Renoflation: Understanding Rising Renovation Costs and Market Drivers

By Housey · Last reviewed 19th of May 2026

Renoflation: Understanding Rising Renovation Costs and Market Drivers

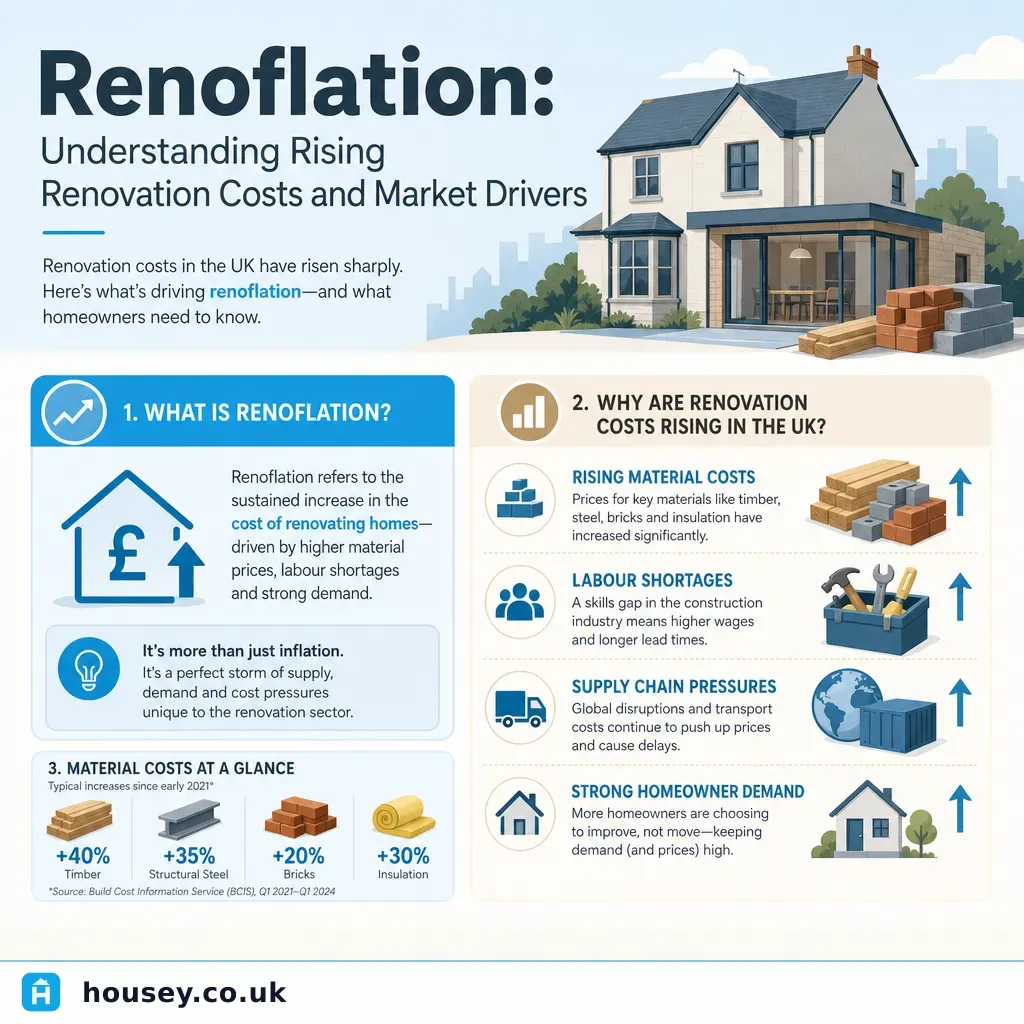

Planning a home improvement project in 2026 means confronting a market where the prices you would have paid five years ago can feel like a different era. Renovation costs in the UK have risen substantially since 2020, driven by a combination of forces that affect materials, labour, and demand simultaneously — and at rates that frequently outpace general consumer price inflation. Understanding these dynamics helps you set a realistic budget, negotiate with greater confidence, and identify when a quote reflects genuine market conditions rather than an overcharge.

Key points

- Construction material prices in the UK rose an estimated 20–30% between 2020 and 2023, according to ONS materials price index data; many categories remain elevated above pre-2020 levels despite easing from their peaks.

