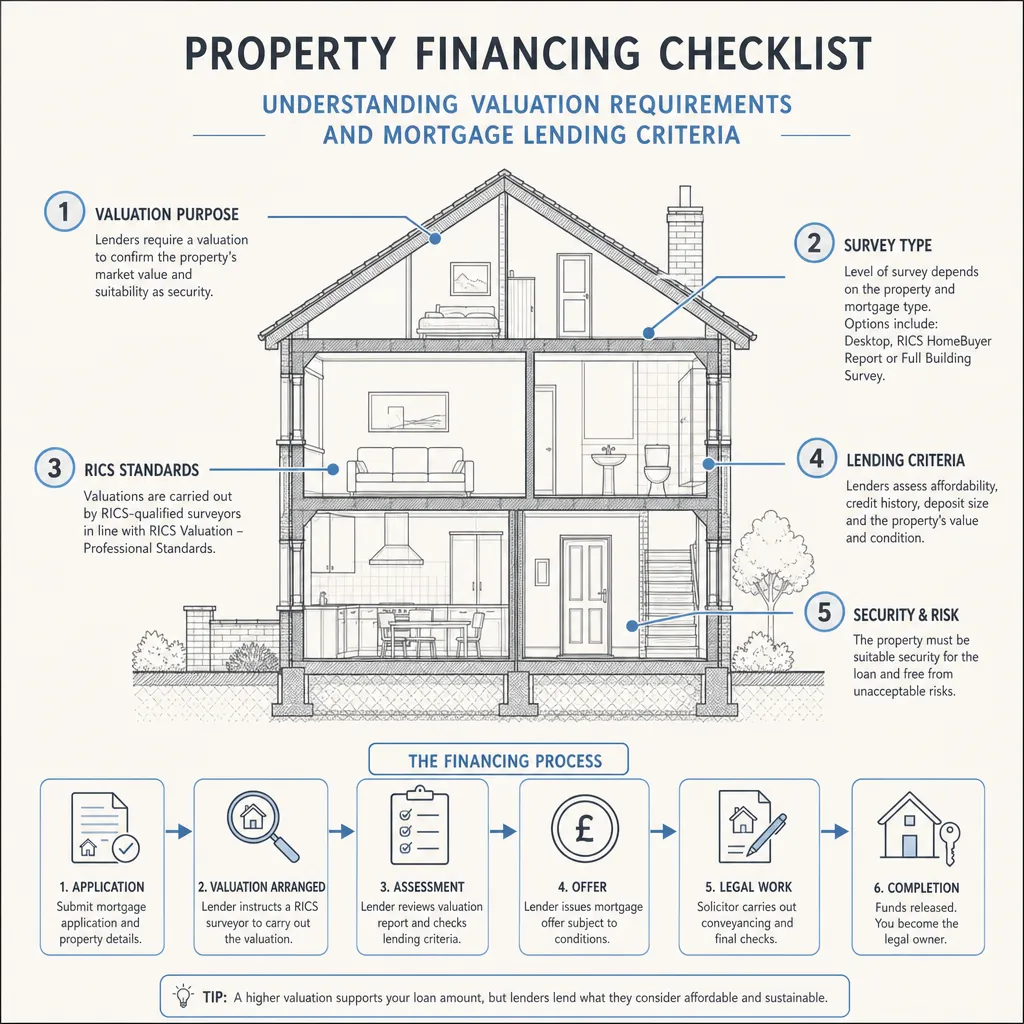

Property financing checklist: understanding valuation requirements and mortgage lending criteria

By Housey · Last reviewed 7th of May 2026

Property financing checklist: understanding valuation requirements and mortgage lending criteria

Mortgage lenders have a direct financial interest in the property you are buying, which means they impose their own valuation and inspection requirements before releasing funds. Understanding what lenders look for — and how surveys fit into that picture — helps buyers avoid delays, down-valuations, and the unexpected discovery that a lender will not advance on a particular property at all. This matters most when buying older, non-standard, or visibly imperfect properties where lending criteria can diverge sharply from buyer expectations.

Key points

- Mortgage lenders commission their own mortgage valuation for the lender's benefit — it does not replace a RICS Home Survey and creates no duty of care to the buyer.

- A mortgage valuation typically costs £150–£1,500 depending on property value and lender; some lenders include a free valuation as a product incentive (Indicative UK costs, last reviewed 2026-05-07).

- Lenders can decline to lend, reduce the loan amount (a down-valuation), or attach mortgage conditions requiring specific works before funds are released.

- Properties with non-standard construction — steel frame, prefabricated reinforced concrete (PRC), Mundic block, or thatched roofs — may face restricted mainstream lending and higher deposit requirements.

