Property Valuations and Appraisals: Understanding the Costs

By Housey · Last reviewed 31st of May 2026

Property Valuations and Appraisals: Understanding the Costs

A formal property valuation is required at several points in a homeowner's journey — not only when buying. Remortgaging, equity release, probate, matrimonial proceedings, Help to Buy loan redemption, and capital gains tax calculations all typically require a valuation from a RICS Registered Valuer. Understanding which type of valuation you need, who commissions it, and what it costs prevents both unnecessary expenditure and the risk of relying on an assessment that is not fit for its intended legal or financial purpose.

Key points

- In the UK, the standard term is 'valuation', not 'appraisal' (the American equivalent) — a formal RICS Red Book valuation carries professional indemnity protection and is required for most legal and financial purposes.

- A mortgage lender's valuation is commissioned and controlled by the lender to protect its loan — it is not independent advice to the borrower and must not be relied on as a substitute for independent professional assessment.

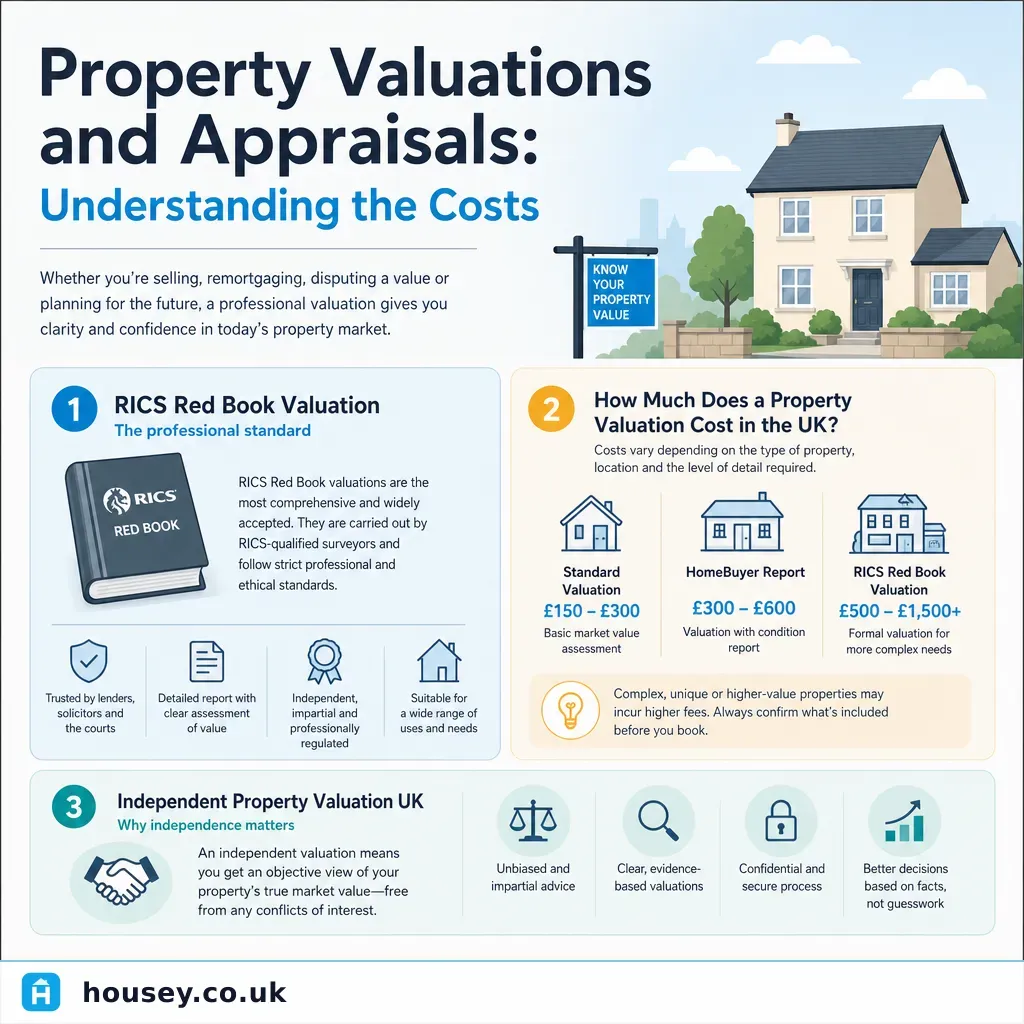

- RICS Red Book valuations (produced under RICS Valuation — Global Standards) are required for secured lending disputes, probate, matrimonial proceedings, Help to Buy equity loan redemption, and other regulated or legal purposes.

