Property Type Preferences: Understanding Market Demand

By Housey · Last reviewed 10th of May 2026

Property Type Preferences: Understanding Market Demand

The UK housing market offers a diverse range of property types — from Victorian terraced houses to purpose-built modern flats — each attracting different buyer profiles, commanding different prices, and performing differently across regions and economic cycles. Whether you are a first-time buyer assessing what your budget can realistically secure, a homeowner trying to understand your competitive position, or someone planning a move and wanting to know where demand is strongest, understanding how property types compare across the market is a practical starting point.

Key points

- Semi-detached houses are consistently the most purchased property type by transaction volume in England and Wales, according to HM Land Registry price paid data.

- Terraced houses represent a disproportionately large share of first-time buyer purchases, reflecting affordability constraints as much as preference.

- The early 2020s saw detached houses post some of the strongest price growth in many regions, driven partly by increased demand for space and gardens as working patterns shifted.

- Leasehold tenure — most common in flats — carries specific legal and financial considerations including ground rent, service charges, and lease length, all of which affect value and saleability.

- The Leasehold and Freehold Reform Act 2024 introduced significant changes to leasehold rights in England and Wales that buyers and sellers of flats should understand before exchange.

How property type demand breaks down in the UK

HM Land Registry price paid data consistently shows semi-detached and terraced houses dominating transaction volumes across England and Wales. Detached houses and flats each account for meaningful but smaller shares, with flats particularly concentrated in London and major urban centres.

Buyer demand by property type broadly reflects life-stage needs, budget, and regional housing stock.

Property type | Typical buyer profile | Key demand drivers | Main considerations |

|---|---|---|---|

Detached house | Growing families, move-up buyers, those prioritising space and privacy | Privacy, garden, extension potential, no shared walls | Higher maintenance costs; usually freehold; smaller buyer pool |

Semi-detached house | First-time buyers, young families, upsizers | Balance of space, garden, and relative affordability | Party wall for extensions; usually freehold; strong market liquidity |

Terraced house | First-time buyers, city dwellers, investors | Affordability, urban location, character in older stock | Party wall on both sides; sometimes leasehold |

Flat or maisonette | Single buyers, young professionals, downsizers, investors | City-centre affordability, lower external maintenance | Leasehold issues, lease length, service charges, building safety |

New-build (any type) | First-time buyers using incentives, those avoiding renovation | Modern energy performance, warranties, no immediate works needed | Developer premium at purchase; snagging period; leasehold reform ongoing |

Bungalow | Older buyers, downsizers, those with accessibility needs | Single-storey living, often generous plots, low-step access | Scarce supply; often commands higher price per m²; extension potential |

Why semi-detached houses dominate UK transactions

Semi-detached houses offer a balance of space, garden access, and relative affordability compared to detached properties, making them the most liquid segment of the UK housing market. They exist in sufficient quantity across almost every town and suburb in England and Wales, and they serve a broad range of buyer needs — from first-time buyers stretching their budget to growing families seeking more space than a terrace can provide.

Their prevalence reflects the UK's interwar and postwar housebuilding eras, when the semi-detached form became the default template for mass residential development. The majority of housing stock built between roughly 1920 and 1970 across England and Wales follows this pattern, providing deep and familiar supply at a range of price points. For sellers, this also means plenty of comparable evidence to support asking prices and valuations.

Flats: a more complex picture

Demand for flats varies more sharply by location than any other property type. In central London and many major cities, flats represent the primary entry point for buyers working within typical salary and deposit constraints. Demand is driven partly by first-time buyers and partly by investors seeking rental yield in areas with strong employment.

However, the flat market has faced specific challenges in recent years that buyers and sellers should be aware of:

- Cladding and building safety: Following the Building Safety Act 2022, leaseholders in buildings with cladding defects gained important new legal protections, but remediation is still ongoing in many blocks. Mortgage lenders continue to treat some buildings with caution. Buyers should check whether a flat requires an EWS1 (External Wall System) assessment form before making an offer, particularly in buildings over 11 metres.