- EPC ratings and PAS 2035 retrofit assessments can influence mortgage product eligibility, particularly for green mortgage products from lenders such as Barclays, NatWest, and specialist providers.

What is a mortgage valuation and what does it cover?

A mortgage valuation is a brief inspection carried out by a surveyor appointed by the lender. Its sole purpose is to confirm the property is adequate security for the loan amount. The valuer typically spends 15–30 minutes on site and produces a short report confirming the estimated market value and noting any obvious concerns that might affect lendability.

What a mortgage valuation does NOT cover:

- Detailed assessment of the building fabric, drains, or roof structure

- Identification of damp, timber decay, or structural movement beyond obvious visual signs

- Any advice to you as the buyer on condition or repair costs

A mortgage valuation is not a survey. Buyers who rely on it alone risk missing serious defects that only emerge after legal completion.

How lenders assess property suitability

Lenders use a combination of the valuation report and their own internal criteria to decide whether to lend, and on what terms.

Factor | What lenders typically check | Why it matters |

|---|---|---|

Market value vs purchase price | Surveyor's estimated value vs agreed sale price | Down-valuation reduces the maximum loan amount |

Construction type | Standard (brick/block/slate/tile) vs non-standard | Some non-standard types restrict the choice of lender |

Habitable condition | Property must be immediately habitable | Properties needing major structural work may require specialist finance |

Lease length (leasehold) | Usually ≥70–85 years remaining (lender-specific) | Short leases reduce the property's security value |

EPC rating | Some green mortgage products require EPC Band C or above | Poor EPC ratings may exclude best-rate products |

Flood risk | Environment Agency flood zone classification | High flood risk can trigger specialist insurance requirements or a declined application |

Subsidence history | Previous insurance claims or ground movement records | May trigger further structural investigation before lending proceeds |

Non-standard construction

Properties built with steel frame, in-situ concrete, prefabricated reinforced concrete (PRC), Mundic block (found in parts of Cornwall and Devon), or those with thatched roofs may face fewer lenders willing to offer mortgages, higher deposit requirements (often 25% or more), or a requirement for a specialist structural survey before approval. Check lender eligibility before instructing solicitors if you are buying non-standard construction.

Mortgage conditions: what they are and how to deal with them

Mortgage conditions — sometimes called a "mortgage retention" or "lender conditions" — are requirements the lender attaches to the offer. Until satisfied, part or all of the funds may be withheld.

Common conditions include:

- Evidence that a specific repair has been completed before completion (e.g., roof work, electrical remediation)

- A retention of funds (typically £1,000–£5,000) held back until works are done post-completion

- A requirement to obtain a full structural survey or specialist report before funds are released

- Proof of adequate buildings insurance from the day of completion

What to do if your lender attaches conditions:

- Get the condition in writing and understand exactly what work is required and by when.

- Instruct relevant specialists — structural engineer, roofer, or electrician — to quote promptly.

- Check whether the condition must be satisfied pre- or post-completion, as this affects timing and negotiation with the seller.

- Consider re-negotiating the purchase price to reflect required works.

- Speak to a mortgage broker if the condition is severe enough to threaten the application.

Buyer checklist: preparing for the valuation and lending process

Before instructing a mortgage:

When the mortgage valuation is booked:

After the mortgage valuation:

Before exchange:

What not to assume

Many buyers make the same mistakes when it comes to valuations and lending. Here are the most common misunderstandings:

"The mortgage valuation confirmed the property is in good condition." It did not. The mortgage valuation confirms the lender considers the property adequate security at the loan amount. The surveyor is not assessing the property on your behalf and has no duty of care to you as the buyer.

"Because the lender valued it at the purchase price, I don't need a survey." A valuation at purchase price means the lender is willing to lend — nothing more. It says nothing about the condition of the roof, drains, electrics, damp levels, or structural integrity. A RICS Level 2 survey is always worth commissioning independently.

"All lenders use the same valuation criteria." They do not. Criteria vary significantly between lenders, particularly for non-standard construction, short leases, properties with recent flood history, and EPC ratings. A mortgage broker can identify lenders whose criteria suit the specific property.

"A down-valuation means I must renegotiate or walk away." Not necessarily. You can challenge a down-valuation by providing recent comparable sales evidence to the lender or their appointed surveyor. A mortgage broker can assist with this process.

"A survey is optional if the property looks fine at viewing." Viewings are brief and cannot reveal problems inside roof voids, below floors, within drainage runs, or behind walls. A valuation survey protects the lender; only an independent RICS survey protects you.

