Property Valuation Factors: Elements Affecting Home Assessment

By Housey · Last reviewed 31st of May 2026

Property Valuation Factors: Elements Affecting Home Assessment

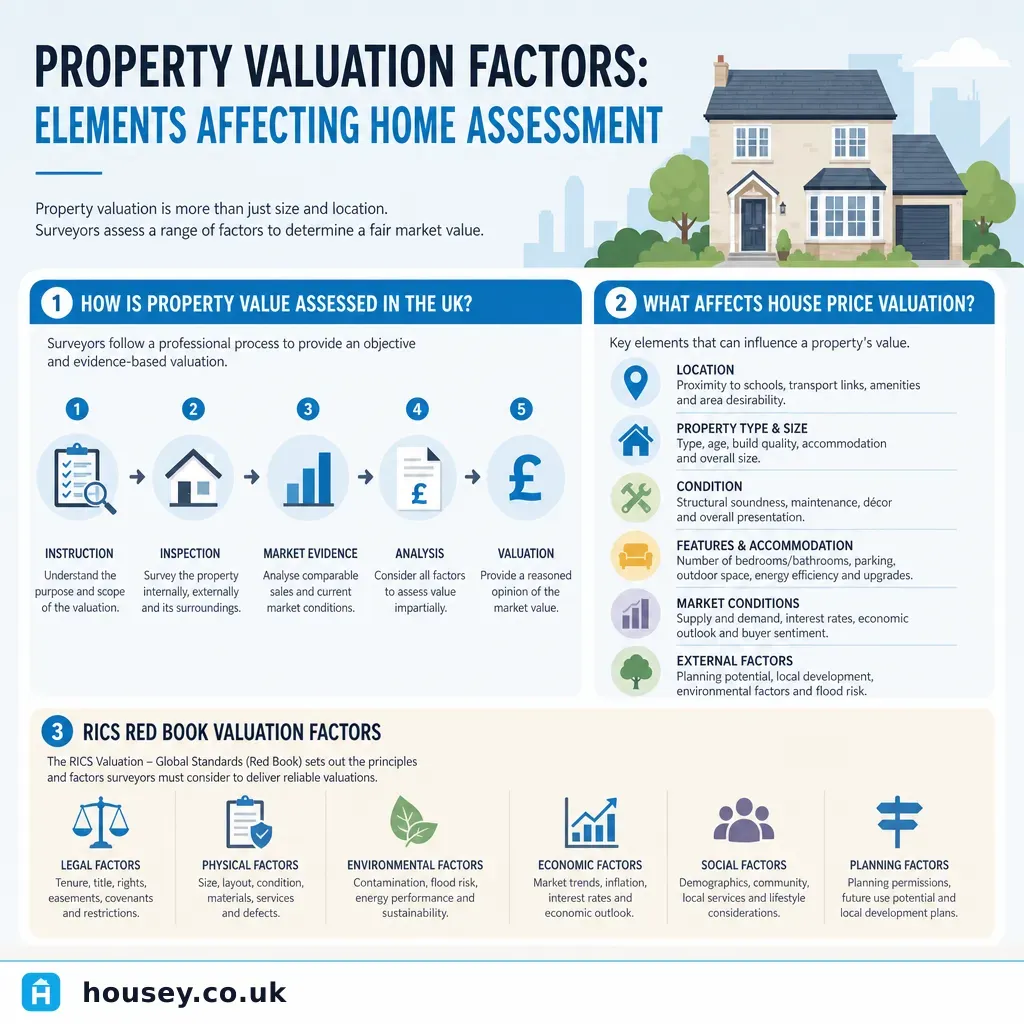

UK homeowners encounter property valuations at several pivotal moments — when selling, remortgaging, buying, or reviewing their buildings insurance. Understanding what drives a valuation outcome helps you prepare effectively, question a result with evidence, and avoid costly surprises at exchange or completion.

