Mortgage Strategy: Staircasing or Accelerated Repayment Decisions

By Housey · Last reviewed 24th of May 2026

Mortgage Strategy: Staircasing or Accelerated Repayment Decisions

For shared ownership homeowners, deciding what to do with surplus income — or a lump sum from savings, inheritance, or a bonus — raises a question unique to this tenure: should you buy more of your property outright through staircasing, or use the money to overpay your mortgage? Both approaches can reduce your long-term housing costs, but they work in fundamentally different ways and carry different costs, tax implications, and cash-flow effects. The right choice depends on your lease terms, financial position, and how long you plan to stay in the property.

Key points

- Staircasing means purchasing additional equity shares in a shared ownership property from the housing association at the current RICS-assessed market value — not the original purchase price.

- Under older shared ownership leases, the minimum staircasing tranche is typically 10%; under the 2021 Affordable Homes Programme model lease, a minimum 1% tranche is available for the first 15 years of ownership.

- Each staircasing transaction requires an independent RICS valuation, solicitor fees, and may trigger a Stamp Duty Land Tax (SDLT) liability, depending on how SDLT was handled at the original purchase.

- Overpaying your mortgage reduces your outstanding loan and total interest cost but does not change your share percentage or reduce the rent you pay to the housing association on their retained share.

- Rent on the housing association's share typically increases annually — most leases index rent at RPI or CPI plus a percentage (often up to 5% per year) — meaning the rent liability grows over time regardless of mortgage overpayments.

How staircasing works

Staircasing is the formal process of purchasing additional equity shares in your shared ownership home from the housing association. When you originally bought your share — commonly between 25% and 75% of the property's market value — you began paying a subsidised rent to the housing association on the portion they retain.

To staircase, you notify your housing association, who arranges an independent RICS valuation at the current market value. The price you pay for additional shares is based on that valuation, not your original purchase price. If property values have risen since you bought, staircasing will cost more than it would have done at the outset.

Minimum tranche sizes vary by lease generation:

- Pre-2021 model leases: minimum staircasing tranche is usually 10% of the full market value.

- 2021 Affordable Homes Programme model lease: a 1% minimum tranche is available for the first 15 years, enabling smaller, more regular increments before a minimum 5% tranche applies thereafter.

Each staircasing transaction involves:

- An independent RICS valuation (indicative cost: £300–£600, varies by property and location; last reviewed 2026-05-24)

- Solicitor fees for the staircasing conveyancing (indicative cost: £500–£1,500; last reviewed 2026-05-24)

- Possible SDLT depending on your original election at purchase

- A revised mortgage if you are borrowing to fund the purchase of additional shares

Once you reach 100% ownership, rent payments to the housing association cease. You become the outright owner — typically a freeholder or a long leaseholder, depending on the scheme and property type.

How overpaying your mortgage works in shared ownership

Making overpayments means paying more than your contractual monthly mortgage amount, thereby reducing your outstanding loan balance and the total interest payable over the term.

In a shared ownership context, overpaying your mortgage:

- Reduces the loan secured against your current share of the property.

- Reduces the interest you pay over the remaining mortgage term.

- Does not increase your equity share — you still own, for example, 40% of the property.

- Does not reduce the rent you pay to the housing association on their retained share.

- Builds up equity within your existing share, which you can access on sale or remortgage.

Most residential mortgage products allow overpayments of up to 10% of the outstanding balance per year without an early repayment charge. Check your specific mortgage terms before overpaying, particularly if you are mid-way through a fixed-rate period.

Staircasing vs overpaying: a comparison

Factor | Staircasing | Overpaying mortgage |

|---|---|---|

Reduces rent you pay? | Yes — proportionally as you increase your share | No |

Increases your equity share? | Yes — formally and on the title | No — builds equity within existing share only |

Transaction costs involved? | Yes — valuation, legal fees, possible SDLT | No |

Requires a new RICS valuation? | Yes, each time | No |

Benefit if property values rise? | Share purchase becomes more expensive | Not directly affected |

Benefit if property values fall? | Shares are cheaper to buy | Not affected |

Tax implications? | Possible SDLT on each tranche | None typically |

Best suited to | Long-term residents, those concerned about rent escalation | Those with limited capital, shorter-term plans, or mid fixed-rate mortgage |

Which approach should you choose?

- Consider staircasing if you have enough capital to cover a meaningful tranche plus transaction costs, you plan to stay in the property for the long term, and you are concerned about rent escalation under your lease's annual review formula.

- Consider overpaying your mortgage if you want to reduce interest costs without incurring transaction costs, you are uncertain about staying in the property, or you are within a fixed-rate period where remortgaging would trigger early repayment charges.

- Consider a staged approach if your monthly surplus is modest — use regular overpayments to accumulate a lump sum, then staircase once you have enough to make the transaction costs proportionate.

- Check your lease before either option, particularly if it was granted before 2021, as older leases may have different minimum tranche rules, pre-emption rights, or restrictions on staircasing above a certain level.