- Labour costs account for 50–60% of most domestic renovation budgets and continue to rise as the CITB reports persistent annual shortfalls of approximately 50,000 workers across the UK construction sector.

- "Renoflation" compounds differently from general CPI inflation: materials and labour price rises apply in parallel, amplifying overall project cost increases beyond what any single inflation measure captures.

- VAT at 20% applies to most home improvement work carried out by VAT-registered contractors — a cost that rises proportionally as base prices increase, magnifying the headline impact on total project spend.

- Post-pandemic demand surges and the retrofit push under programmes such as ECO4 and the Boiler Upgrade Scheme have added structural demand pressure on top of underlying input cost rises.

What is renoflation?

"Renoflation" is an informal term for the above-general-inflation rise in home renovation and improvement costs documented across the UK and other developed markets since 2020. It is not an official statistic or published index, but a description of a compounding market phenomenon.

Where general CPI captures the average price of a broad basket of goods and services, renovation costs are concentrated in categories — construction materials, trade labour, and energy — that all moved sharply in the same direction at the same time. That simultaneity is the distinguishing feature: in most economic cycles, labour or materials may rise, but rarely both at once and rarely at sustained double-digit annual rates.

The main cost drivers

Construction materials

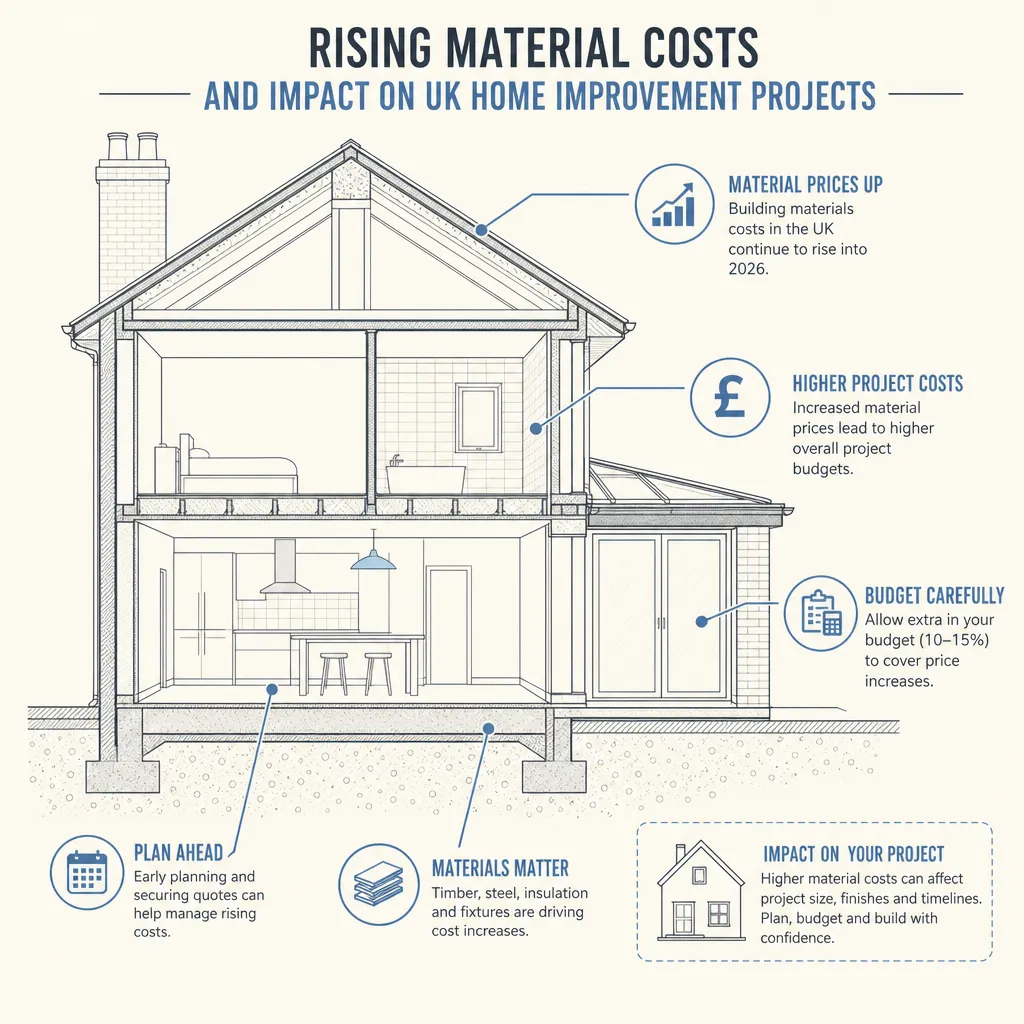

The timber shortage of 2020–2022 was the first highly visible signal. Global supply disruption, pandemic-driven demand for DIY and new build, and logistics constraints drove softwood timber prices in the UK up significantly from historical ranges. Structural steel, cement, and insulation products followed similar patterns.

