Q4 Job Price Index: UK Service Pricing Trends and Market Analysis

By Housey · Last reviewed 19th of May 2026

Q4 Job Price Index: UK Service Pricing Trends and Market Analysis

The cost of getting work done on your home has shifted significantly over the past few years, and knowing what is driving those changes can mean the difference between a well-budgeted project and an expensive surprise. Whether you are planning a kitchen extension, rewiring an ageing Victorian terrace, or fitting a heat pump, the prices you are quoted today reflect broader forces in the UK construction economy — from material supply chains to trade skills shortages. Q4 in particular carries its own pricing character, as tradespeople weigh end-of-year demand against the seasonal slowdown in outdoor and groundworks activity.

Key points

- The ONS Construction Output Price Index (published quarterly on GOV.UK) tracks price movements across new build, repair and maintenance, and infrastructure — the repair and maintenance sub-index is most relevant for domestic improvements.

- BCIS (Building Cost Information Service), the RICS-affiliated data provider, publishes tender price indices and detailed labour and material sub-indices used by professional quantity surveyors to benchmark project costs.

- UK construction material prices rose sharply between 2020 and 2023 — timber, insulation, and cement prices increased by an estimated 20–30% in that period — and have since plateaued at elevated levels rather than returning to pre-2020 norms.

- The CITB Construction Skills Network consistently identifies labour shortages in electricians, plumbers, and specialist retrofit trades as a key upward pressure on wages and, consequently, on quoted day rates.

- Q4 price dynamics tend to be mixed: demand for indoor work (heating, electrical, kitchens) remains strong as the weather shifts, while outdoor projects (roofing, groundworks, landscaping) see reduced competition for bookings.

How UK home improvement prices are tracked

Homeowners rarely see price index data directly, but two sources underpin how professionals — surveyors, architects, and project managers — estimate and benchmark costs.

The ONS Construction Output Price Index is published on GOV.UK as part of the Construction Statistics release. It covers housing (new build and repair/maintenance separately), commercial, and infrastructure sectors. For most domestic renovation work, the "private housing repair and maintenance" sub-index is the most relevant signal.

The BCIS Tender Price Index is used by quantity surveyors to adjust historical cost data to current conditions. It factors in competitive pressure — how many firms are tendering for available work — as well as raw input costs. When contractors are busy, tender prices rise even if material costs remain stable, because competition for the work reduces.

Together, these indices explain why a builder's quote for the same specification can vary substantially between years, seasons, and economic conditions.

Material costs and supply chain dynamics

Several material categories have outsized influence on overall renovation budgets.

Material | Typical use | Post-2020 price trend | Position as of 2026 |

|---|---|---|---|

Structural timber | Stud walls, roofing, joists | Sharp rise 2020–2022, partial easing | Elevated vs pre-2020 baseline |

Rigid insulation boards | Solid wall, floor, flat-roof insulation | Significant increases driven by energy regulation demand | Remains high; sustained by Part L requirements |

Cement and aggregates | Groundworks, extensions, repairs | Moderate rise, broadly stabilised | Near pre-crisis levels in most regions |

Copper pipework | Plumbing, underfloor heating | Volatile, linked to global commodity markets | Subject to ongoing commodity price fluctuation |

PVC and plastics | Windows, guttering, drainage | Energy-cost-driven rises; some reversion | Mixed, tracks oil price movements |

Indicative trends based on ONS materials data and BCIS sub-indices. Individual supplier prices vary by region and volume.

Homeowners planning major works should ask builders to specify which materials are included in the quote and whether any price-volatility clauses apply for projects running beyond three months.

Labour costs and the skills shortage

Material prices attract the headlines, but labour typically accounts for 50–60% of a domestic renovation budget across most trade categories. The CITB Construction Skills Network reports identify persistent shortages in:

- Electricians — especially for EV charging installations, solar PV, and Electrical Installation Condition Report (EICR) remediation work.

- Plumbers and heating engineers — demand amplified by heat pump rollout under the Boiler Upgrade Scheme.

- Plasterers and dry-liners — interior finishing trades face limited apprenticeship pipelines.

- Specialist retrofit installers — demand for PAS 2035-compliant Retrofit Coordinators and installers continues to outpace supply.

Where demand outstrips supply, day rates rise. Homeowners in high-demand areas — London, the South East, and regions with concentrated retrofit activity — may see quotes 20–30% above the national mid-range.

Q4 seasonal patterns

Autumn and winter introduce predictable shifts in the home improvement market.