- Indicative fees: £250–£600 for a standard residential RICS Red Book valuation; probate and matrimonial valuations may cost more due to report complexity. (Indicative UK costs, last reviewed 2026-05-31.)

- Automated valuation models (AVMs) — used by some lenders for low-risk remortgages — are algorithmic estimates. They carry no professional liability for the borrower and are not accepted for probate, litigation, leasehold extension, or most formal regulated purposes.

What is a property valuation in the UK?

A property valuation is a professional assessment of a property's open market value at a specific date. In the UK, formal valuations are carried out under the RICS Valuation — Global Standards (commonly called the Red Book), which sets out methodologies, ethical requirements, and reporting standards for RICS Registered Valuers.

The term 'appraisal' is the American equivalent and appears in some mortgage comparison content aimed at international audiences. UK lenders, solicitors, and estate agents almost always refer to a 'valuation'.

An estate agent's valuation — typically called a market appraisal — is a commercially motivated estimate intended to support pricing and marketing decisions. It carries no professional indemnity protection and is not accepted by lenders, HMRC, or courts for formal purposes.

Which type of valuation do you need?

Purpose | Type required | Who commissions it | Who pays |

|---|---|---|---|

Mortgage application (purchase) | Lender's valuation | The lender | Usually the buyer as a product fee; sometimes waived |

Remortgage | Lender's valuation or AVM | The lender | Often waived or included in the remortgage product |

Probate and inheritance tax | RICS Red Book valuation | The executor or administrator | The estate |

Matrimonial or divorce proceedings | RICS Red Book valuation | One or both parties | As agreed or ordered by the court |

Help to Buy equity loan redemption | RICS Red Book valuation | The homeowner | The homeowner |

Capital gains tax (base cost) | RICS Red Book valuation | The owner | The owner |

Equity release | Lender's valuation | The lender | Usually the homeowner as a completion cost |

Leasehold extension or enfranchisement | RICS Red Book valuation | The leaseholder or freeholder | Usually the instructing party |

How much does a property valuation cost?

Fees vary by purpose, property type, and the complexity of the report required.

Indicative UK costs, last reviewed 2026-05-31. Obtain written quotes — fees vary by region, surveyor, and instruction complexity.

Valuation type | Typical fee range |

|---|---|

Mortgage valuation (lender-instructed) | £0–£500 (often waived or product-included) |

RICS independent residential valuation | £250–£600 |

Probate valuation | £300–£700+ |

Matrimonial valuation | £400–£900+ |

Help to Buy redemption valuation | £200–£500 |

Leasehold extension valuation | £600–£1,500+ |

Leasehold extension valuations sit at the higher end because the calculation requires specialist knowledge of lease terms, ground rent, and marriage value under the Leasehold Reform, Housing and Urban Development Act 1993, and the more recent Leasehold and Freehold Reform Act 2024, which introduced further changes to the premium calculation framework.

The difference between a valuation and a condition survey

These two products are frequently confused:

- A valuation answers: what is this property worth at this date?

- A condition survey (RICS Level 2 or Level 3) answers: what is the condition of this property and what defects exist?

RICS Level 2 and Level 3 surveys include a market valuation section within the report, but their primary purpose is condition reporting — identifying defects, risks, and items requiring attention or repair. If you need a figure for a legal or financial purpose, a standalone RICS Red Book valuation is the appropriate product. If you are buying and want both condition and value assessed, a RICS Level 2 or Level 3 survey often represents better value than commissioning both products separately.

What to ask before instructing a valuer

- Is the surveyor a RICS Registered Valuer? Verify via RICS Find a Surveyor.

- Will the valuation comply with the RICS Red Book (RICS Valuation — Global Standards)?

- What comparable evidence will be used, and how recently were those transactions completed?

- Will you physically inspect the property, or is this a desktop or drive-by valuation?

- Will the report be accepted by the intended recipient — lender, court, HMRC, or Help to Buy agent — for my specific purpose?

- Is VAT included in the quoted fee?

- How long will the written report take to produce after the inspection?

Important limitations

This article provides general information about property valuation types and indicative costs in the UK. Fees, report requirements, and the appropriate valuation type vary by lender instructions, solicitor requirements, jurisdiction (Scotland and Northern Ireland have some different practices), and the specific legal or financial purpose. Indicative cost ranges may not reflect current local market rates. This article does not constitute financial or legal advice. Always instruct a RICS Registered Valuer and confirm that the report will be accepted for its intended purpose before commissioning.

