Market Analysis: How Recent Events Impact Property Asking Prices

By Housey · Last reviewed 10th of May 2026

Market Analysis: How Recent Events Impact Property Asking Prices

Setting or interpreting an asking price in a moving market is one of the most consequential decisions a UK buyer or seller faces. Economic headlines about interest rates, employment, and inflation all feed into buyer confidence and purchasing power — but the chain from event to changed asking price is not always direct or immediate. Understanding the transmission mechanism helps sellers price with more confidence and buyers avoid misjudging a market on the basis of stale data.

Key points

- The Bank of England base rate is the single most watched indicator for UK property prices: a 0.25 percentage point change can shift the maximum mortgage a typical buyer qualifies for by thousands of pounds at mid-range loan sizes.

- The ONS UK House Price Index tracks completed sale prices registered at HM Land Registry; Rightmove and Zoopla track asking prices — both are useful, but they measure different things and can diverge significantly in fast-moving conditions.

- Stamp Duty Land Tax (SDLT) changes — such as the temporary first-time buyer relief that ended in March 2025 — produce marked short-term demand spikes followed by corrections once the deadline passes.

- Local economic events, including major employer closures or expansions and confirmed infrastructure announcements such as new rail links, can move asking prices in specific postcode areas independently of national trends.

- EPC rating has become a material factor in buyer willingness to pay since lenders began linking green mortgage terms and higher loan-to-value limits to energy-efficiency thresholds.

How economic events transmit into asking prices

Asking prices are set by sellers and their estate agents in response to buyer enquiry levels, sale-agreed rates, and wider economic conditions. They are a leading indicator of market sentiment, not a confirmed measure of value. The chain from economic event to changed asking price typically runs as follows:

- Economic event — a base rate change, an inflation print, a significant employment or wage-growth report.

- Mortgage market response — lenders reprice fixed-rate and tracker products, often within days of the event.

- Buyer affordability changes — the maximum loan a buyer qualifies for shifts; some buyers are priced out, others gain renewed confidence.

- Agent and seller sentiment — estate agents adjust their advice to clients on pricing strategy; some sellers lower asks, others hold or withdraw listings to wait.

- Listed asking prices adjust — typically with a lag of four to eight weeks from the original event.

This lag means asking prices on Rightmove today partly reflect sentiment from five or six weeks ago. In fast-moving conditions, buyers and sellers can be operating on materially different assumptions about where the market currently stands.

Key economic events and their typical effect on UK asking prices

Economic event | Typical short-term effect on asking prices | Typical medium-term effect |

|---|---|---|

Bank of England base rate rise | Downward pressure as affordability tightens | Prices may stabilise if employment remains strong |

Base rate cut | Upward pressure as mortgage costs fall and demand recovers | Sustained rises if cuts continue over multiple decisions |

High inflation print | Mixed; reduces real purchasing power but may delay rate cuts | Uncertainty tends to reduce transaction volumes |

Strong employment or wage growth data | Supports asking prices, particularly in high-demand regions | Gradual upward movement if sustained |

SDLT relief introduced or ending | Temporary demand spike ahead of deadline; correction typically follows | Prices adjust to reflect the underlying demand level |

Major local employer announcement | Localised movement in affected postcodes | Can be significant in single-employer or company-town areas |

New transport infrastructure confirmed | Positive uplift along the route, strongest near new stations | Long-term uplift if connectivity materially improves commuting options |

Mortgage product withdrawal or mass repricing (e.g., mini-budget 2022) | Sharp demand fall; some sellers withdraw listings entirely | Recovery tied to lender confidence and product availability returning |

What not to assume when reading property market headlines

Property market coverage regularly misleads because it conflates different measures, geographies, and property types. Understanding these common misreadings helps buyers and sellers make better decisions.

Do not assume asking prices equal sale prices. The gap between an advertised asking price and an agreed sale price varies by region and market conditions. In competitive markets, properties can sell at or above asking price; in slower markets, the average discount from asking to agreed price can be 3–6% or more.

Do not assume national indices apply to your postcode. The ONS UK House Price Index is a national average. London's market, the north of England, rural Scotland, and coastal retirement areas can move in opposite directions simultaneously. A headline stating that house prices fell nationally may mean prices rose in your local area.

Do not assume a price reduction signals desperation. In some markets, an initial high asking price followed by a reduction is a deliberate strategy that tests buyer appetite before finding the clearing level. In others, it signals genuine difficulty. Context — days on market, number of reductions, local supply and demand — matters more than the reduction alone.