What tends to happen in Q4:

- Heating and HVAC work peaks. Boiler replacements, heat pump installations, and heating system upgrades see high demand as temperatures fall. Lead times extend and some engineers charge premium rates for urgent callouts.

- Outdoor work slows but does not stop. Groundworks and drainage projects are less attractive in cold, wet conditions, but roofing repairs, repointing, and external insulation projects continue when weather permits.

- Builders aim to close the books. Some contractors accept lower-margin work to keep crews employed through a quieter period; others hold rates firm and reduce available slots.

- Supply-chain pressure eases somewhat. Merchant stocks built up over summer reduce pressure on lead times for standard materials.

What this means for homeowners:

- If your project is time-sensitive (roof repair, heating failure), expect limited negotiating room in Q4.

- If your project can start in January, you may find more availability and competitive pricing in the post-Christmas lull.

- Kitchen and bathroom fit-outs often carry long supply-chain lead times for units and appliances — plan 10–16 weeks ahead.

Worked scenario: pricing a loft conversion across different market conditions

Consider a homeowner in Birmingham planning a 40 m² dormer loft conversion. Indicative UK costs (last reviewed 2026-05-19 — always obtain current quotes):

Market condition | Indicative price range | Key driver |

|---|---|---|

Competitive pre-pandemic market (2019 baseline) | £30,000–£42,000 | Lower material costs, more contractor competition |

2022 peak inflation environment | £45,000–£65,000 | Timber, steel, and labour all at cycle highs |

2025–26 stabilised-but-elevated market | £38,000–£55,000 | Materials off peak, labour market still tight |

Source: BCIS repair and maintenance cost data and published industry ranges. These are indicative ranges only — actual quotes depend on specification, access, structural complexity, and regional labour markets.

The scenario illustrates why a quote that looks expensive compared to a 2019 figure may in fact reflect genuine market conditions rather than overcharging.

Homeowner checklist: using price trends to budget effectively

When to get professional help

If your project is complex, involves listed building or conservation area constraints, or is valued above approximately £50,000, a professional cost consultant — typically an RICS-chartered quantity surveyor — can benchmark quotes against current BCIS data and identify outliers. For multi-trade works, a project manager or principal contractor arrangement may protect you from coordination-cost surprises that inflate final bills above the original estimates.

How Housey can help

Housey connects UK homeowners with vetted local service providers across a wide range of improvement and build services. Whether you are planning an extension, a loft conversion, or a heating upgrade, our marketplace helps you request multiple quotes, compare providers on a like-for-like basis, and make better-informed decisions based on current market conditions.

Frequently asked questions

How often does the ONS publish construction price data?

The ONS publishes Construction Statistics, including the Construction Output Price Index, on a quarterly basis, typically around 10–12 weeks after the reference quarter ends. The full dataset, including the private housing repair and maintenance sub-index, is freely available on GOV.UK under the Construction Statistics release. No subscription is required to access it.

Is BCIS data available to homeowners?

BCIS data is primarily a subscription service aimed at professionals — quantity surveyors, architects, and project managers. Some summary data is published through RICS channels and the industry press. For homeowners, comparative quote-getting remains the most practical proxy for understanding current market pricing conditions without a professional subscription.

Why do quotes for the same job vary so much?

Variation reflects differences in specification, material quality, overhead structure, geographic market conditions, and contractor workload. A significantly lower quote may reflect a different specification or compressed margins — always ask what is included and excluded before drawing conclusions about which quote represents fair value.

Should I time my project to avoid peak pricing?

For discretionary, non-urgent work, planning to start in January–March often finds more contractor availability and, in some cases, more competitive pricing as contractors fill the post-Christmas lull. This advantage is most pronounced for exterior and groundworks projects. Indoor trades — plumbing, electrical, and kitchen fitting — tend to remain busy year-round.

Sources and further reading

- ONS Construction Output Price Indices — Office for National Statistics

- BCIS Building Cost Information Service — RICS

- CITB Construction Skills Network Reports — CITB

- FMB State of Trade Survey — Federation of Master Builders

- Building Regulations Approved Documents — GOV.UK

Useful next reads

Improvement & Build

Improvement & BuildQ1 2026 Job Price Index: UK Service Pricing Trends and Market Analysis

UK trade and construction prices in Q1 2026 were shaped by elevated materials costs, a persistent skills shortage in specialist trades, and the April 2026 National Insurance increase for employers.

