Mortgage Redemption: Understanding Mortgage Discharge Costs and Procedures

By Housey · Last reviewed 25th of May 2026

Mortgage Redemption: Understanding Mortgage Discharge Costs and Procedures

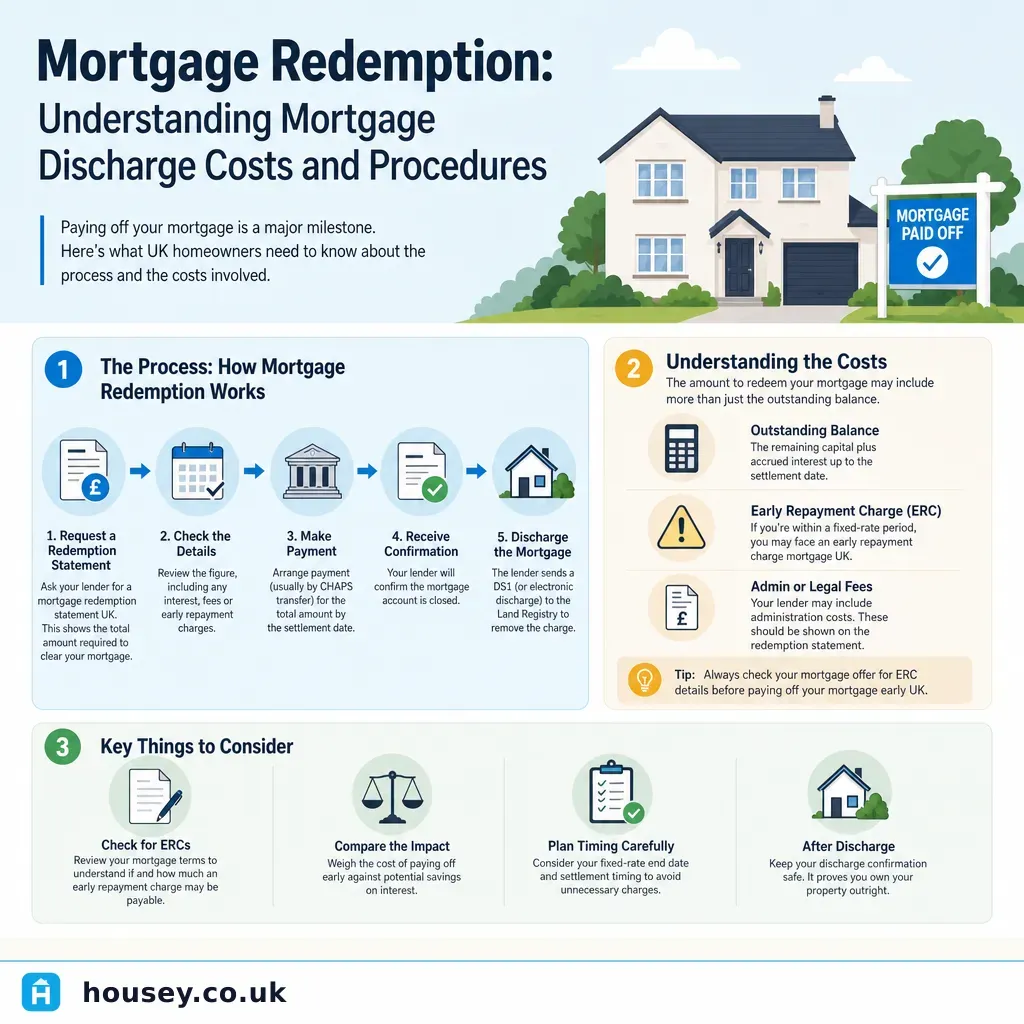

Mortgage redemption arises at the end of a mortgage term, when switching to a new lender, or when selling a property with an outstanding loan. Understanding what the total payoff figure contains — and what charges may apply — helps homeowners plan completion finances accurately and avoid last-minute shortfalls. The process also involves a formal step at HM Land Registry that must be completed before the property title is fully clear of the lender's registered charge.

Key points

- A redemption statement (also called a settlement figure) shows the exact amount needed to clear the mortgage on a specific future date, including outstanding capital, accrued interest, any early repayment charge (ERC), and any administration fees.