Key points

- RICS Red Book valuations follow RICS Valuation — Global Standards, the professional framework used for mortgage, probate, matrimonial, and dispute valuations across the UK.

- Location is the single most influential factor, with proximity to well-rated schools, transport links, and employment centres commanding the highest premiums in comparable evidence.

- Property condition can shift a valuation by thousands of pounds; visible defects such as damp, cracked render, or a failing roof are noted by valuers and may trigger a lender retention.

- Floor area is measured using the RICS IPMS 3 residential standard (in square metres) and used alongside price-per-square-metre data from comparable sales.

- Leasehold properties with fewer than 80 years unexpired are progressively harder to mortgage, and below 70 years many high-street lenders decline to lend at all.

What a property valuation is — and what it is not

A property valuation is a professional opinion of market value (or another defined basis, such as insurance reinstatement cost) at a specific date. It is not:

- A survey of condition — a RICS Level 2 or Level 3 Home Survey assesses the fabric and defects of the building.

- A guarantee of the price you will achieve if you sell.

- An automated valuation model (AVM) estimate from a portal such as Rightmove or Zoopla.

For mortgage purposes, lenders commission a mortgage valuation — often a brief desktop or drive-by assessment confirming the property is suitable security for the loan. A full RICS Red Book valuation for probate, matrimonial proceedings, Help to Buy repayment, or shared ownership staircasing is a more detailed exercise requiring a physical internal inspection.

Location and comparable sales

Valuers rely primarily on comparable evidence — recent sales of similar properties in the same area. HM Land Registry records all registered sales in England and Wales, and valuers cross-reference this with local market knowledge.

Key location factors include:

- Postcode sector and street-level desirability

- Proximity to Ofsted-rated schools, particularly Outstanding-rated primaries

- Train station walking distance and journey times to major employment centres

- Local crime statistics (available from police.uk)

- Flood risk zone — Environment Agency flood maps are routinely consulted

- Proximity to commercial, industrial, or noisy infrastructure

Physical characteristics and condition

Factor | Positive effect on value | Negative effect on value |

|---|---|---|

Floor area (sq m) | Larger than comparables for the area | Smaller or awkwardly configured |

Number of bedrooms | Matches local buyer demand | Fewer than typical for the street |

Outdoor space | South-facing garden, off-street parking | No garden; on-street parking only |

Condition | Recently renovated, new roof and windows | Active damp, structural cracks, failing roof |

EPC rating | Band C or above | Band E, F, or G — especially relevant for buy-to-let |

Extension or loft conversion | Adds usable floor area with planning compliance | Unpermitted works or non-compliant glazing |

Leasehold tenure | Lease 125+ years unexpired | Sub-80 years — a known mortgage risk |

Condition is assessed visually during an inspection. Valuers are not structural defect specialists, but they will note visible problems and may recommend a lender retention — withholding part of the mortgage advance pending remediation.

Legal and tenure factors

Leasehold properties: A lease with fewer than 80 years unexpired becomes progressively harder to mortgage and less attractive to buyers. Once below 80 years, the marriage value calculation under the Leasehold Reform, Housing and Urban Development Act 1993 makes statutory lease extension more expensive.

Restrictive covenants: Old covenants preventing certain uses or alterations can deter buyers and may reduce value, particularly where enforcement risk remains live.

Planning enforcement: Live enforcement notices or unresolved permitted development disputes will typically appear in conveyancing searches and can reduce value and delay exchange.

Building regulations compliance: Retrospective evidence — a completion certificate or an indemnity insurance policy — for extensions, conversions, or electrical work matters. Its absence can affect value and saleability.

EPC rating and energy performance

Since April 2020, privately rented properties in England and Wales must have an EPC rating of at least E to be legally let under the Minimum Energy Efficiency Standards (MEES). The Government has consulted on raising this threshold to Band C for new tenancies. This regulatory backdrop means:

- An F or G-rated property carries a measurable discount in investment valuations.

