on — that pays for emergency call-outs, temporary repairs, and sometimes overnight accommodation if the home is uninhabitable.

- Since October 2011, responsibility for lateral drains and shared sewers transferred to the local water company under the Water Industry Act 1991 (amended by the Water Industry (Schemes for Adoption of Private Sewers) Regulations 2011); homeowners are generally responsible only for drains within their property boundary.

- Policy excesses on buildings claims for water damage commonly range from £250 to £500; home emergency policies often carry a lower or zero excess but cap individual call-out costs at £500–£1,000.

- The Association of British Insurers (ABI) distinguishes escape of water (a named buildings insurance peril) from home emergency assistance (a separate service product with its own exclusions and call-out limits).

What standard home insurance covers — and what it does not

Most UK buildings insurance policies include escape of water as a named peril. This typically covers sudden damage caused by a burst or frozen pipe, water damage to floors, ceilings, and walls resulting from the escape, and sometimes the cost of locating and accessing the source of the leak (trace-and-access cover, though this is often a paid add-on rather than standard).

What standard buildings insurance usually excludes:

- Gradual deterioration, seepage, or slow leaks that built up over time.

- Blocked drains, unless the blockage directly causes a sudden flood event and measurable structural damage.

- Damage caused by lack of maintenance — insurers may argue a foreseeable problem was not attended to.

- The failed component itself (the pipe, tap, or boiler) — only the resulting water damage to the building is typically covered.

- Drains and pipework outside your legal property boundary.

Contents insurance covers possessions damaged by water but does not pay for building repairs. Always check your specific policy wording — exclusions vary considerably between insurers.

What home emergency cover adds

Home emergency cover is designed to get a qualified tradesperson to your door quickly and carry out a temporary or permanent fix. Typical cover includes emergency plumber call-outs for burst pipes or loss of water supply, drainage engineers for blocked or collapsed drains within your boundary, labour and parts up to stated policy limits (commonly £500–£1,000 for labour and £250–£500 for parts), and alternative accommodation if the property is uninhabitable.

Common exclusions in home emergency policies include pre-existing conditions (most policies exclude problems that existed before the policy start date), drains beyond the property boundary, cosmetic repairs after the emergency is made safe, and damage to fixtures or contents (which falls to buildings and contents insurance respectively).

Who owns your drains? Property boundary rules

Under the Water Industry Act 1991, as amended by the Water Industry (Schemes for Adoption of Private Sewers) Regulations 2011, the dividing line between homeowner and water company responsibility is as follows:

- Your responsibility: the drain serving only your property, from where it leaves your house to the boundary of your curtilage.

- Water company's responsibility: lateral drains and shared sewers were transferred to regional water companies in October 2011. Thames Water, Anglian Water, Severn Trent, and others now maintain and repair these at no charge to the homeowner.

If a drainage problem appears to extend beyond your boundary, contact your regional water company directly before instructing a private contractor. You should not need to pay for repair of that section.

Home insurance vs. home emergency cover

Feature | Standard buildings insurance | Home emergency cover |

|---|---|---|

Burst pipe damage | Usually covered (escape of water peril) | Call-out and temporary fix covered |

Blocked drain | Usually excluded unless causes sudden flood | Usually covered (within boundary) |

Gradual leak damage | Usually excluded | Usually excluded (pre-existing condition) |

Labour cost | Not applicable — damage repair only | Covered to policy limit (often £500–£1,000) |

Parts replacement | Not applicable | Covered to separate limit (often £250–£500) |

Out-of-hours response | No — you arrange contractors | Yes — 24/7 helpline typical |

Excess | Typically £250–£500 | Often £0–£100 |

Approximate annual cost | Included in buildings premium | £60–£180 standalone approx |

Indicative UK costs, last reviewed 2026-05-11. Premiums and limits vary by insurer, property type, and claims history.

Homeowner checklist: before and after a plumbing or drainage emergency

Before an emergency:

When an emergency happens:

After the emergency:

Red flags that suggest a more serious problem

Contact a qualified drainage contractor promptly if you notice:

- Slow or recurring blockages that return despite clearing — this may indicate a partial pipe collapse, root ingress, or incorrect gradient.

