Shared Ownership Property Valuations and Market Changes

By Housey · Last reviewed 24th of May 2026

Shared Ownership Property Valuations and Market Changes

Shared ownership sits at an unusual intersection of homeownership and renting — and valuations play a central role in every significant financial decision a shared owner faces. Whether you are considering buying additional shares (staircasing), preparing to sell, approaching a remortgage, or simply trying to understand how a shifting market affects your position, the mechanics of shared ownership valuations work differently from standard homeownership in ways that matter considerably.

Key points

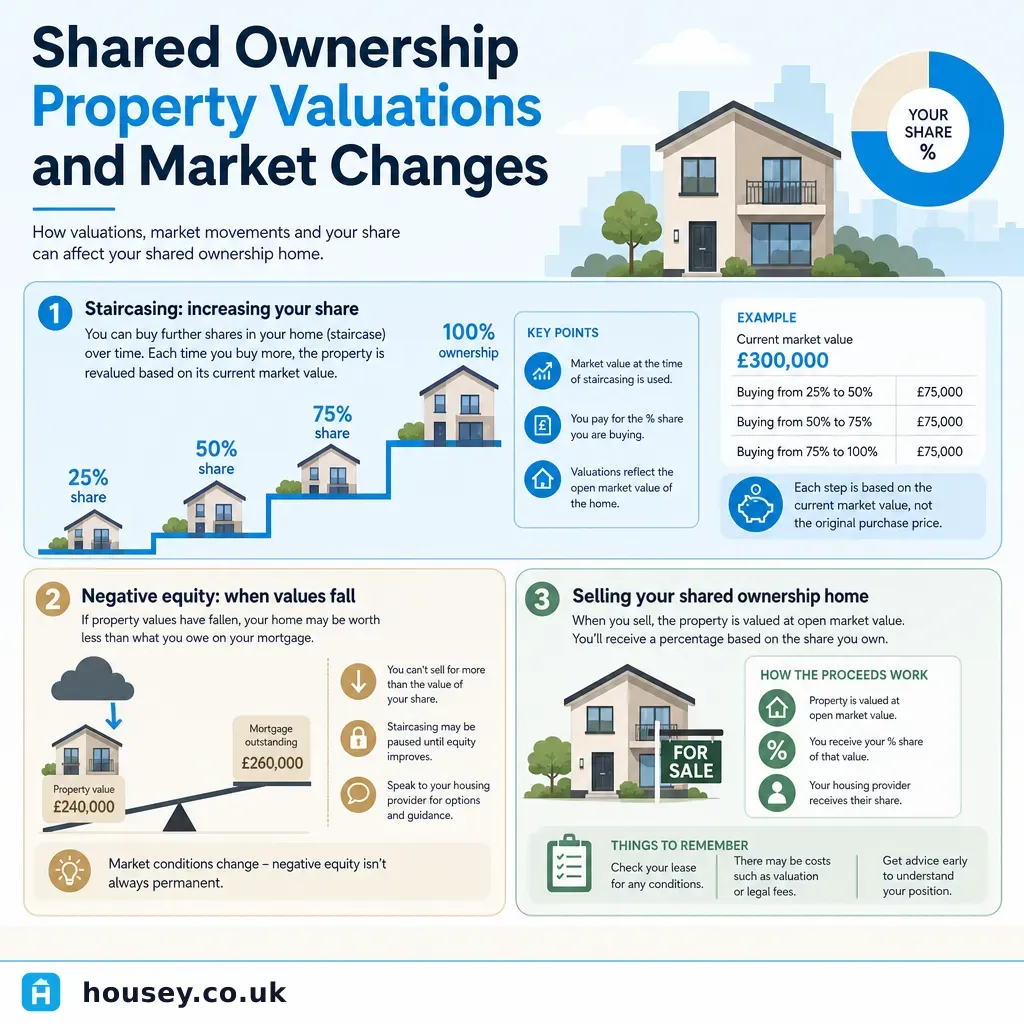

- A RICS-registered valuer must carry out any shared ownership valuation used for staircasing, selling, or remortgaging; valuations are typically valid for three months, though your housing association's lease may specify a different window.

