Property valuation factors: how mortgages and lending conditions influence market confidence

By Housey · Last reviewed 7th of May 2026

Property valuation factors: how mortgages and lending conditions influence market confidence

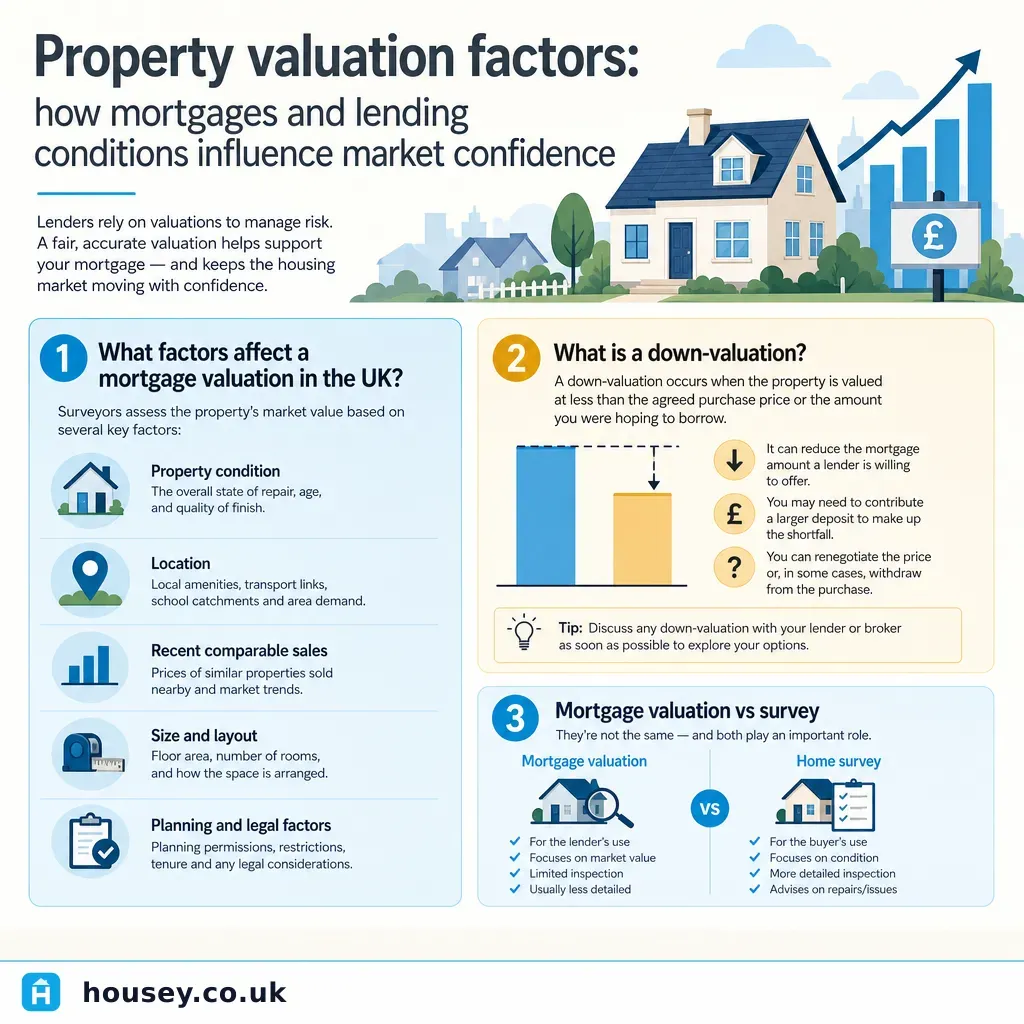

Mortgage lending conditions sit at the centre of the UK property market. When a buyer applies for a mortgage, the lender instructs a valuation of the property — and the outcome of that valuation can determine how much can be borrowed, whether the sale proceeds, and what price the seller ultimately accepts. For homeowners tracking the market, understanding how lending criteria, interest rates, and lender caution translate into property values helps explain why prices can stall or fall even when estate agents report strong enquiry levels.

Key points

- Lenders use the lower of the agreed purchase price or the surveyor's valuation when calculating how much to lend; any gap between the two is called a down-valuation.

- The RICS Valuation – Global Standards (Red Book) sets the methodology that RICS-registered valuers must follow when producing mortgage valuations in the UK.

