London Property Market Conditions And Buyer Advisory For Investors

By Housey · Last reviewed 18th of May 2026

London Property Market Conditions And Buyer Advisory For Investors

London's property market sits in a category of its own within the UK — characterised by wide price variation between boroughs, a high proportion of leasehold flats, and market dynamics that can differ substantially from national trends. For buyers and investors, decisions made without proper independent professional advice on valuation, condition, and legal structure carry material financial risk, and the complexity of the London market makes that advice especially important.

Key points

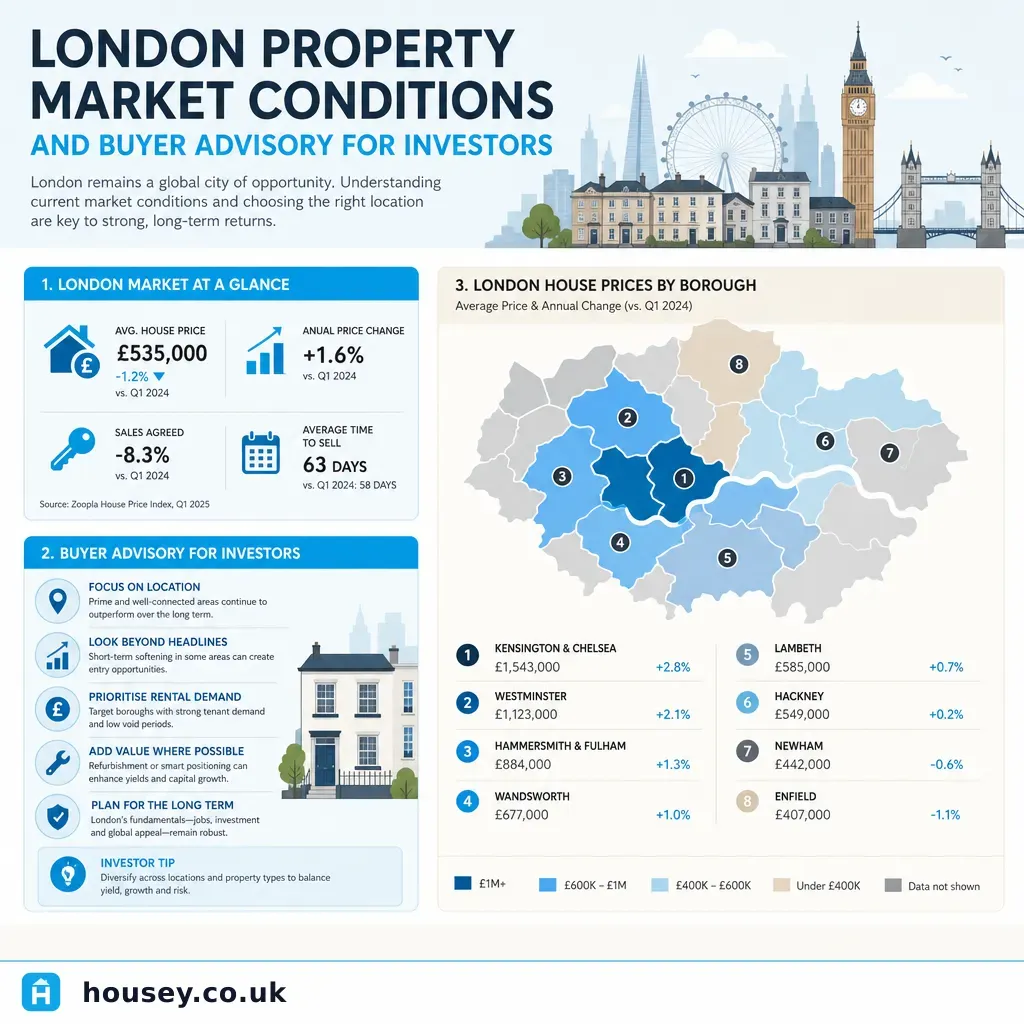

- The average London house price was approximately £526,000 as at early 2026 (HM Land Registry UK House Price Index), but borough-level averages range from below £300,000 in some outer boroughs to over £1,000,000 in prime inner London areas.

- Approximately 40% of London's housing stock is leasehold — predominantly flats — meaning buyers must assess ground rent terms, service charges, and unexpired lease length before committing.