- Leasehold reform: The Leasehold and Freehold Reform Act 2024 introduced significant changes to the leasehold system in England and Wales, including improved routes to lease extension and restrictions on certain ground rent terms. Buyers should check current lease length carefully — leases below 80 years become progressively harder and more expensive to extend, and can affect mortgage availability.

- Service charges: Rising service charges, particularly in older buildings requiring major works to roofs, lifts, or communal plant, have affected some buyers' ability to sell or remortgage. Requesting at least three years of service charge accounts and the most recent major works schedule before exchange is standard practice.

Detached houses: the premium segment

Detached houses represent the aspirational end of the mainstream market for most UK buyers. They typically offer the greatest privacy, the largest plots, and the most scope for extension under permitted development rights. Demand is consistent but the buyer pool is smaller, as pricing frequently places detached houses beyond first-time buyers and many second-time buyers in higher-cost regions.

The early 2020s saw notable demand for detached homes in rural, coastal, and commuter belt locations as remote working made daily commuting less essential for some households. This produced above-average price growth in specific markets, though the extent of that growth varied considerably by region. Buyers in some northern cities can access detached houses at prices that would secure a one-bedroom flat in central London — a difference that has attracted relocation buyers and remote workers to markets including Leeds, Sheffield, and parts of the Midlands.

Terraced houses: broad appeal and urban character

Terraced houses account for a large share of the UK's total housing stock, particularly in northern English cities, South Wales valleys, and the inner suburbs of most major conurbations. Their appeal among first-time buyers reflects affordability rather than preference alone — a terrace is often the largest property a buyer can access at a given income and deposit level.

In areas such as Manchester, Leeds, Liverpool, and Sheffield, Victorian and Edwardian terraces have attracted buyers who value character, proximity to city centres, and renovation potential. In some of these markets, well-presented terraces with period features sell quickly and may command a premium over newer-built alternatives of similar square footage.

Decision tree: which property type suits your situation?

- Choose a flat if you are buying in a high-cost city centre, prioritise low external maintenance, or are purchasing as a rental investment; always check lease length, service charge history, and any outstanding building safety matters first.

- Choose a terraced house if you want a garden and more internal space than a flat at a lower price point than a semi-detached, particularly in an urban or inner-suburban area.

- Choose a semi-detached house if you want a broadly liquid, well-supplied, versatile property that is straightforward to sell in most UK markets; it suits a wide range of life stages and buyer profiles.

- Choose a detached house if space, privacy, and extension potential are your priorities and your budget supports it; verify what the plot, local planning context, and permitted development rights allow before committing.

- Choose a new-build if you want modern insulation, high energy ratings, and a developer warranty with minimal immediate renovation; factor in the new-build premium and allow time for a snagging inspection.

- Ask a RICS-accredited surveyor if you are uncertain about the structural condition of any property, particularly older terraced or semi-detached homes showing signs of damp, roof wear, or movement.

- Ask a solicitor with leasehold experience before exchange if a flat has a lease below 80 years, high service charges, or any unresolved building safety matters.

What sellers should know about their property type

Understanding where your property type sits in the local market helps you set realistic expectations before listing:

- Semi-detached and terraced houses in good condition typically attract a broader pool of buyers and sell more quickly than most flats in many regional markets.

- Flats may require additional preparation — particularly around lease documentation, service charge accounts, and building safety certificates — to satisfy buyers and their mortgage lenders before they can proceed.

- Detached houses attract a smaller pool of qualified buyers but those buyers are often more committed, more certain of their finances, and in a clearer position to proceed.

- Bungalows in popular coastal, rural, or retirement-oriented areas can attract strong competition from a specific demographic, sometimes resulting in above-asking offers.