- ERCs typically apply during fixed-rate, tracker, or discounted deal periods and are commonly structured as 1–5% of the outstanding balance, reducing year by year through the deal period.

- After full repayment, the lender must discharge its legal charge at HM Land Registry; a DS1 or electronic e-DS1 form is required to remove the charge from the title register.

- Most lenders permit annual overpayments of up to 10% of the outstanding balance without triggering an ERC — the exact allowance is stated in your original mortgage offer documentation.

- A separate administration or mortgage exit fee of £50–£300 may apply at redemption even when no ERC is due. (Indicative UK costs, last reviewed 2026-05-25.)

What a redemption statement contains

When you decide to pay off your mortgage — whether during a sale, a remortgage, or a standalone repayment — your lender issues a redemption statement setting out:

- Outstanding capital balance

- Interest accrued from the last payment date to the proposed redemption date

- Any early repayment charge

- Administration or mortgage exit fee

- Any outstanding arrears, if applicable

Redemption statements are date-specific and typically valid for 30 days. If your sale or remortgage completes after the validity period, you will need a revised figure. Request the statement as early as possible and specify a redemption date a few days after your anticipated completion to allow for processing time.

During a property sale, your conveyancer typically requests the redemption figure directly from the lender and provides a formal undertaking to the lender's solicitors to repay the mortgage from sale proceeds on the day of completion.

Early repayment charges explained

An early repayment charge (ERC) is levied when you repay part or all of your mortgage before the end of an agreed deal period. ERCs compensate the lender for lost interest income when a borrower exits a product early. They apply to both full redemptions and overpayments that exceed your annual allowance.

Typical ERC structure by year of deal:

Year of deal | Typical ERC (% of outstanding balance) |

|---|---|

Year 1 | 4–5% |

Year 2 | 3–4% |

Year 3 | 2–3% |

Year 4 | 1–2% |

Year 5 | 0–1% |

After deal end date | 0% |

These are illustrative ranges only. Your original mortgage offer document states your exact ERC schedule. Indicative UK costs, last reviewed 2026-05-25.

Some mortgage products include a portability clause, allowing you to transfer the existing rate to a new property purchase without triggering an ERC, subject to lender criteria and the new property's valuation. Check your mortgage offer to confirm whether portability applies to your product.

How to request a redemption statement

- Contact your lender directly — most provide redemption figures online, by telephone, or through a secure messaging portal.

- Specify the exact intended redemption date, usually your anticipated sale or remortgage completion date.

- Review every line of the statement, particularly the ERC figure, and cross-reference it with your original mortgage offer document.

- Share the statement with your conveyancer, who will use it to prepare completion finances and provide a formal undertaking to the lender's solicitors.

If the figure appears higher than expected, ask your lender to itemise each component and confirm which mortgage offer clause the ERC is based on. Errors do occur and can be challenged.

What happens to the charge on your title

When a mortgage is registered, the lender registers a legal charge at HM Land Registry. This charge appears on the title register and secures the lender's interest in the property — the owner cannot sell or remortgage without first discharging it.

On full repayment the process is:

- Your conveyancer or the lender's solicitors confirm receipt of the redemption funds.

- The lender issues a DS1 form, or submits an electronic e-DS1 discharge directly to HM Land Registry.

- HM Land Registry updates the title register to remove the charge — the property is then free of the lender's registered interest.

- Your conveyancer should confirm the updated title register reflects the discharge; you can verify this yourself via the HM Land Registry title register service.

During a remortgage, your new lender's solicitors usually manage the simultaneous discharge and registration of the new charge. If you are repaying the mortgage with no concurrent transaction, you will generally need a solicitor to handle the HM Land Registry application, as the lender's DS1 alone does not automatically update the register without a formal application.

Mortgage redemption checklist

Before completing a mortgage redemption — whether as part of a sale, remortgage, or direct repayment:

What to ask your lender before redeeming

- What is the exact redemption figure valid to [your intended completion date], including all fees?

- Is an early repayment charge applicable, and which clause in my mortgage offer is it based on?