- Subsidence near drain runs — settlement or sinking ground above buried pipes can signal a collapsed or leaking sewer.

- Sewage smell inside or outside the property without an obvious blocked gully — this can indicate a cracked pipe or failed joint below ground.

- Gurgling from multiple fixtures simultaneously — a sign of a shared drain problem rather than a localised blockage.

- Damp patches on ground-floor walls near soil pipes or rodding-eye covers.

These symptoms may require a CCTV drain survey rather than a simple unblock, and the findings may affect an insurance claim or a property sale.

When to get professional help

Call a qualified drainage contractor if you cannot clear a blockage with standard household methods, if there is any sign of sewage or foul water entering the property, if you suspect a collapsed or cracked pipe (evidenced by subsidence or persistent wet ground), or if you are buying or selling a property and want to confirm the condition of underground drainage before exchange.

How Housey can help

If you need a qualified professional to inspect, unblock, or repair your drainage system, Housey can connect you with vetted drainage contractors who carry relevant trade accreditations and public liability insurance. You can compare quotes before committing to any work.

Frequently asked questions

Does home insurance cover a blocked drain?

Most standard buildings insurance policies exclude blocked drains unless the blockage directly causes sudden accidental damage such as a flood that damages floors or walls. A home emergency add-on or standalone policy is more likely to cover the call-out and unblocking cost. Always check your specific policy schedule for the wording on drainage cover.

Who is responsible for drains outside my property boundary?

Since October 2011, lateral drains and shared sewers outside your property boundary are the responsibility of your regional water company under the Water Industry (Schemes for Adoption of Private Sewers) Regulations 2011. Contact your water company directly — you should not need to pay a private contractor for faults in that section.

Can I claim on both home insurance and home emergency cover for the same incident?

Possibly, for different elements. Home emergency cover typically pays for the call-out, labour, and temporary repair; buildings insurance then covers resulting structural damage. Inform both insurers and follow each insurer's claims process. Avoid starting significant repair work without prior insurer agreement, as unilateral repairs can affect a claim.

Is trace-and-access cover worth adding to my buildings policy?

For properties with older or concealed pipework — a Victorian terrace with lead or clay pipes under a solid floor, for example — trace-and-access cover can be valuable. Identifying a hidden leak may require cutting through tiles, lifting floors, or excavating, and these investigation costs can run to several hundred pounds before any repair begins.

What can I do if my insurer disputes whether damage was sudden or gradual?

Gather evidence of when damage was first noticed: dated photographs, CCTV drain survey reports, and contractor invoices all help establish a timeline. The Financial Ombudsman Service adjudicates insurance disputes free of charge to the consumer once the insurer's internal complaints process has been completed.

Sources and further reading

- Buildings insurance consumer information — Association of British Insurers

- Water Industry Act 1991 — legislation.gov.uk

- Sewers and drains: your responsibilities — GOV.UK

- Water Industry (Schemes for Adoption of Private Sewers) Regulations 2011 — legislation.gov.uk

- Insurance complaints — Financial Ombudsman Service

Useful next reads

Improvement & Build

Improvement & BuildRetaining Wall Installation: Cost, Design and Maintenance

A retaining wall holds back soil on a sloped or banked site.

Improvement & Build

Improvement & BuildRepiping Your Home: Water Supply Line Replacement

Repiping is typically needed when lead, iron, or early polybutylene pipes corrode, leak, or restrict flow.

Improvement & Build

Improvement & BuildPervious Concrete Surfaces: Modern Sustainable Driveway Solutions

Pervious concrete (also called porous or no-fines concrete) is a specialist concrete mix with large voids that allow rainwater to pass through the surface and into the sub-base below.

Improvement & Build

Improvement & BuildRelocating a Bathroom: When to Hire a Plumber Versus a Bathroom Specialist

Relocating a bathroom usually requires both a qualified plumber for pipework and drainage and other specialist trades for electrics, tiling, and finishes.

Improvement & Build

Improvement & BuildImproving Your Driveway: Options, Costs and Considerations

Installing a new driveway with a non-permeable surface larger than 5m² over a front garden in England requires planning permission unless water drains to a permeable area.