- Under the Leasehold Reform (Ground Rent) Act 2022, ground rents on new residential leases are capped at a peppercorn (effectively zero); existing leases may still carry escalating ground rent clauses.

- A lease with fewer than 80 years remaining attracts marriage value in any lease extension premium calculation, significantly increasing cost — lenders may also decline to lend below 70 years.

- For flats in buildings above 11 metres, an EWS1 (External Wall Fire Review) assessment may be required by lenders and insurers — buyers should check building safety status before instructing a survey.

Understanding London's market geography

London's property market is not one market — it is a collection of micro-markets that respond differently to interest rate changes, employment shifts, transport investment, and planning policy.

Area type | Characteristics | Key buyer considerations |

|---|---|---|

Central London (Zone 1–2) | High prices, strong international demand, predominantly flats, many long leaseholds | Lease length critical; service charges can be substantial; SDLT materially higher above £500,000 threshold |

Inner boroughs (Zone 2–3) | Victorian and Edwardian terraces and conversions; inter-war semis; strong rental demand | RICS Level 3 survey recommended for older stock; conservation area restrictions common; check permitted development history |

Outer boroughs (Zone 3–6) | Greater mix of houses and flats; wider price range; commuter-driven demand; more new-build | New-build valuation gap to resales; leasehold new-build houses to avoid; check Help to Buy repayment terms if applicable |

New-build developments (all zones) | Often leasehold, developer-set service charges, ground-floor retail complications | Always commission independent valuation; do not rely solely on developer-recommended solicitors or valuers |

How London's leasehold market affects buyers

A significant proportion of London property — particularly flats — is sold on a leasehold basis. This is a legal structure, not a defect, but it creates obligations and risks that freehold property does not.

Key leasehold considerations for London buyers:

- Lease length: below 80 years remaining means marriage value applies in any extension premium calculation, significantly increasing cost. Lenders commonly require a minimum of 70 years at the point of mortgage application.

- Ground rent: check whether the existing lease has fixed, RPI-linked, or doubling ground rent clauses. Doubling ground rent leases — where the rent doubles more than every 20 years — are widely regarded as difficult to mortgage and sell.

- Service charge: annual service charge is an additional ongoing cost, and major works contributions (served via a section 20 notice under the Landlord and Tenant Act 1985) can amount to tens of thousands of pounds. Request three years of accounts and ask specifically about any anticipated section 20 notices.

- Building safety: for flats in buildings above 11 metres, check EWS1 status and whether the building is enrolled in a government remediation scheme under the Building Safety Act 2022. This affects insurability and mortgage availability.

- Share of freehold: some London flats have a share of freehold, giving leaseholders more collective control. This is generally preferable but adds complexity if alterations or lease extensions are planned.

Which survey do you need for a London property?

Survey selection should be driven by the property's age, construction type, and visible condition — not by asking price.

Decision tree: which survey is appropriate?

- Is the property a purpose-built flat in a post-1980 block in apparent good condition? → A RICS Level 2 Home Survey is usually sufficient.

- Is the property a Victorian or Edwardian conversion flat, or a period terrace? → A RICS Level 3 Building Survey is recommended — hidden defects and historic alterations are common in this stock.

- Are there visible cracks, damp staining, suspected roof problems, or evidence of structural movement? → RICS Level 3 Building Survey, possibly supplemented by a structural engineer's input.

- Is the property in a building above 11 metres? → Check EWS1 status before commissioning a survey — building safety position may be more material than physical condition findings.

- Is the property listed, a mansion flat conversion, an ex-local authority flat, or a converted commercial building? → Consider a structural survey in addition to, or instead of, a standard RICS survey, as construction and condition issues may be atypical.

- Do you need a professional view on market value for negotiation, at auction, or in an off-market transaction? → Commission an independent valuation survey — a mortgage valuation is not a substitute.