- What is my annual overpayment allowance, and have I used any portion of it in the current year?

- Is there an administration or mortgage exit fee separate from any ERC?

- Will you or your solicitors handle the HM Land Registry discharge, or should my conveyancer do this?

- What is your preferred payment method for the redemption sum?

- How long after receipt of funds will the discharge documentation be issued?

When to get professional help

For most redemptions where a conveyancer is already instructed for a sale or remortgage, no additional professional input is needed specifically for the redemption. Consider seeking specialist advice if:

- The ERC figure appears higher than expected and you want to verify the calculation against your mortgage offer.

- You are modelling whether early redemption is financially worthwhile compared with serving out the deal period.

- The property has a second charge — for example, a Help to Buy equity loan — requiring a separate redemption and discharge process.

- There is a dispute with the lender over the redemption figure or the removal of the charge from the title.

- You are redeeming a buy-to-let mortgage and need to consider potential tax implications alongside the redemption costs.

If a dispute with your lender cannot be resolved directly, the Financial Ombudsman Service can investigate complaints about mortgage redemption charges and procedures.

How Housey can help

When selling a property, coordinated conveyancing is essential to ensure the redemption statement is obtained, the lender is repaid at completion, and the title charge is formally discharged at HM Land Registry. Housey helps homeowners find and compare regulated conveyancers who manage this process from start to finish, so that nothing falls through the gaps between exchange and completion.

Frequently asked questions

What is an early repayment charge and when does it apply?

An early repayment charge (ERC) is a fee your lender charges if you repay part or all of your mortgage before the end of a fixed-rate, tracker, or discounted deal period. ERCs are expressed as a percentage of the outstanding balance — typically 1–5%, often reducing year by year through the deal. The exact schedule is set out in your original mortgage offer; always check this before making any large overpayment or redemption decision.

How do I get a mortgage redemption statement?

Contact your lender directly by phone, online account, or secure message. Specify the exact date on which you intend to redeem, as the figure includes interest accrued to that date. The statement will list outstanding capital, accrued interest, any ERC, and any administration fees. Statements are typically valid for 30 days; if completion is delayed beyond that date, request a revised figure from your lender.

What happens to the legal charge on my property when I pay off my mortgage?

Your lender's registered charge at HM Land Registry must be formally discharged after full repayment. The lender or their solicitors submit a DS1 or electronic e-DS1 discharge form, and HM Land Registry updates the title register to remove the charge. During a sale or remortgage the conveyancers handle this; for a standalone repayment, you will generally need a solicitor to manage the Land Registry application.

Can I make overpayments without triggering an early repayment charge?

Most lenders allow overpayments of up to 10% of the outstanding mortgage balance per year without triggering an ERC. This allowance is set out in your original mortgage offer and typically resets annually. Overpaying within this allowance reduces your balance and the total interest payable over the remaining term. Check your offer carefully — some products have lower allowances or different terms.

Sources and further reading

- Mortgages — consumer information — Financial Conduct Authority (FCA)

- Practice guide 31: discharge of registered charges — HM Land Registry

- Mortgages and secured loans — Citizens Advice

- Financial Ombudsman Service — mortgages — Financial Ombudsman Service

Useful next reads

General property advice

General property adviceWhat to do when your boiler stops working

When your boiler stops working, check the pressure gauge (should read 1–1.

General property advice

General property adviceProperty Market Trends: Activity Growth and Price Movements

UK property market activity is measured through completed sale registrations (HM Land Registry), lender mortgage data, and transaction volumes from HMRC.

General property advice

General property adviceInstalling a water main shut-off valve for your property

A water main shut-off valve — commonly called a stopcock — controls all water entering your home from the mains.

General property advice

General property adviceMonthly House Price Index: August Market Report and Analysis

The UK House Price Index is published monthly using completed Land Registry transaction data, meaning August figures typically reflect sales agreed months earlier.

General property advice

General property adviceScottish Property Market: Activity and Regional Trends

Scotland's property market operates under distinct legal rules: sellers must provide a Home Report before marketing, transactions become legally binding at conclusion of missives rather than exchange of contracts, and Land and Buildings Transaction Tax replaces Stamp Duty.