- Under the pre-April 2021 model, the minimum initial share is usually 25%; under the new model (homes funded from April 2021), the minimum initial share falls to 10%.

- When you staircase, the price of additional shares is calculated from the open market value at the time of the new RICS valuation — not from your original purchase price.

- A market fall reduces the value of your share proportionally; if your outstanding mortgage on that share exceeds its current value, you are in negative equity.

- Rent on the housing association's share is typically linked to RPI or CPI, not to property market values — it can rise even when your property value falls.

How shared ownership valuations work

Shared ownership valuations follow RICS Red Book Global Standards. The RICS-registered valuer assesses the open market value of the whole property as if it were being sold freehold on the open market. Your share price is then calculated as your ownership percentage of that figure.

Valuations are required in these typical situations:

- Staircasing — buying additional shares from your housing association

- Selling your share — the housing association usually has a nomination period (typically eight weeks) to find a buyer from its waiting list at the valuation price

- Remortgaging — mortgage lenders require an independent RICS valuation

- Subletting — where the lease permits it

Costs for a shared ownership RICS valuation typically range from £250 to £500 (indicative UK costs, last reviewed 2026-05-24; costs vary by region, property type, and which valuer is instructed).

Your lease will specify who instructs the valuer and who pays. For staircasing, some housing associations instruct the valuer and you reimburse them; others allow you to instruct a valuer from an approved panel.

How property market changes affect your position

Rising market

A rising market increases the value of your share and builds equity — but it also increases the cost of buying more shares. If you want to staircase from 25% to 50%, the cost of that additional 25% is based on the higher current market value at the point of the new RICS valuation, not your original purchase price.

Falling market

A market fall reduces your share's value proportionally. Two key risks follow:

- Negative equity — if your outstanding mortgage exceeds the current value of your share, you cannot easily sell or remortgage without covering the shortfall.

- Tighter lending conditions — while additional shares cost less in absolute terms during a downturn, lenders may apply stricter criteria for staircasing mortgages.

What not to assume

Common assumption | Reality |

|---|---|

Rent stays the same if property prices fall | Rent on the housing association's share is typically linked to RPI or CPI — it can rise even when property values fall |

I can sell my share whenever I choose | The housing association has a nomination period (typically eight weeks) to find a buyer; the resale process takes time |

Staircasing to 100% removes all restrictions | Some leases — particularly on rural exception sites or certain London affordable housing schemes — prevent full staircasing to 100% |

My share value mirrors the market exactly | The RICS valuation also reflects the specific property's condition, lease length, and local demand factors |

Selling your shared ownership home

When you sell, the process differs from a standard open-market sale:

- Request a RICS valuation per your lease terms.

- Notify your housing association — they typically have eight weeks to nominate a buyer from their waiting list at the valuation price.

- If no buyer is found within the nomination period, you may be able to market on the open market through an agreed estate agent; your lease will specify the precise terms.

- The buyer purchases your share, or may staircase to 100% simultaneously.

A solicitor with shared ownership experience is essential here. Lease terms vary significantly between housing associations and between older and newer funding models.

The post-April 2021 shared ownership model

The government's new model of shared ownership applies to homes funded from April 2021:

- Minimum initial share reduced from 25% to 10%

- Minimum staircasing tranche reduced to 1% in certain circumstances (check your specific lease)

- Housing association responsible for repairs for the first 10 years on qualifying new-build properties under the new model

- Rent increases capped at RPI + 0.5% under the new model

Older leases operate under different terms. Check your specific lease with a solicitor before assuming any new-model rules apply to your home.

Important limitations

This article provides general information only. Shared ownership lease terms, housing association policies, RICS valuation processes, and market conditions vary considerably. Rules differ between England, Wales, Scotland, and Northern Ireland. Nothing in this article constitutes legal, financial, or surveying advice. Always consult a RICS-registered valuer, a solicitor with shared ownership experience, and an independent financial adviser before making any staircasing, selling, or remortgage decision.