Red flags when buying a London property

These indicators warrant further investigation before exchange:

- Short lease (under 85 years remaining): cost of extension and risk of an unmortgageable position should be priced into any offer — obtain a LEASE estimate or specialist leasehold solicitor advice before proceeding

- Escalating ground rent clauses: any lease where ground rent doubles more than every 20 years is problematic for mortgageability and resale

- Missing building regulations completion certificates: indicates prior works were carried out without approval — may require indemnity insurance or a retrospective regularisation application

- Section 20 notice outstanding or expected: you could inherit a major works liability of thousands of pounds — ask the managing agent directly and in writing

- No EWS1 or an EWS1 with a B2 or C rating: some lenders and insurers may decline cover; remediation timescales are uncertain

- High or rising service charge with a low sinking fund balance: check the reserve fund level; a building with a near-zero sinking fund and high service charge suggests deferred maintenance

- Flood risk: check the Environment Agency Flood Map for Planning and the seller's TA6 property information form disclosures

- Japanese knotweed: TA6 disclosure is required; specialist treatment and mortgage restrictions may apply

Important limitations

The information in this article is general guidance for educational purposes only. London property values, leasehold legislation, building safety rules, and market conditions change, and the specific circumstances of any individual transaction — including legal title, physical condition, planning history, leasehold terms, and building safety status — require professional assessment.

This article does not constitute financial, investment, or legal advice. Rules and risks vary significantly by property, borough, tenure, and transaction type. Any decision to purchase London property should be taken with the benefit of independent professional advice appropriate to your specific circumstances.

What to ask a qualified professional

Questions to ask your surveyor or valuer before instructing:

- What level of survey is appropriate for this specific property, construction type, and age?

- Are there aspects of the property that cannot be inspected, and what are the implications?

- What is your view on the property's condition relative to the asking price?

- Are there any defects likely to affect mortgage lending or resale value?

- Are there signs of historic or active structural movement?

Questions to ask your solicitor or conveyancer:

- What is the unexpired lease term, and what is the indicative cost of a lease extension?

- Are there any unusual ground rent provisions or service charge clauses I should be aware of?

- Has the property received building regulations completion certificates for any works?

- Is there a section 20 notice pending, expected, or recently served?

- Are there any restrictions on subletting, use, or alterations in the lease?

Questions to ask the managing agent or freeholder (for leasehold flats):

- What is the current annual service charge and what does it cover?

- What is the current balance of the sinking or reserve fund?

- Has an EWS1 assessment been carried out, and what was the outcome?

- Are any major works planned or anticipated in the next three years?

When to get professional help

You should always seek independent professional advice before exchanging contracts on a London property:

- Commission a RICS Home Survey appropriate to the property's age and condition — a lender's mortgage valuation is not a substitute for your own survey

- For older properties, unusual construction, or where defects are suspected, a structural survey provides more detailed engineering analysis than a standard RICS Level 2 report

- Where lease length is below 85 years, ground rent clauses are unusual, or service charge history is unclear, instruct a specialist leasehold solicitor to review documents before exchange

- For off-market transactions, auction purchases, or where you are negotiating a price reduction based on condition, an independent valuation survey provides the professional evidence to support your position

How Housey can help

Housey connects buyers and investors with qualified surveyors and valuers across London. Whether you need a RICS Home Survey, an independent valuation survey, or a detailed structural survey for an older or unusual property, submit a job request to receive quotes from vetted local professionals.

Frequently asked questions

How long does a RICS survey take for a London property?

The physical inspection typically takes 2–4 hours for a flat or smaller house, and up to a full day for a large or complex property. The written report is usually delivered within 3–5 working days of inspection, though this varies by surveyor and workload. For properties with building safety concerns — such as those requiring EWS1 review — additional time should be allowed.

Is a mortgage valuation the same as a survey?

No. A mortgage valuation is carried out for the lender's benefit to confirm the property provides adequate security for the loan. It is not a detailed inspection and will not identify all defects. You should always commission your own independent survey in addition to any mortgage valuation — the two documents serve entirely different purposes and protect different parties.

What is Stamp Duty Land Tax (SDLT) on a London property?

SDLT applies to residential purchases above £125,000 in England. Rates rise progressively above £250,000. An additional 3% surcharge applies on the entire purchase price if you already own another residential property. First-time buyers benefit from relief up to £500,000. SDLT rates and thresholds are set by HMRC and can change — always check current rates on GOV.UK before budgeting.

Should I use a buying agent when purchasing in London?

A buying agent works exclusively for the purchaser and can provide access to off-market properties and negotiation expertise in a competitive market. Fees are material — typically 1–2% of purchase price plus VAT — so the value depends on the agent's specific expertise in your target area and price range. For straightforward open-market purchases, an experienced solicitor and independent surveyor may be sufficient.