By 2023–24, most material categories had eased from their peaks, but easing from a peak is not the same as returning to previous levels. Homeowners comparing a 2026 quote to a 2019 estimate will find a step-change in many material categories that has not unwound.

Trade labour

The Construction Industry Training Board (CITB) estimates that the UK construction sector needs to recruit around 50,000 workers per year to meet demand. Structural shortfalls in electricians, plumbers, roofers, and specialist retrofit trades persist. The consequences:

- Day rates for skilled tradespeople have risen materially, particularly in high-demand regions such as London and the South East.

- Lead times extend when tradespeople are busy — booking slots eight to twelve weeks out is now common for many trades.

- Contractors can be more selective about projects, reducing competitive price pressure in their favour.

Energy and overhead costs

The energy price crisis of 2021–23 raised the operating costs of builders' merchants, manufacturing facilities, transport, and plant. While wholesale energy prices have fallen from their peaks, elevated grid tariffs have fed through into product prices and business overheads that contractors must recover in their quoted rates.

Government retrofit demand

Programmes including ECO4, the Boiler Upgrade Scheme (BUS), and the Great British Insulation Scheme have injected substantial demand into insulation, heat pump, and heating system trades. This has been broadly positive for decarbonisation goals but adds demand pressure on trades that were already stretched by the wider renovation market.

How renoflation affects different project types

Project type | Typical material share | Typical labour share | Relative renoflation impact |

|---|---|---|---|

Loft conversion (timber-frame dormer) | 40–50% | 50–60% | High — timber and skilled labour both rose sharply |

Kitchen replacement (supply and fit) | 50–65% | 35–50% | Moderate to high — supply costs vary widely by specification |

Boiler replacement | 50–60% (appliance) | 40–50% | High demand pressure amplified by BUS subsidy scheme |

Rewiring and EICR remediation | 25–35% | 65–75% | Dominated by labour costs — electrician day rates are the key driver |

External wall insulation | 45–55% | 45–55% | Double pressure from insulation material costs and retrofit demand |

Painting and decorating | 20–30% | 70–80% | Largely labour-driven; material cost impact is lower than most trades |

Shares are indicative; actual splits depend on specification, location, and project scale.

Red flags: genuine market pricing vs overcharging

Renoflation creates a real challenge: legitimate market prices are higher than before, making it harder to distinguish a fair quote from an inflated one. These signs suggest a quote warrants closer scrutiny:

- Price significantly above two comparable quotes for the same specification. A 10–15% premium may reflect experience or quality; 30–50% above average without a clear explanation is a red flag.

- No written quote or specification. Verbal pricing only, with no line-item breakdown, makes meaningful comparison impossible.

- Pressure to commit immediately. Reputable tradespeople quote and wait; high-pressure tactics frequently signal exploitation of the perceived scarcity of tradespeople.

- Demand for a very large cash upfront payment. A deposit of 10–25% is standard for larger projects; demands for full or near-full cash payment before work starts are a warning sign.

- No public liability insurance or accreditation evidence provided on request. Legitimate professionals can produce these promptly.

Worked scenario: budgeting a bathroom renovation in Sheffield

A homeowner in Sheffield plans a full bathroom renovation in a 1970s semi-detached house — removing and replacing the suite, tiling, and plumbing connections. Indicative UK costs (last reviewed 2026-05-19 — always obtain current quotes for your specific property and specification):

Market scenario | Specification | Indicative total range |

|---|---|---|

2019 (pre-pandemic baseline) | Mid-range suite, standard tiles, local plumber | £5,000–£8,000 |

2022 (peak renoflation) | Same specification | £8,000–£13,000 |

2025–26 (stabilised-but-elevated) | Same specification | £7,000–£11,000 |

Source: BCIS maintenance and repair cost data and published industry survey ranges. Costs depend on specification, property access, and local market conditions.