Improvement & Build

Improvement & BuildRising Material Costs and Impact on UK Home Improvement Projects

UK construction material prices remain above pre-2020 levels despite some easing from peak inflation.

Improvement & Build

Improvement & BuildQ1 2025 Home Improvement Trends: Market Data and Consumer Priorities

Q1 2025 saw UK homeowners prioritise loft conversions, energy efficiency upgrades, and kitchen extensions as build costs stabilised following the 2022–2023 peak and mortgage rates began to ease.

Improvement & Build

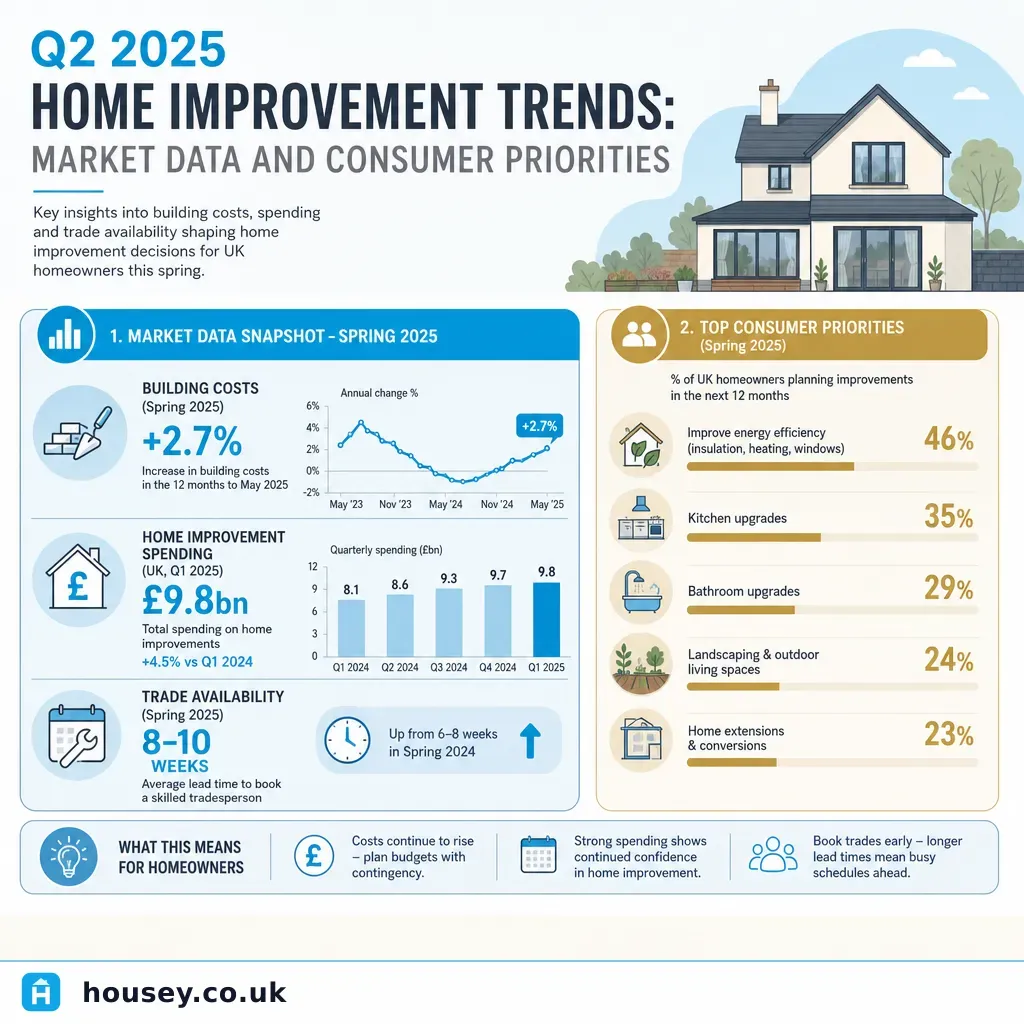

Improvement & BuildQ2 2025 Home Improvement Trends: Market Data and Consumer Priorities

In Q2 2025, kitchen refurbishments and bathroom renovations led UK consumer home improvement demand, followed by single-storey extensions and garden offices.

Improvement & Build

Improvement & BuildQ4 2025 Home Improvement Trends: Market Data and Consumer Priorities

In Q4 2025, UK homeowners prioritised heating upgrades, insulation, and kitchen refurbishments as temperatures fell.