- Improvements that lift a property from E to C — loft insulation, cavity wall insulation, a heat pump — can add measurable value, particularly in the buy-to-let and first-time buyer markets.

- For owner-occupier valuations, energy efficiency is an increasingly salient factor as buyers factor in running costs.

Worked example: 1930s semi-detached in the East Midlands

A three-bedroom 1930s semi with 85 sq m of floor area in a market town near a railway station is being valued for remortgage purposes.

Positive factors: Band D EPC (close to C following recent loft insulation), south-facing rear garden, off-street parking, and two comparable sales in the same street within the past three months.

Negative factors: Original single-glazed windows at the front (conservation area — replacement requires consent), a visible crack in the rear gable wall, and a shared garage with unclear tenure not registered at Land Registry.

Likely valuer response: The crack may prompt a note in the report and a possible retention. The conservation area windows are not a defect but limit improvement options. The garage tenure would be flagged for the conveyancer. Using the three recent comparables, the valuer would adjust downward for condition. The assessed figure could sit 5–8% below a comparable fully renovated property nearby.

This is a worked illustration only; actual valuations depend on current market conditions and individual professional judgement.

Homeowner checklist: preparing for a valuation

Important limitations

This article provides general information about factors that commonly influence property valuations in England and Wales. Valuation is a professional judgement exercise — the same property can yield different figures from different valuers depending on the comparable evidence available, the basis of valuation required, and the date of inspection. Nothing in this article constitutes a formal valuation opinion. Always instruct a RICS-registered valuer for any purpose that has legal, financial, or insurance consequences.

What to ask a qualified professional

- What basis of valuation are you using — market value, insurance reinstatement cost, or another defined basis?

- Which comparable sales are you relying on, and how recent are they?

- Will this be a full RICS Red Book valuation or a mortgage valuation?

- Will you inspect internally, or is this a desktop or drive-by assessment?

- What factors might trigger a retention or reduce the figure, and what evidence could address them?

- Are you on the approved panel of my mortgage lender?

When to get professional help

A professional valuation is essential whenever the result has financial or legal consequences:

- Remortgaging or releasing equity

- Probate — the Valuation Office Agency will scrutinise figures submitted for Inheritance Tax purposes

- Matrimonial or partnership dissolution

- Shared ownership staircasing or Help to Buy repayment

- Lease extension negotiation under the Leasehold Reform, Housing and Urban Development Act 1993

- If you believe a lender's mortgage valuation is materially too low (formal challenge routes include a Homebuyer's Response and RICS dispute resolution)

How Housey can help

Housey connects you with RICS-registered professionals who carry out valuation surveys and insurance valuations. Compare quotes from local experts, check credentials, and get the formal opinion you need — whether for a remortgage, probate, or insurance reinstatement calculation.

Frequently asked questions

How is market value defined for a UK property valuation?

Market value is defined by the RICS Red Book as the estimated amount for which a property should exchange on the date of valuation between a willing buyer and a willing seller in an arm's length transaction after proper marketing, where both parties are knowledgeable and neither is under compulsion to buy or sell.

Can I dispute a mortgage valuation that seems too low?

Yes. You can ask your lender to commission a second valuation or instruct your own RICS-registered valuer to prepare a counter-valuation. If you believe the valuer made a material error, the RICS dispute resolution service and the Financial Ombudsman Service both provide formal avenues for challenge.

Does a new kitchen or bathroom always add value?

Not always. Comparable properties and local demand set the ceiling. A newly fitted kitchen may help a property sell faster but rarely adds pound-for-pound value above a tidy existing kitchen. Valuers assess whether an improvement has added floor area or brought the property up to market standard — cosmetic upgrades above the local norm seldom add measurable value.

How does lease length affect a property valuation?

Leases below 80 years unexpired are harder to mortgage and less attractive to many buyers. Below 70 years, many high-street lenders decline to lend. Extending the lease before selling via the statutory route under the Leasehold Reform, Housing and Urban Development Act 1993 can materially increase value and saleability for qualifying leaseholders who have owned for at least two years.