- Consult a financial adviser if you are unsure which approach better suits your income, mortgage product, tax position, and long-term plans. Shared ownership finance involves several interacting variables.

Worked UK property scenario

Situation: Priya bought a 40% share of a two-bedroom flat in Bristol in 2021. The full market value at the time was £280,000, so her 40% share was £112,000. She took out a 25-year repayment mortgage and her outstanding balance is now approximately £98,000. She pays £380 per month in rent to the housing association on their 60% share (£168,000). Her lease indexes rent at RPI plus 0.5% annually.

Option A — Staircase by 10% The property is independently valued at £310,000 in 2026. A 10% tranche costs £31,000. Solicitor and RICS valuation fees add approximately £1,800. Total outlay: around £32,800. After staircasing from 40% to 50%, Priya's rent reduces proportionally — she now pays rent on a 50% share (£155,000) rather than 60%, reducing her monthly rent from approximately £380 to £317. Annual saving: approximately £756. If rent increases at 3% annually, the cumulative saving over 10 years would be substantial — and growing.

Option B — Overpay mortgage by £5,000 Priya makes a £5,000 lump-sum overpayment. Her outstanding balance falls to approximately £93,000. At her current mortgage rate, this saves roughly £200–£250 per year in interest over the remaining term. Her rent stays at £380 per month and continues to rise annually. No transaction costs.

Comparison: Staircasing has a much higher upfront cost but delivers a permanent, compounding reduction in rent. Overpaying is more accessible and avoids transaction costs, but does not address the escalating rent liability. For Priya, who plans to stay in the flat for at least 10 years, the staircasing option is likely to generate greater total savings over the long term — but only if she can afford the upfront outlay without stretching her finances.

This is a simplified illustrative example using indicative figures. Actual costs, valuations, and savings will vary. Indicative UK costs, last reviewed 2026-05-24. Always seek advice from a qualified financial adviser and your housing association before proceeding.

Important limitations

This article provides general background on shared ownership staircasing and mortgage overpayments in England. It is not financial or legal advice. The right strategy depends on your specific lease terms, mortgage product, housing association rules, SDLT position, and personal financial circumstances. Rules around Stamp Duty Land Tax on shared ownership transactions are complex and subject to change. The worked scenario uses simplified assumptions and should not be treated as a financial projection. Always seek advice from a qualified financial adviser and a solicitor familiar with shared ownership before making any staircasing decision.

What to ask a qualified professional

- What is the minimum staircasing tranche permitted under my specific lease, and does the 2021 model lease apply?

- What will a RICS valuation cost for my property, and how long is the valuation valid for purposes of the transaction?

- Are there any early repayment charges on my current mortgage if I need to remortgage to fund a staircasing purchase?

- What is the rent review formula in my lease, and by how much could my rent increase over 10 and 20 years?

- Would this staircasing transaction trigger a Stamp Duty Land Tax liability, and if so, at what amount?

- What are the total transaction costs of a staircasing exercise including legal fees, valuation, and any remortgage arrangement fee?

- How much of my outstanding mortgage can I overpay each year without incurring an early repayment charge?

When to get professional help

Consult a qualified financial adviser who is familiar with shared ownership before making any significant decision about staircasing or mortgage strategy. Seek professional advice in particular if:

- You are considering staircasing to 100% ownership, which substantially changes your financial and legal position and may require a new mortgage product.

- Your lease was granted before 2021 and you are uncertain about your specific rights, minimum tranche sizes, or any pre-emption obligations.

- Your mortgage is approaching the end of a fixed-rate period and you need to consider remortgaging at the same time as planning a staircasing transaction.

- You are unsure whether a staircasing transaction would trigger a Stamp Duty Land Tax liability under your original SDLT election.

How Housey can help

Housey covers a wide range of property guidance for homeowners at every stage of ownership. If your shared ownership question touches on conveyancing, valuations, or planning your next move, browse our property advice guides for clear, practical information to help you make better decisions.

Frequently asked questions

Can I staircase to 100% on any shared ownership property?

Most shared ownership leases allow staircasing to 100% full ownership, at which point rent payments to the housing association cease. However, some properties — particularly those on National Park land, rural exception sites, or certain designated areas — have lease restrictions preventing staircasing above a set threshold. Always check your specific lease and confirm with your housing association before planning a staircasing programme.

Do I need a new mortgage to staircase?

Not if you are funding the additional share from savings. If you need to borrow to fund the purchase, you will typically need to extend your existing mortgage or remortgage to a new product. If you are mid-term on a fixed rate, early repayment charges may apply. A mortgage broker familiar with shared ownership can advise on the most cost-effective approach given your current product.

Does overpaying my mortgage increase my share in the property?

No. Overpaying your mortgage reduces the outstanding loan on your existing share but does not change the equity split between you and the housing association. Only a formal staircasing transaction — purchasing additional shares at a RICS-assessed market value — changes the ownership percentages recorded in your lease and at HM Land Registry.

Is there Stamp Duty Land Tax on staircasing?