Important limitations

This article provides general information about mortgage valuation and lending criteria in England and Wales. Criteria vary between lenders, mortgage products, property types, and individual circumstances. Nothing here constitutes mortgage advice, legal advice, or a valuation. Rules in Scotland — where Home Reports are required before a property is marketed — and in Northern Ireland differ from those in England and Wales. Always verify current requirements with your lender or an FCA-authorised mortgage broker before proceeding.

What to ask a qualified professional

Before instructing a surveyor or mortgage broker:

- To your lender or broker: What construction types does this lender accept? Is there a minimum lease length? What EPC band is required for this mortgage product?

- To a RICS surveyor: What level of survey do you recommend for this property's age and type? What are the most likely areas of concern given the construction and location?

- To your solicitor: Are there any entries on the title or Land Registry records suggesting previous structural, subsidence, or flooding issues?

- If a condition is attached: What specific evidence does the lender require, and by what date must it be provided?

When to get professional help

Seek independent professional advice promptly if:

- The lender has attached a condition requiring structural investigation or specific repairs before funds are released

- The property has been down-valued by more than 5% of the agreed purchase price

- You are buying non-standard construction and are uncertain which lenders will accept it

- The property is in Flood Zone 2 or 3 (England) and you have not checked insurance implications

- Visible signs of movement, cracking, or damp have been noted in the mortgage valuation report

How Housey can help

If you need an independent survey alongside your lender's mortgage valuation, Housey can help you request quotes from RICS-qualified surveyors. Explore RICS Home Surveys for a comprehensive independent assessment, choose a RICS Level 2 survey for conventional properties in reasonable condition, or commission structural surveys where concerns have already been flagged. For lender-required assessments, see valuation surveys.

Frequently asked questions

Is the mortgage valuation the same as a survey?

No. A mortgage valuation is a brief inspection for the lender's benefit, confirming the property is adequate security for the loan. It is not an assessment of condition and does not protect the buyer. A RICS Home Survey (Level 2 or Level 3) is a separate, independent inspection carried out on your behalf.

What happens if the property is valued below the purchase price?

If the lender's valuation comes in below the agreed purchase price, the lender will only advance a loan based on the lower figure. You will need to make up the shortfall in cash, renegotiate the price with the seller, or challenge the valuation with recent comparable sales evidence. A mortgage broker can assist.

Can a lender refuse to lend on a property because of its condition?

Yes. Lenders can decline to lend on properties that are not immediately habitable, have serious structural concerns, or are of a construction type outside their acceptable criteria. Specialist lenders or bridging finance may be options in some cases — speak to an FCA-authorised mortgage broker for guidance.

What is a mortgage retention?

A mortgage retention is where the lender withholds a portion of the loan amount until specified works are completed. For example, the lender may retain £3,000 until a roof repair is evidenced by a contractor's invoice and inspection sign-off. The retained amount and conditions should be set out clearly in the mortgage offer document.

Do I need a survey if the property is newly built?

New-build properties come with an NHBC Buildmark warranty or equivalent, but can still have defects. A RICS snagging survey or new-build inspection is advisable before or shortly after legal completion, even if the lender's mortgage valuation raised no concerns.

Sources and further reading

- GOV.UK EPC Register — GOV.UK

- Money Helper — Mortgage valuations explained — MoneyHelper (MaPS)

- Environment Agency Flood Map for Planning — Environment Agency

- Citizens Advice — Buying a home — Citizens Advice

- RICS — Find a RICS-regulated firm — RICS

Useful next reads

Surveys & Inspections

Surveys & InspectionsProperty valuation factors: how mortgages and lending conditions influence market confidence

Mortgage lenders base their offer on the lower of the agreed purchase price or the surveyor's valuation.

Surveys & Inspections

Surveys & InspectionsWhy Property Boundaries Matter: Surveying and Dispute Prevention

Property boundaries in England and Wales are recorded as general boundaries by HM Land Registry — not precise measurements.

Surveys & Inspections

Surveys & InspectionsGetting a Valuation Survey Before Selling Your Property

Before selling, a free estate agent appraisal gives a market price guide, but only a RICS Red Book valuation carries formal professional standards and legal weight.

Surveys & Inspections

Surveys & InspectionsProperty Valuation Survey: Understanding Market Worth and Cost Assessment

A property valuation survey establishes a property's market value at a specific date.

Surveys & Inspections

Surveys & InspectionsProperty Valuation Factors: Elements Affecting Home Assessment

UK property valuations are primarily driven by location and comparable sales evidence, followed by floor area, condition, EPC rating, and legal factors such as lease length.