Sources and further reading

- RICS Valuation — Global Standards (Red Book) — RICS

- UK House Price Index — HM Land Registry

- Minimum Energy Efficiency Standards (MEES) for landlords — GOV.UK

- Leasehold Reform, Housing and Urban Development Act 1993 — legislation.gov.uk

- Check the flood risk for your area — Environment Agency / GOV.UK

Useful next reads

Surveys & Inspections

Surveys & InspectionsProperty Valuation Survey: Understanding Market Worth and Cost Assessment

A property valuation survey establishes a property's market value at a specific date.

Surveys & Inspections

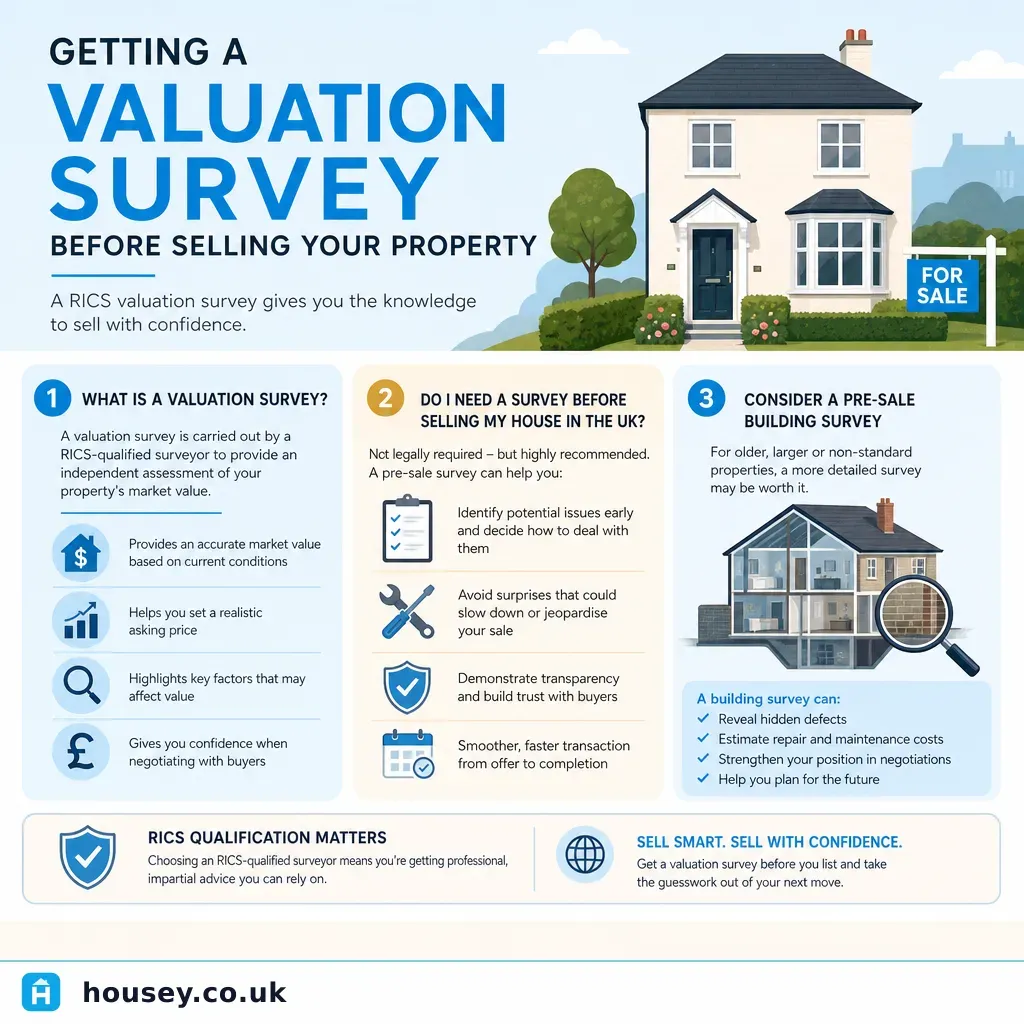

Surveys & InspectionsGetting a Valuation Survey Before Selling Your Property

Before selling, a free estate agent appraisal gives a market price guide, but only a RICS Red Book valuation carries formal professional standards and legal weight.