Sources and further reading

- UK House Price Index — HM Land Registry — HM Land Registry

- Leasehold Reform (Ground Rent) Act 2022 — legislation.gov.uk

- EWS1 external wall fire review — RICS guidance — RICS

- Stamp Duty Land Tax rates — GOV.UK — GOV.UK

- Leasehold Advisory Service (LEASE) — Leasehold Advisory Service

- Environment Agency Flood Map for Planning — Environment Agency

Useful next reads

Buying & Moving

Buying & MovingIdentifying and Resolving Delays in Property Transactions

Delays in UK property transactions most often arise from slow local authority searches, incomplete identity documents, mortgage hold-ups, leasehold complications, or a problem elsewhere in the chain.

Buying & Moving

Buying & MovingAcquiring Multiple Properties in the Cotswolds: Conveyancing and Bulk Transaction Essentials

Acquiring multiple Cotswolds properties in one transaction requires specialist conveyancing for each title, careful attention to SDLT — Multiple Dwellings Relief was abolished for most transactions from June 2024 — and awareness of listed building and conservation area constraints.

Buying & Moving

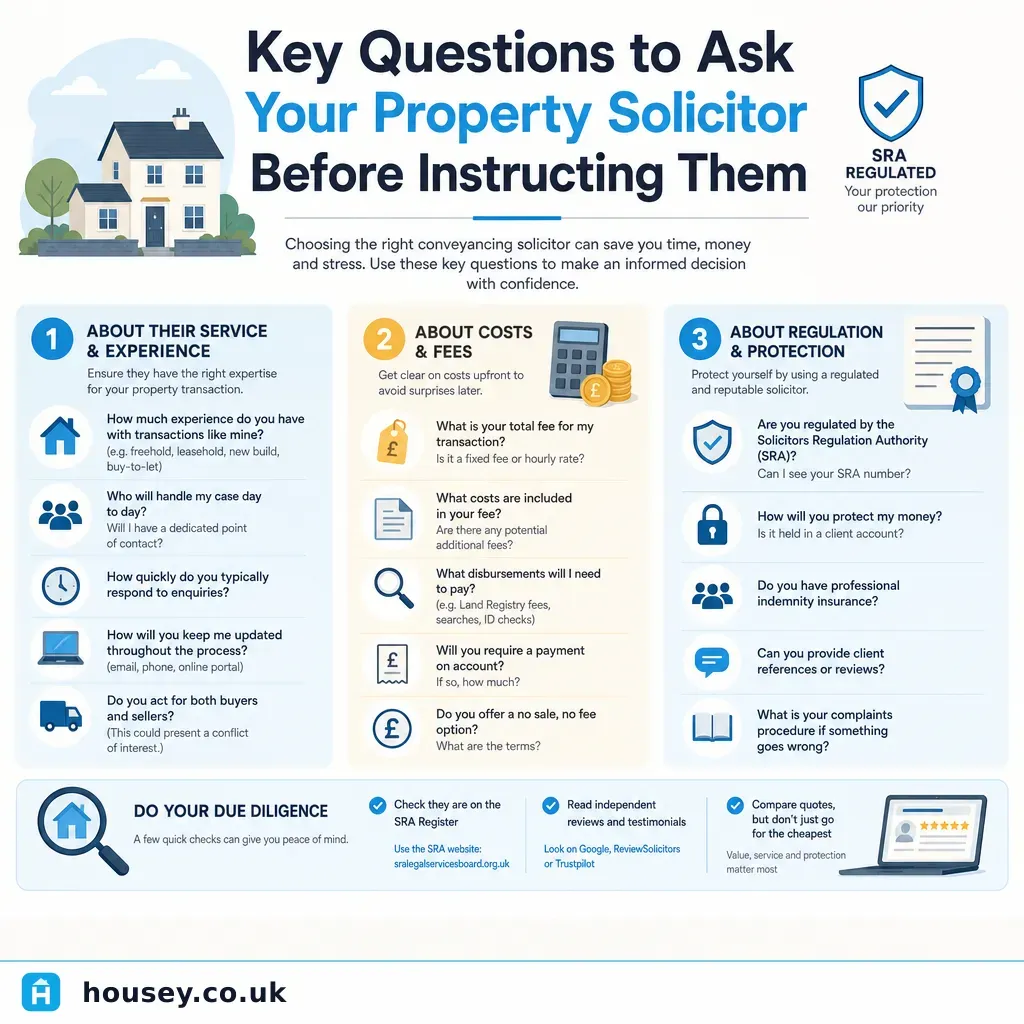

Buying & MovingKey Questions to Ask Your Property Solicitor Before Instructing Them

Before instructing a property solicitor, ask whether they are on your mortgage lender's approved panel, whether their quote is fixed and includes VAT and all disbursements, who will personally handle your case, and what their abortive-fee policy is.