- Loan-to-value (LTV) ratios directly affect the interest rate a borrower pays and the maximum loan available; a 90% LTV mortgage typically carries a higher rate than a 60% LTV product.

- Under the Minimum Energy Efficiency Standards (MEES), privately rented properties in England and Wales must hold an EPC rating of at least E to be legally let; some lenders apply stricter criteria for buy-to-let applications.

- A standard mortgage valuation is not a buyer's survey — it may involve a short physical inspection or a desktop assessment, and it protects the lender's security interest, not the buyer's.

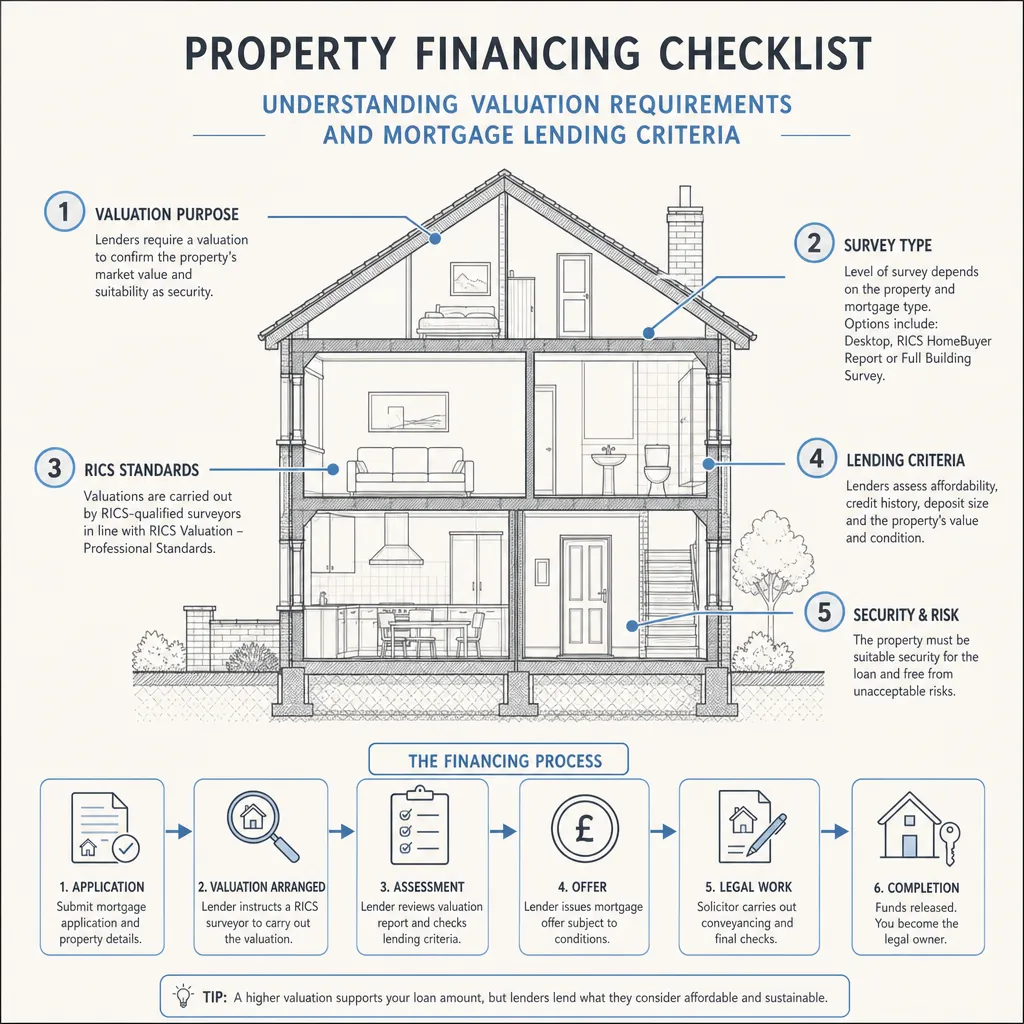

What a mortgage valuation actually assesses

A mortgage valuation answers one question for the lender: is the property worth at least the sum being borrowed against it? The RICS valuer considers recent comparable sales in the local area, the property's physical condition, its tenure (freehold or leasehold), and any characteristics that might make the property difficult to resell — such as non-standard construction, a short lease, cladding concerns, or significant structural defects.