Surveys & Inspections

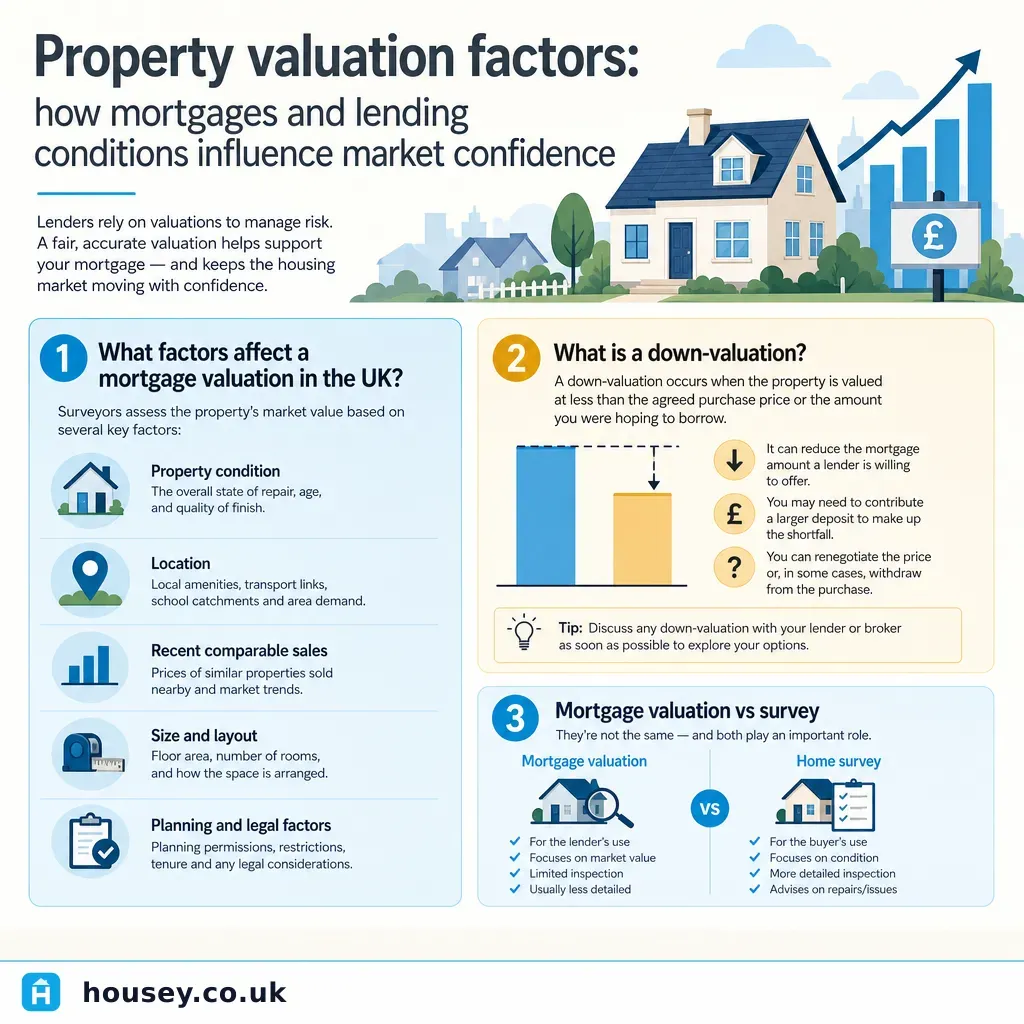

Surveys & InspectionsProperty valuation factors: how mortgages and lending conditions influence market confidence

Mortgage lenders base their offer on the lower of the agreed purchase price or the surveyor's valuation.