Do not assume the market is static while you deliberate. Interest rates, mortgage product availability, and buyer competition can shift materially over the months a buyer or seller is active. A mortgage-in-principle obtained three months ago may no longer reflect available products or current lender criteria.

Do not treat one month's data as a trend. Seasonal patterns, Easter and school holiday effects, and reporting lags create significant noise in monthly indices. A single month of rising asking prices does not confirm a sustained recovery; a single month of falls does not confirm a crash.

Worked UK property scenario: rate cuts and sale timeline

Consider a seller in a commuter town in the East Midlands who listed a three-bedroom semi-detached in early 2024 at £285,000, based on comparable sales from three months earlier. The Bank of England base rate stood at 5.25% and mortgage rates were elevated. In the first six weeks of marketing the property received two viewings and no offers.

By late 2024, the Bank of England had begun cutting the base rate, reaching 4.75%. Mortgage product rates fell, and the estate agent reported a noticeable increase in buyer enquiry volumes across their branch. The seller, advised by their agent, held the asking price rather than reducing to generate urgency.

By early 2025, two offers arrived. The seller agreed a sale at £279,500 — below asking price, but within 2% of it, and without the reputational cost of a visible listing reduction.

The lesson is that the rate cut did not automatically produce a higher price, but it did restore transaction volume in that market. The seller's decision to hold rather than reduce proved correct — but only because they were not under time pressure and local supply remained constrained. A seller facing financial pressure might reasonably have made a different decision at the same point, accepting a faster sale at a slightly lower price. Neither outcome would be wrong; both would be rational given different circumstances.

How sellers should respond to market changes

Rather than reacting to each headline, a structured approach tends to serve sellers better:

- Monitor transaction volumes, not just price indices. High volumes signal buyer confidence; falling volumes suggest hesitation even when advertised prices hold up.

- Get a fresh agent appraisal if significant time has passed. Market conditions six months ago may be materially different from today's.

- Consider an independent valuation if you need an objective view that is not influenced by the agent's interest in winning or retaining the instruction.

- Adjust marketing strategy before adjusting price. Sometimes a change in presentation, photography, or the profile of buyer being targeted resolves the problem without a price cut.

- Know your minimum acceptable outcome before market conditions force a decision under pressure. A clear floor price agreed in advance prevents reactive decisions during negotiation.

When to get professional help

If you are pricing a property for sale and significant economic events have recently moved the market — a sudden rate change, a major local employer announcement, a planning decision that changes the character of the area — seek a professional view before committing to an asking price. An estate agent's free appraisal is commercially motivated; an independent RICS-registered valuer's written report provides a defensible, impartial figure.

If you are buying and concerned that asking prices are disconnected from underlying value, a pre-purchase RICS Home Survey will not tell you what to pay, but it will reveal condition issues that affect what the property is realistically worth to you — and that is a necessary input to any sensible negotiation.

How Housey can help

Housey connects buyers and sellers with qualified professionals across the UK, including RICS-registered valuers who provide independent valuation reports and surveyors who carry out pre-purchase home surveys. If you are making a pricing or purchasing decision in uncertain market conditions, an independent professional assessment is the most reliable input available. You can use Housey to request quotes from relevant professionals in your area.

Frequently asked questions

Which index is most reliable for UK house prices?

The ONS UK House Price Index is generally regarded as the most rigorous measure because it is based on completed mortgage transactions registered with HM Land Registry, adjusted for property mix and seasonal effects. Rightmove and Zoopla indices track asking prices, which are a useful leading indicator of sentiment but not a measure of agreed or achieved sale values.

How quickly do asking prices respond to a Bank of England rate decision?

Mortgage product repricing by lenders can happen within days of a Bank of England decision. Estate agent advice to sellers typically follows within one to two weeks. Asking prices on new listings tend to adjust over four to eight weeks. Existing listings may be slow to change if sellers are reluctant to acknowledge a shift in market conditions.

Do asking prices vary significantly between UK regions?

Yes, substantially. ONS data consistently shows that London and the South East command significantly higher prices per square metre than the North East, Wales, or Scotland. Percentage changes in any given period can diverge widely between regions, so any national figure masks a range of local conditions that may simultaneously be moving in opposite directions.

What effect does a Stamp Duty change have on asking prices?

Stamp Duty Land Tax changes alter the net cost of purchase at specific price points. When relief is introduced, demand typically rises for properties just below a new threshold, which can push asking prices upward. When relief expires, the reverse tends to occur. The effect is most pronounced in the months immediately before and after the change date.