The scenario illustrates that costs remain materially above pre-2020 levels despite easing from the 2022 peak — a pattern broadly consistent across most domestic project types.

How to protect your renovation budget

- Get at least three detailed, written quotes for the same specification — not ballpark figures or verbal estimates.

- Ask whether prices are fixed or subject to material variation, and how long the quote remains valid.

- Stage larger projects where possible — completing one phase and allowing the market to settle before proceeding can reduce exposure to mid-build cost increases.

- Use a quantity surveyor for projects above approximately £30,000 to benchmark quotes against current BCIS data.

- Include a 10–15% contingency in your budget — 15–20% for older properties or any project involving existing structure.

- Avoid peak booking windows (typically April–September) for flexible projects; January–March usually offers more availability and can yield modest savings.

When to get professional help

For projects above approximately £30,000, or for complex multi-trade works, an RICS-chartered quantity surveyor can provide independent cost benchmarking against current BCIS data. This is especially valuable when quotes vary significantly — a surveyor can identify specification differences that explain apparent discrepancies, or confirm that prices are genuinely out of line with prevailing market rates.

How Housey can help

Housey connects UK homeowners with vetted local service providers across improvement, build, and energy retrofit categories. Requesting multiple quotes through our platform and comparing providers on a like-for-like basis is a practical tool for navigating a market where cost variation is real, and where the difference between the right quote and the wrong one can be significant.

Frequently asked questions

What is renoflation?

Renoflation is an informal term describing the above-general-inflation rise in home renovation costs, driven by simultaneous increases in construction material prices, trade labour rates, and demand. It has been particularly marked in the UK since 2020 and reflects structural factors — labour shortages, retrofit demand, and material supply adjustments — that are unlikely to reverse fully in the short term.

How much have UK renovation costs risen since 2020?

ONS materials price indices show many key construction materials rose 20–30% between 2020 and 2023. Labour cost increases are consistently reported in CITB and FMB surveys, particularly for trades in shortage. Overall project costs for common renovation types rose broadly 30–50% at the 2022 peak, with some moderation since, though prices remain well above pre-2020 levels.

Will renovation costs come down in 2026?

Most industry commentary suggests costs will stabilise at elevated levels rather than returning to pre-2020 norms. Material prices have eased from peak in most categories, but the labour shortage is structural and unlikely to resolve quickly. Sustained demand from energy retrofit programmes adds further upward pressure on specialist trades such as heat pump engineers and retrofit coordinators.

Should I delay my project to wait for lower prices?

For most homeowners, indefinite delay is unlikely to yield meaningfully lower prices — the structural cost drivers are not reversing quickly. If your project is urgent due to safety, regulatory compliance, or deteriorating structure, delay carries real costs. For discretionary work, timing the start for a quieter booking window (January–March) may yield modest savings without an open-ended wait.

Sources and further reading

- ONS Construction Statistics — Office for National Statistics

- CITB Construction Skills Network Reports — CITB

- FMB State of Trade Survey — Federation of Master Builders

- BCIS Building Cost Information Service — RICS

- Boiler Upgrade Scheme guidance — GOV.UK

- ECO4 Energy Company Obligation scheme — GOV.UK

Useful next reads

Improvement & Build

Improvement & BuildRising Material Costs and Impact on UK Home Improvement Projects

UK construction material prices remain above pre-2020 levels despite some easing from peak inflation.

Improvement & Build

Improvement & BuildRental Property Improvements: Investment Decisions and ROI Planning

Prioritise compliance-driven improvements first — a minimum EPC rating of E (with C proposed for new tenancies), annual Gas Safety Certificate, EICR every five years, and smoke and CO alarms on every storey.

Improvement & Build

Improvement & BuildComparing Refurbishment Investment Against New Build Viability

Whether refurbishment or new build is the better investment depends on the existing structure's condition, planning context, build costs, and your end goal.

Improvement & Build

Improvement & BuildStrategic Home Improvements That Enhance Property Value

The home improvements most likely to add value in the UK are loft conversions (typically 10–20%), rear extensions (5–15%), and updated kitchens and bathrooms.

Improvement & Build

Improvement & BuildRenovating a Repossessed Property: Strategic Planning and Assessment

Repossessed properties are sold by the lender with no obligation to provide seller disclosure or property information forms.