When this becomes urgent

Seek professional advice promptly if:

- Your property value may have fallen below your outstanding mortgage balance on your share

- Your housing association has issued a notice or deadline relating to your lease

- You are struggling to meet both rent and mortgage payments simultaneously

- You want to sublet (many shared ownership leases prohibit or tightly restrict this)

- You are approaching the end of a fixed-rate mortgage term and want to understand your remortgage options

What to ask a qualified professional

RICS-registered valuer:

- Are you experienced with shared ownership valuations in this area and postcode?

- How long will the valuation remain valid for my housing association's staircasing process?

- What access and documents will you need before the inspection?

Solicitor (shared ownership experience essential):

- What are the resale provisions and nomination period in my specific lease?

- Can I staircase to 100% under the terms of my lease?

- What total costs should I budget for — legal fees, SDLT or LBTT, valuation fee, housing association administration charge?

Independent financial adviser:

- What mortgage options are available to me for staircasing at my current loan-to-value ratio?

- How would a market fall affect my ability to remortgage?

When to get professional help

Shared ownership is a complex tenure and market changes affect it differently from standard homeownership. Seek professional help if you are planning to staircase or sell, suspect you may be in negative equity, have received communications from your housing association about lease obligations, or are approaching the end of a fixed-rate mortgage term.

How Housey can help

Housey connects homeowners — including shared owners — with qualified surveyors and solicitors. Whether you need a RICS-registered valuation for staircasing or legal advice from a solicitor with shared ownership conveyancing experience, Housey can help you find the right professional for your situation.

Frequently asked questions

Do I need a new RICS valuation every time I staircase?

Yes. Each time you purchase additional shares, a fresh RICS-registered valuation is required to establish the current open market value. The price you pay is based on this new valuation, not your original purchase price. Most housing associations specify approved valuers or a defined process for instructing one; check your lease for the exact requirements.

What happens if property values have fallen and I want to sell my shared ownership home?

If the market has fallen, your RICS valuation will reflect the lower value. If that figure is below your outstanding mortgage on your share, you are in negative equity and may not be able to sell without making up the shortfall. Contact your mortgage lender and a solicitor experienced in shared ownership conveyancing to understand your options before acting.

Can my housing association refuse my request to staircase?

Generally, your lease grants you the right to staircase and the housing association cannot refuse without a valid lease-based reason. However, some leases — particularly on rural exception sites or certain affordable housing schemes — restrict staircasing to 100%. Always check your specific lease terms with a solicitor before assuming the right to staircase is unrestricted.

Is Stamp Duty Land Tax payable when I staircase?

SDLT applies in England; LBTT applies in Scotland. Both have specific shared ownership rules. In England, on your initial purchase you can elect to pay SDLT on the full market value (paying nothing on future tranches) or pay in stages as you staircase. Rules are complex and depend on your circumstances; always take professional advice and check current GOV.UK guidance.

Sources and further reading

- Shared ownership: buying more shares (staircasing) — GOV.UK

- Shared ownership scheme — GOV.UK

- RICS Red Book Global Standards — RICS

- SDLT: shared ownership property — GOV.UK

- New model shared ownership — Homes England / GOV.UK

Useful next reads

General property advice

General property adviceMortgage Strategy: Staircasing or Accelerated Repayment Decisions

Staircasing means buying additional equity shares in your shared ownership home from the housing association, based on a current RICS valuation.

General property advice

General property adviceWhat to do when your boiler stops working

When your boiler stops working, check the pressure gauge (should read 1–1.

General property advice

General property adviceProperty Market Trends: Activity Growth and Price Movements

UK property market activity is measured through completed sale registrations (HM Land Registry), lender mortgage data, and transaction volumes from HMRC.

General property advice

General property adviceInstalling a water main shut-off valve for your property

A water main shut-off valve — commonly called a stopcock — controls all water entering your home from the mains.

General property advice

General property adviceMonthly House Price Index: August Market Report and Analysis

The UK House Price Index is published monthly using completed Land Registry transaction data, meaning August figures typically reflect sales agreed months earlier.