Buying & Moving

Buying & MovingHow to Choose a Qualified Conveyancing Solicitor

To choose a qualified conveyancing solicitor, verify they are regulated by the Solicitors Regulation Authority (SRA) or the Council for Licensed Conveyancers (CLC), check whether they hold Law Society CQS accreditation, and confirm they are on your mortgage lender's approved panel.

Buying & Moving

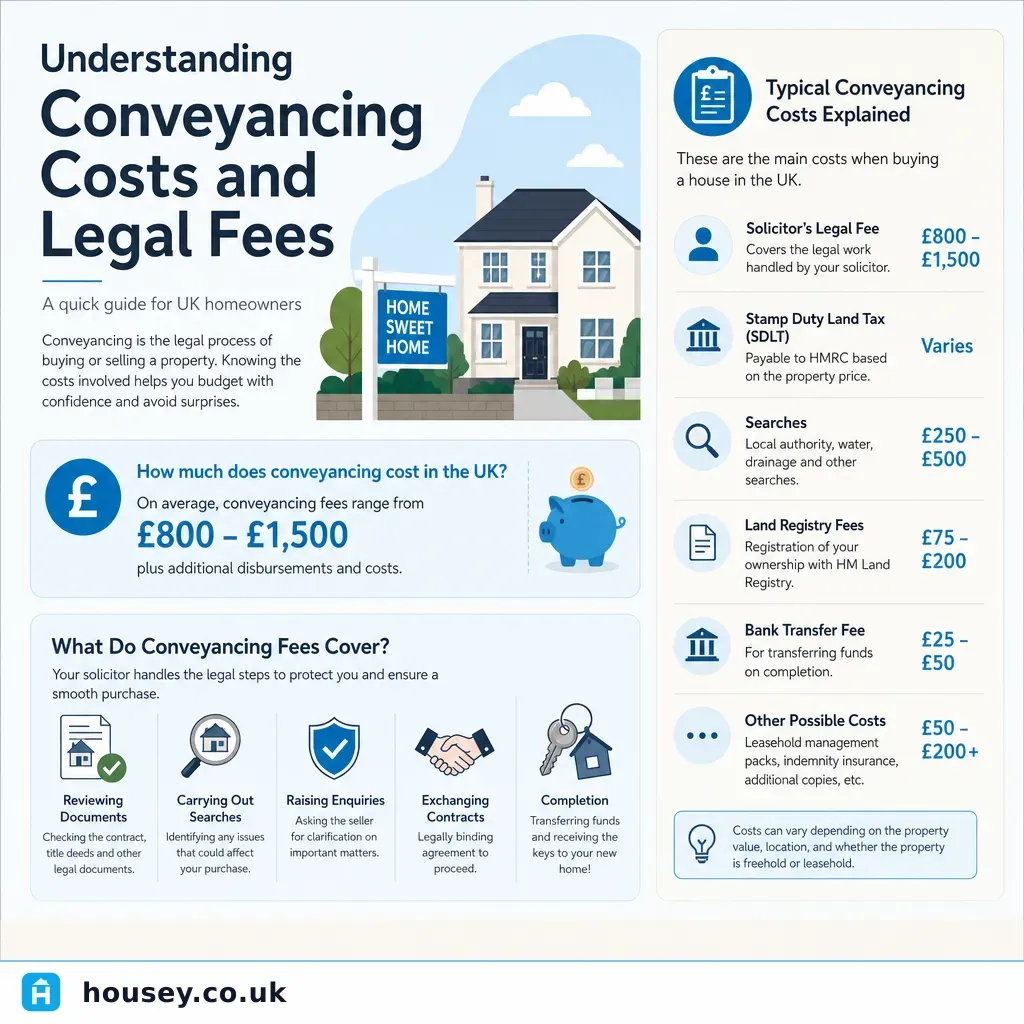

Buying & MovingUnderstanding Conveyancing Costs and Legal Fees

Conveyancing costs in England and Wales include a solicitor's or licensed conveyancer's professional fee plus disbursements such as searches, Land Registry registration, and bank transfer charges.