The valuer does not produce a detailed schedule of defects, estimate repair costs, or advise the buyer on whether to proceed. For that kind of buyer-facing analysis, a separate RICS Home Survey or specialist inspection is needed.

Property factors that commonly affect a mortgage valuation

Property characteristic | Likely effect on mortgage valuation or lending decision |

|---|---|

Non-standard construction (timber frame, prefab, steel frame) | May reduce or limit the lender's offer; some lenders decline these property types entirely |

Lease below 70–85 years remaining | Many lenders require a minimum remaining term; very short leases can make a property unmortgageable |

Significant structural movement or severe damp | Valuer may note concerns; lender may impose a retention until remedial work is completed |

EPC rating F or G on a buy-to-let property | May be unlettable under MEES and therefore unacceptable as lender security |

Unresolved cladding or fire-safety issues on high-rise flats | May be unmortgageable without a valid EWS1 form confirming external wall safety |

Above-garage or deck-access flats | Some lenders decline; others apply a lower maximum LTV |

How lending conditions shape market confidence

When the Bank of England raises the base rate, mortgage rates typically follow. Higher borrowing costs reduce the maximum loan a buyer can service at a given monthly payment, which directly compresses purchasing power across the buyer pool. In practical terms:

- A buyer qualifying for a £300,000 mortgage at 2% interest may qualify for considerably less at 5% on the same income and repayment period.

- If purchasing power falls across the buyer pool, sellers face pressure to reduce asking prices or accept longer marketing periods.

- Lenders periodically tighten LTV thresholds during periods of economic uncertainty, withdrawing 85–95% LTV products and effectively restricting buyers with smaller deposits.

This is why mortgage approval volumes — published monthly by the Bank of England — are closely watched by market analysts. When approvals fall, reduced buyer competition tends to dampen comparable sales evidence, which feeds into more cautious valuations over subsequent months.

Mortgage valuation vs RICS Home Survey: a comparison

A persistent source of confusion for buyers is the assumption that the lender's valuation confirms the property is structurally sound or in good condition. It does not. The table below sets out the key differences.

| Mortgage valuation | RICS Level 2 Home Survey | RICS Level 3 Building Survey |

|---|---|---|---|

Who commissions it | Lender | Buyer | Buyer |

Who it protects | Lender | Buyer | Buyer |

Primary purpose | Confirms value adequate for lending | Condition ratings and material information | Full inspection with detailed defect analysis |

Defects recorded | Only those materially affecting value | Yes, with traffic-light condition ratings | Yes, in detail including cost implications |

Typical report length | 1–4 pages or desktop summary | 15–30 pages | 40–80+ pages |

Indicative fee range | Often bundled with mortgage product | £400–£900 | £600–£1,500+ |

Best suited to | Lender's security purposes only | Conventional properties in reasonable condition | Older, larger, unusual, altered, or defective properties |

Indicative UK costs, last reviewed 2026-05-07. Fees vary significantly by region, property size, and surveyor.

If defects or structural concerns arise from a RICS Home Survey, a structural survey from a chartered structural engineer may be advisable before exchange.

What causes a down-valuation?

A down-valuation occurs when the RICS valuer concludes the property is worth less than the agreed purchase price. Common triggers include:

- Optimistic pricing in a cooling market, where recent comparable sales do not support the agreed figure.

- Significant defects noted during inspection that reduce the property's value relative to comparable, undamaged properties.

- Rapidly softening market conditions, where sales evidence has weakened since the offer was agreed.

- Unusual or non-standard properties where there is a thin comparable market, making the valuation inherently uncertain.

Buyers facing a down-valuation typically have three options: renegotiate the agreed purchase price with the seller; increase the deposit to cover the gap between the valuation and the purchase price; or challenge the valuation through the lender's appeals process by providing fresh comparable evidence.

Important limitations

This article provides general guidance only. Mortgage lending criteria, LTV thresholds, valuation methodology, and energy efficiency regulations can change. Individual property valuations depend on specific physical, legal, and market factors that only a RICS-registered valuer inspecting the property can assess accurately. Nothing in this article constitutes mortgage advice, financial advice, legal advice, or a valuation. Always consult a qualified mortgage adviser and a RICS-registered valuer before making decisions based on valuation or lending expectations.