When to get professional help

For most purchases, a RICS-accredited surveyor, a licensed conveyancer or solicitor, and an independent mortgage adviser provide the core professional support. Specific situations warrant additional expertise:

- Flat with potential cladding or building safety concerns: Instruct a solicitor experienced in building safety law before exchange. Ask the vendor or managing agent for the EWS1 form and the most recent Fire Risk Assessment for the building.

- Older terraced or semi-detached with visible defects: Consider a RICS Level 3 Building Survey rather than a RICS Level 2 Home Survey if there is evidence of damp, cracking, past alterations, or roof deterioration.

- Detached house with outbuildings or extensions: Verify the planning permission and building regulations history for any added structures before exchange. Your solicitor should raise these enquiries, but asking explicitly about planning certificates and completion certificates is advisable.

- New-build: Commission an independent snagging survey before legal completion, not after moving in. Defects are easier and cheaper to resolve while the developer retains legal responsibility under the warranty.

How Housey can help

Housey connects UK homeowners and buyers with qualified property professionals — from RICS-accredited surveyors and structural engineers to conveyancers and planning consultants. Whatever property type you are buying, selling, or assessing, Housey can help you request and compare quotes from relevant local specialists.

Frequently asked questions

Which property type holds its value best in the UK?

No single type uniformly outperforms all others. Detached and semi-detached houses have generally shown strong long-term price growth across most of England and Wales. Flats have shown more variable performance, particularly where leasehold issues, cladding remediation costs, or rising service charges have affected saleability. Location, condition, and for flats, lease length all have significant influence on long-term value.

Are flats harder to sell than houses in the UK?

In many markets, flats take longer to sell than comparable houses and attract a narrower buyer pool. This is particularly true where mortgage lenders are cautious about cladding, where lease lengths are short, or where service charges are high. In high-demand city-centre locations, well-positioned flats with long leases and manageable service charges can sell quickly and at competitive prices.

Do new-builds lose value immediately after purchase?

New-builds are often sold at a premium over comparable second-hand properties. Some buyers experience depreciation in the early years, particularly if the developer priced aggressively. Over the longer term, value is shaped by location, condition, and market conditions rather than new-build status alone. New-builds typically carry EPC ratings of A or B, which may become an increasingly relevant selling point as energy efficiency standards evolve.

What is a bungalow premium and why does it exist?

Bungalows offer single-storey living with no stairs, which appeals strongly to older buyers, those with mobility needs, and those attracted by often generous plot sizes. Supply of bungalows is limited relative to demand — they are rarely built in significant numbers today — creating a per-square-metre premium in many areas. In popular coastal and rural locations, competition from a specific demographic can be strong.

Does property type affect the mortgage products available to me?

Yes. Lenders apply different criteria depending on property type. Flats in high-rise buildings may face restrictions related to cladding, construction method, or lease length. Some non-standard construction types may require specialist lenders. New-builds may attract loan-to-value restrictions. Standard houses generally face fewer type-specific constraints, though individual condition issues or very short lease terms on flats can still affect lender appetite.

Sources and further reading

- HM Land Registry: UK House Price Index reports — HM Land Registry

- GOV.UK: Leasehold and Freehold Reform Act 2024 — GOV.UK

- GOV.UK: Building Safety Act 2022 — GOV.UK

- RICS: Home surveys and valuations guidance — Royal Institution of Chartered Surveyors

- ONS: UK House Price Index latest bulletin — Office for National Statistics

Useful next reads

General property advice

General property adviceLondon Property Costs vs Regional Alternatives: Price Comparison

London's average property price is roughly double the UK average and around three times higher than cities such as Manchester, Leeds, and Birmingham.