Surveys & Inspections

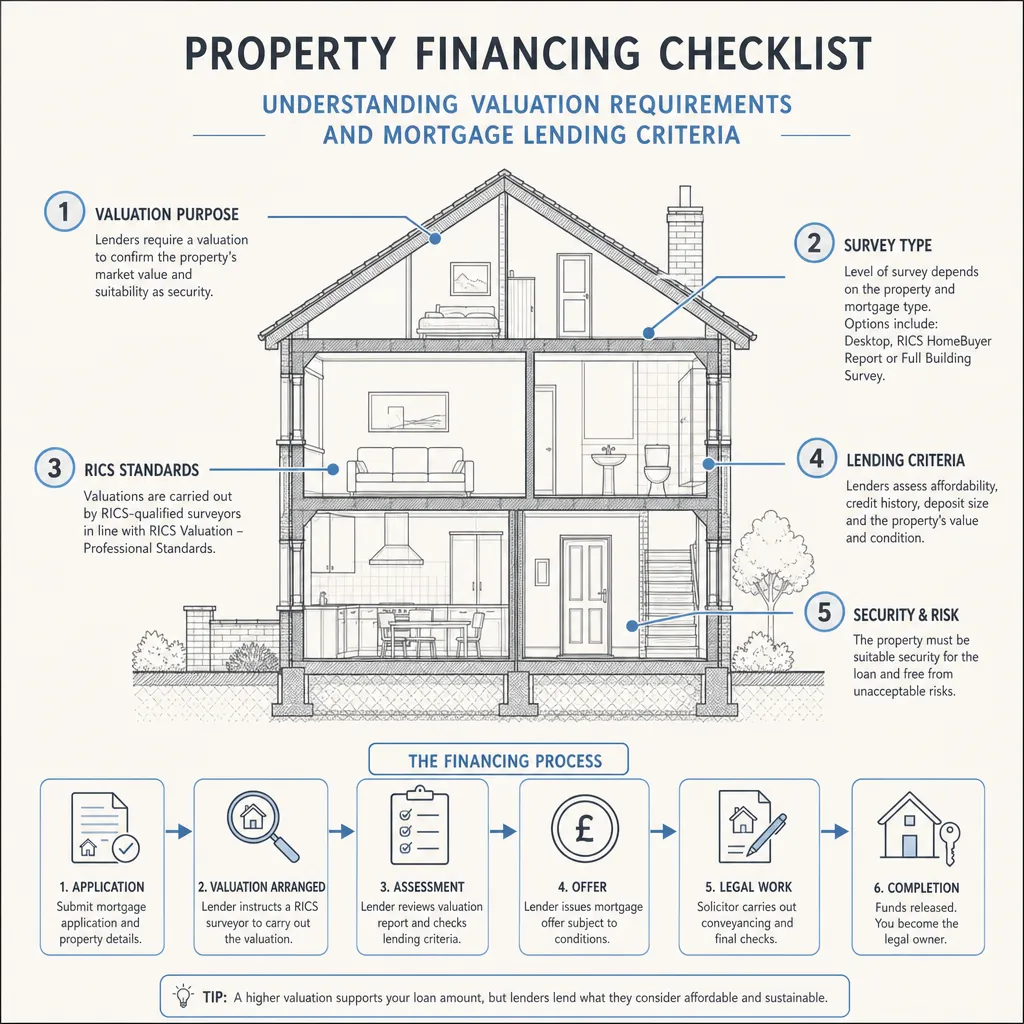

Surveys & InspectionsProperty financing checklist: understanding valuation requirements and mortgage lending criteria

Mortgage lenders require their own valuation before releasing funds — this confirms the property is adequate security, not its condition.

Surveys & Inspections

Surveys & InspectionsWhen to Commission a Home Survey During Property Purchase

Commission a home survey after your offer is accepted and before exchange of contracts.