What to ask a qualified professional

Before instructing a valuation survey or challenging a down-valuation, consider asking:

- Is the valuer RICS-registered and experienced in this property type and local market?

- What comparable sales evidence was used, and from what date range?

- If a retention has been imposed, what work is required and who must sign it off?

- If challenging a down-valuation, what format of comparable evidence does the lender require and within what timeframe?

- Does the mortgage valuation flag anything that would warrant commissioning a separate RICS Home Survey?

- Are there any property characteristics — tenure, construction type, or building safety — that could restrict the pool of lenders willing to offer on this property?

When to get professional help

Seek independent professional advice if:

- The mortgage valuation comes in below the agreed purchase price and you are unsure how to respond.

- The valuation report references structural movement, severe damp, non-standard construction, or fire-safety concerns.

- The property is leasehold with fewer than 85 years remaining on the lease.

- You are buying a flat in a building where cladding remediation or fire safety works remain unresolved.

- You want an independent assessment of the property's condition — separate from and in addition to what the lender requires.

How Housey can help

If you want an independent assessment of a property that goes beyond the lender's mortgage valuation, Housey can connect you with qualified professionals for a valuation survey or a RICS Home Survey. For properties showing signs of structural concern, you can also request a structural survey — giving you condition and value information that protects your interests, not just the lender's.

Frequently asked questions

What is the difference between a mortgage valuation and a RICS Home Survey?

A mortgage valuation is commissioned by the lender to confirm the property is adequate security for the loan. It does not advise the buyer on condition or repair costs. A RICS Home Survey is commissioned by and for the buyer, providing condition ratings and recommendations on defects. The two serve entirely different purposes and should not be treated as interchangeable.

Can a lender down-value a property below the agreed purchase price?

Yes. If the RICS valuer concludes the property is worth less than the agreed price, the lender will base their offer on the lower figure. Buyers can renegotiate the price with the seller, provide a larger deposit to cover the gap, or challenge the valuation through the lender's appeals process with fresh comparable sales evidence.

Does the EPC rating affect whether a buy-to-let mortgage is approved?

In England and Wales, a property rated F or G cannot legally be let under Minimum Energy Efficiency Standards and may be declined by lenders as security for a buy-to-let mortgage. For owner-occupied purchases, EPC ratings do not typically prevent approval, though some lenders offer preferential rates for energy-efficient homes.

What is a mortgage retention and when does it apply?

A mortgage retention is when a lender withholds part of the agreed mortgage offer until specified remedial works are completed and signed off — typically by a chartered surveyor or approved contractor. Retentions are commonly applied when the valuer identifies significant defects such as structural movement, severe damp, or major roof damage that the lender considers a risk to their security.

How do rising interest rates affect property valuations?

Rising rates reduce buyer purchasing power, which can soften demand and compress comparable sales evidence — the data valuers use to assess market value. Valuers do not adjust valuations mechanically for rate changes, but sustained market softening eventually feeds into weaker comparable evidence, which constrains future valuation figures and can reduce what lenders are willing to offer.

Sources and further reading

- RICS Valuation – Global Standards (Red Book) — RICS

- Minimum Energy Efficiency Standards: landlord guidance — GOV.UK

- Mortgage lenders and administrators statistics — Bank of England

- Buying a home: getting a mortgage — Citizens Advice

- External wall system fire review (EWS1) — RICS

Useful next reads

Surveys & Inspections

Surveys & InspectionsProperty financing checklist: understanding valuation requirements and mortgage lending criteria

Mortgage lenders require their own valuation before releasing funds — this confirms the property is adequate security, not its condition.

Surveys & Inspections

Surveys & InspectionsGetting a Valuation Survey Before Selling Your Property

Before selling, a free estate agent appraisal gives a market price guide, but only a RICS Red Book valuation carries formal professional standards and legal weight.

Surveys & Inspections

Surveys & InspectionsProperty Valuation Survey: Understanding Market Worth and Cost Assessment

A property valuation survey establishes a property's market value at a specific date.

Surveys & Inspections

Surveys & InspectionsIdentifying and managing asbestos roof tiles

If your roof was installed before 2000, asbestos cement tiles may be present.

Surveys & Inspections

Surveys & InspectionsAsbestos in homes: identification, risks and management

Asbestos was widely used in UK construction until it was banned in November 1999, so any home built before 2000 may contain asbestos-containing materials.