The SDLT position for shared ownership staircasing is complex. At initial purchase, you can elect to pay SDLT on the full market value upfront, after which no further SDLT arises on subsequent staircasing. If you did not make that election, SDLT may become payable when cumulative ownership reaches certain statutory thresholds. Always seek advice from a solicitor or tax professional before any staircasing transaction.

Sources and further reading

- GOV.UK: Shared ownership homes — buying more shares (staircasing) — GOV.UK

- GOV.UK: Stamp Duty Land Tax for shared ownership properties — GOV.UK

- Homes England: Shared Ownership model lease 2021 — Homes England / GOV.UK

- MoneyHelper: Should I overpay my mortgage? — MoneyHelper (Money and Pensions Service)

Useful next reads

General property advice

General property adviceMortgage Advice After Rate Changes: Financial Planning for Homeowners

When mortgage rates change, homeowners on tracker or standard variable rate mortgages feel the impact immediately, while those on a fixed deal are protected until the term ends.

General property advice

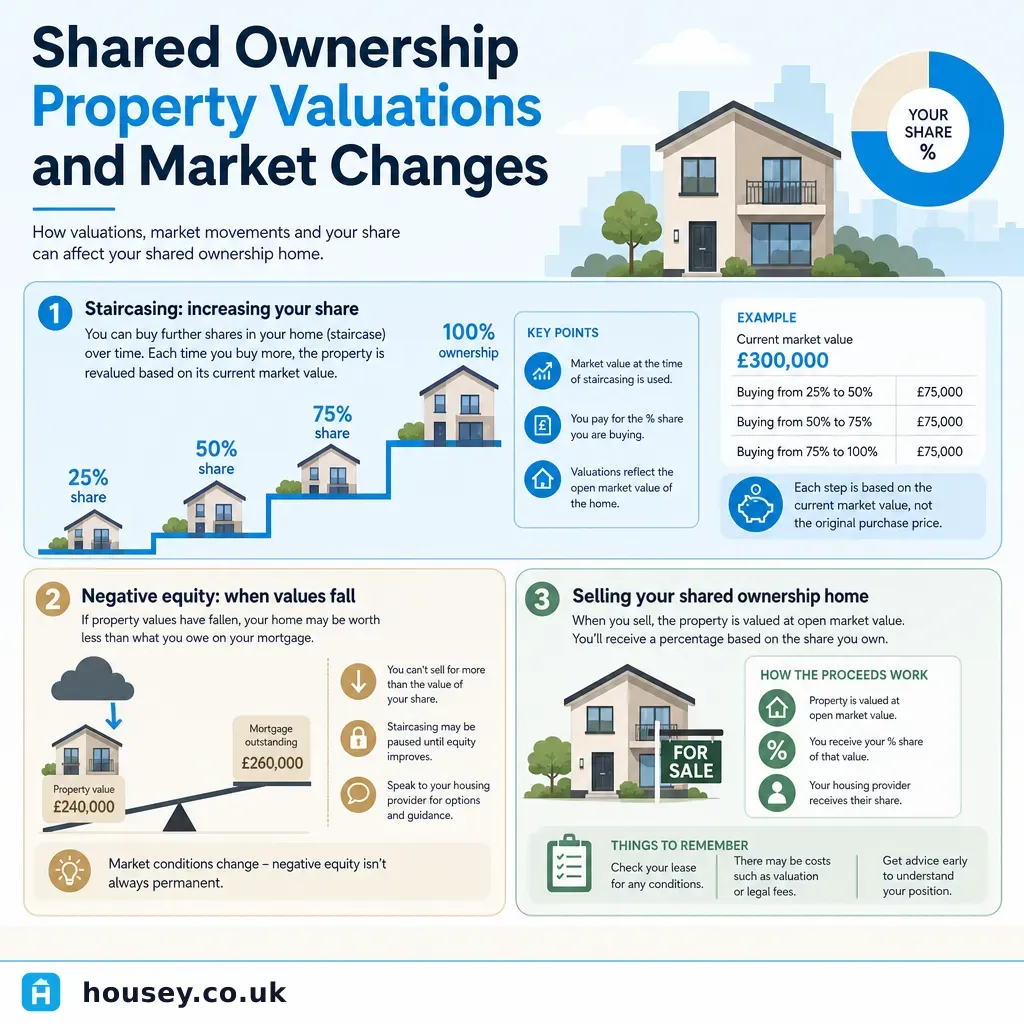

General property adviceShared Ownership Property Valuations and Market Changes

Shared ownership valuations are carried out by RICS-registered valuers to establish the open market value of the whole property; your share price is your ownership percentage of that figure.

General property advice

General property adviceWhat to do when your boiler stops working

When your boiler stops working, check the pressure gauge (should read 1–1.

General property advice

General property adviceProperty Market Trends: Activity Growth and Price Movements

UK property market activity is measured through completed sale registrations (HM Land Registry), lender mortgage data, and transaction volumes from HMRC.

General property advice

General property adviceInstalling a water main shut-off valve for your property

A water main shut-off valve — commonly called a stopcock — controls all water entering your home from the mains.