When this becomes urgent

Seek professional advice without delay if:

- You have received a down-valuation from a mortgage lender that threatens your mortgage offer.

- Probate has been delayed because no HMRC-acceptable valuation of the estate's property has been obtained.

- You are involved in leasehold extension or collective enfranchisement proceedings where the valuation will directly determine the premium payable.

- A valuation is required as evidence in court or arbitration proceedings.

What to ask a qualified professional

Ask your RICS Registered Valuer:

- Is the methodology you will use appropriate for the purpose I have described — probate, matrimonial, lending, or leasehold extension?

- Will my lender, HMRC, or the court accept this report format and methodology?

- My property has unusual features (listed building status, flood risk zone, non-standard construction) — how will these affect your approach and the reported value?

- If the valuation comes in lower than expected, what are the options available to me?

- Will you provide a verbal indication of likely value before the final written report is issued?

When to get professional help

Always instruct a RICS Registered Valuer for formal valuations required for legal, tax, or mortgage purposes. Do not rely on an estate agent's market appraisal or an automated valuation model for any purpose that requires professional indemnity-backed advice.

If a down-valuation is affecting your mortgage offer, a surveyor can explain the basis of their figure and the comparable evidence used. A mortgage broker can advise on whether switching lenders, providing additional evidence, or challenging the valuation formally is likely to help in your circumstances.

How Housey can help

Housey connects homeowners with RICS-registered professionals for valuation surveys and RICS Home Surveys. Compare written quotes from qualified valuers and surveyors before instructing.

Frequently asked questions

What is the difference between a property valuation and a survey?

A valuation establishes what a property is worth at a given date. A survey assesses the condition of the property — identifying defects, risks, and repair priorities. RICS Level 2 and Level 3 surveys include a market valuation section, but their primary function is condition reporting. Commission an RICS Red Book valuation for legal or financial purposes; commission a Level 2 or Level 3 survey for condition advice when buying.

Will my mortgage lender accept an independent RICS valuation?

Most mortgage lenders instruct their own approved panel valuers and will not accept a valuation commissioned directly by the borrower for lending purposes. Some lenders may consider an independent RICS Red Book valuation in specific circumstances. Always confirm with your lender or mortgage broker before commissioning an independent valuation for mortgage purposes.

How long does a property valuation take?

A standard residential valuation inspection typically takes 30 minutes to two hours depending on property size and complexity. Written reports are usually delivered within two to five working days. Probate and matrimonial valuations may take longer because of the detailed methodology statements required in the report.

Is an estate agent's valuation legally binding?

No. An estate agent's market appraisal is a commercial estimate to support pricing and marketing decisions. It carries no professional indemnity protection and is not accepted by lenders, HMRC, or courts as evidence of value. Only a RICS Registered Valuer can produce a report that carries professional liability and is accepted for formal legal or financial purposes.

Sources and further reading

- RICS Valuation — Global Standards (Red Book) — RICS

- Valuation Office Agency — GOV.UK

- Valuing the estate of someone who died — GOV.UK

- Leasehold and Freehold Reform Act 2024 — legislation.gov.uk

- Remortgaging your home — Citizens Advice

Useful next reads

Surveys & Inspections

Surveys & InspectionsLand Surveys and Boundary Measurement: Who Pays

There is no statutory rule in England and Wales that determines who pays for a boundary or land survey.

Surveys & Inspections

Surveys & InspectionsCCTV Drain Survey Costs and What to Expect

A CCTV drain survey in the UK typically costs between £150 and £400 for a standard residential survey covering one or two drainage runs.

Surveys & Inspections

Surveys & InspectionsStructural Building Survey Costs

A RICS Level 3 Building Survey typically costs £500–£1,500 in the UK, depending on property size, age, and location.

Surveys & Inspections

Surveys & InspectionsParty Wall Surveyor Fees and Professional Costs

A party wall surveyor typically charges £700–£1,500 for a straightforward agreed appointment in the UK.

Surveys & Inspections

Surveys & InspectionsUnderstanding Property Surveys: Types and When You Need Them

The three main RICS survey types are the Level 1 Condition Report (for standard properties in good condition), the Level 2 Home Survey (conventional homes in reasonable condition), and the Level 3 Building Survey (older, unusual, or defective properties).