General property advice

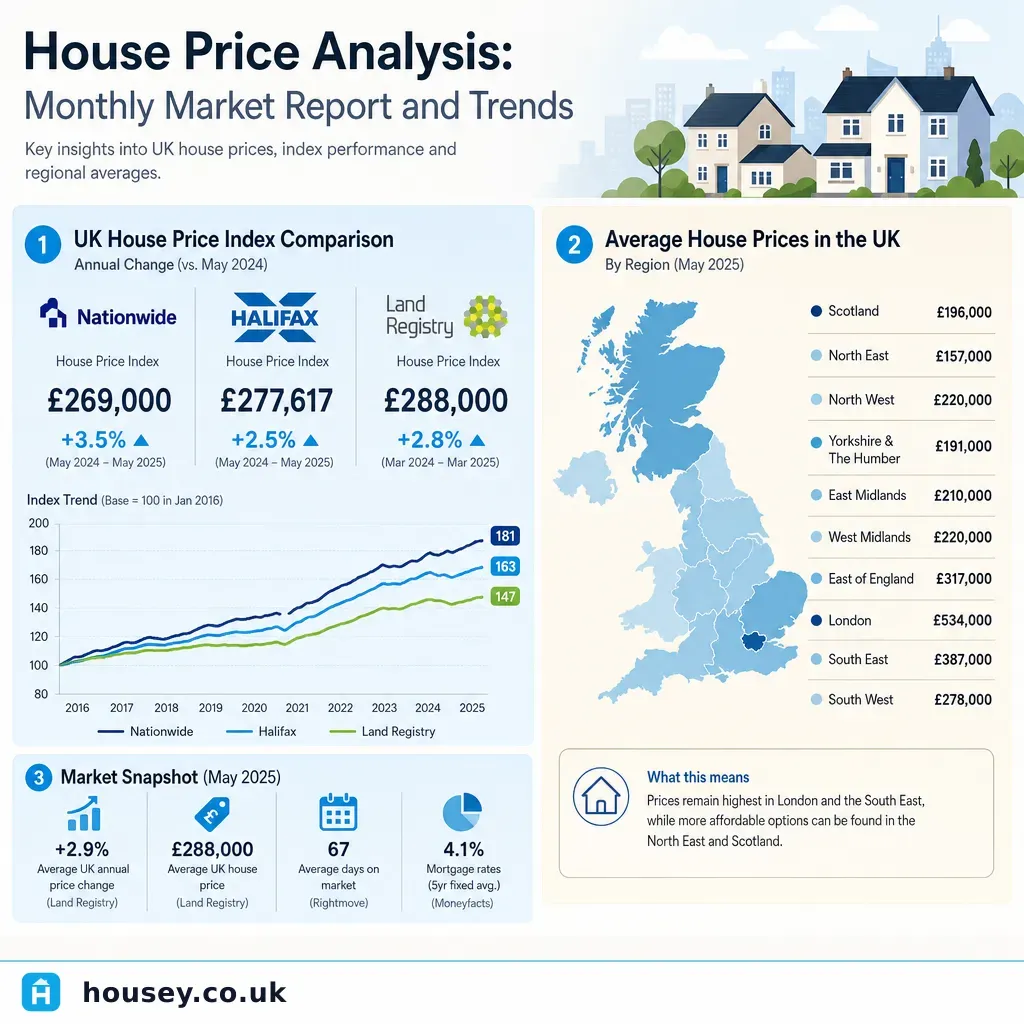

General property adviceHouse Price Analysis: Monthly Market Report and Trends

UK house prices are tracked by several major indices — the HM Land Registry UK House Price Index, the ONS House Price Index, and lender-based measures from Nationwide and Halifax.

General property advice

General property adviceGarden Space Demand: What Modern Homebuyers Are Looking For

Gardens and private outdoor space rank among the most sought-after features for UK homebuyers, particularly since 2020.

General property advice

General property adviceWhat to do when your boiler stops working

When your boiler stops working, check the pressure gauge (should read 1–1.

General property advice

General property adviceProperty Market Trends: Activity Growth and Price Movements

UK property market activity is measured through completed sale registrations (HM Land Registry), lender mortgage data, and transaction volumes from HMRC.