Sources and further reading

- UK House Price Index — Office for National Statistics

- Monetary policy decisions — Bank of England

- Stamp Duty Land Tax — GOV.UK

- UK House Price Index reports — HM Land Registry / GOV.UK

- Rightmove House Price Index — Rightmove

Useful next reads

General property advice

General property adviceMonthly House Price Index: August Market Report and Analysis

The UK House Price Index is published monthly using completed Land Registry transaction data, meaning August figures typically reflect sales agreed months earlier.

General property advice

General property adviceProperty Price Movement: Record-High Asking Prices in the Current Market

UK asking prices reflect what sellers hope to achieve when listing a property, not what buyers necessarily pay.

General property advice

General property adviceUK Property Prices: Understanding Market Dynamics

UK house prices are driven by mortgage affordability, housing supply, employment levels, and policy decisions such as stamp duty changes.

General property advice

General property adviceProperty Market Trends: Activity Growth and Price Movements

UK property market activity is measured through completed sale registrations (HM Land Registry), lender mortgage data, and transaction volumes from HMRC.

General property advice

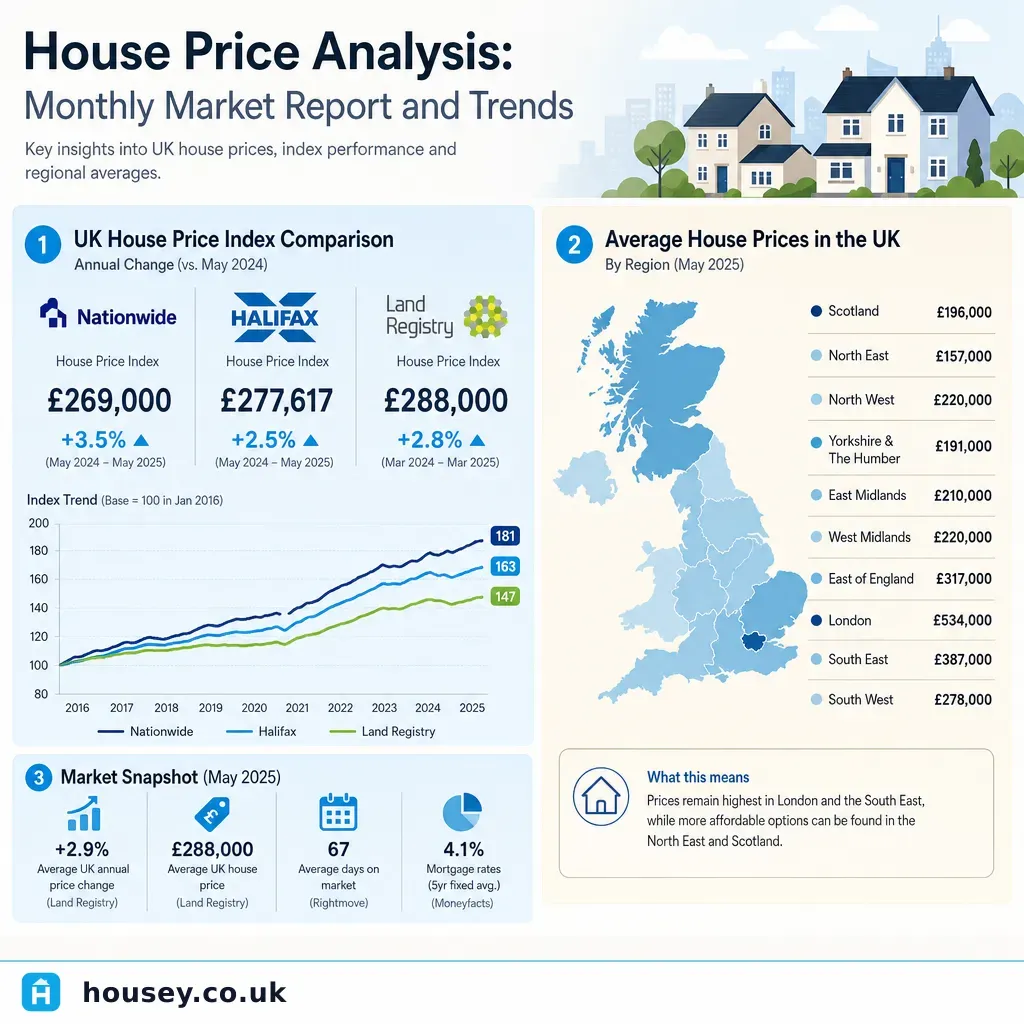

General property adviceHouse Price Analysis: Monthly Market Report and Trends

UK house prices are tracked by several major indices — the HM Land Registry UK House Price Index, the ONS House Price Index, and lender-based measures from Nationwide and Halifax.