Understanding rental property valuation: what to expect when agents assess your home

By Housey · Last reviewed 7th of May 2026

Understanding rental property valuation: what to expect when agents assess your home

Most landlords encounter a rental valuation when they are about to let a property for the first time, switch letting agents, or reassess rental income after a refurbishment. The figure an agent arrives at directly shapes yield calculations, buy-to-let mortgage affordability assessments, and negotiating positions with tenants — so understanding how that number is reached matters more than many landlords realise.

Key points

- A rental valuation (sometimes called a lettings appraisal) is not a formal RICS valuation; it is an agent's informed estimate of market rent and carries no regulatory weight for mortgage lending or legal proceedings.

- The Valuation Office Agency (VOA) sets Local Housing Allowance (LHA) rates by Broad Rental Market Area (BRMA), determining the maximum housing cost claimable by Housing Benefit and Universal Credit tenants in the private rented sector.

- Landlords in England and Wales must hold a minimum EPC rating of E to let a property lawfully; since April 2021, all private rented properties in England must also have a valid Electrical Installation Condition Report (EICR) from a qualified electrician.

- Gross rental yield = annual rent ÷ property value × 100; UK gross yields typically range from 3–9% depending on location and property type (indicative UK figures, last reviewed 2026-05-07).

- Rental valuations from different agents for the same property can legitimately differ by 10–20%, making comparative appraisals essential before setting an asking rent.

What a rental valuation is — and what it is not

A rental valuation from a lettings agent is a market appraisal, not a formal RICS Red Book valuation. The agent is applying knowledge of comparable properties let recently in the local market, combined with an assessment of your property's specific characteristics: size, condition, location, parking, energy performance, and furnished or unfurnished status.

This means:

- The figure can vary between agents, sometimes significantly.

- It is not legally binding on you or a prospective tenant.

- It cannot be used for mortgage lending purposes — buy-to-let lenders require a formal RICS valuation from a registered valuer.

- It may be influenced by an agent's desire to win your instruction, so getting two or three appraisals is standard practice before committing to a letting agent.

How agents assess your property

When a lettings agent visits to appraise your property, they will typically consider the following factors:

Factor | What the agent examines | Why it matters |

|---|---|---|

Location and postcode | Proximity to transport, schools, amenities, and employment centres | Drives tenant demand and sets the market rent ceiling |

Property size and layout | Bedrooms, bathrooms, reception rooms, total floor area | Sets the baseline for comparable properties |

Condition and presentation | Decoration, fixtures, appliances, structural condition | Affects speed of let and achievable rent |

EPC rating | Energy efficiency certificate band (A–G) | Legal minimum E; tenants increasingly factor running costs |

Furnished vs unfurnished | White goods and furniture provision | Affects target tenant profile and achievable rent |

Parking and outdoor space | Off-street parking, garden, terrace | Commands a premium in urban areas |

Current local competition | Active comparable listings, typical void periods | Calibrates achievable vs aspirational rent |

Regulatory compliance | Gas Safety Certificate, EICR, smoke and CO alarms | Non-compliance prevents lawful letting |

The rental valuation process: step by step

Before the agent visits: document preparation list

During the visit

The agent will walk through each room, assess condition and presentation, note approximate dimensions, and discuss your situation: intended tenancy type, furnished or unfurnished preference, your target tenant profile, and your availability timeline. This conversation shapes the final figure as much as the property's physical characteristics.

After the visit

You should receive a written appraisal document setting out the recommended monthly rent, indicative yield calculation, comparable properties used as a reference, suggested management fee structure, estimated void period risk, and any recommended works before marketing. If an agent provides only a verbal figure without written comparables or reasoning, treat that appraisal with caution.

Which type of rental assessment do you need?

- Get a standard lettings appraisal if you want to understand achievable market rent before deciding whether to let, switch agents, or refinance.

- Commission a formal RICS rental valuation if you need the figure for mortgage purposes (a buy-to-let remortgage or portfolio financing), court proceedings, divorce proceedings, or formal business accounting.

- Contact the Valuation Office Agency (VOA) if you are letting to Housing Benefit or Universal Credit claimants and need to understand the applicable Local Housing Allowance rate for your BRMA.

- Speak to a specialist surveyor if the property has unusual characteristics — listed building, non-standard construction, HMO, or mixed-use — that a standard agent appraisal may not accurately capture.

- Ask a specialist property solicitor if you are unsure about your legal obligations as a landlord before setting a rent or instructing an agent.

Why rental valuations vary between agents

It is common to receive appraisals that differ by 10–20% from different agents for the same property. Reasons include:

- Different comparable evidence. Not all agents track the same data; some use Rightmove asking prices rather than achieved rents.

- Different management propositions. An agent pitching a managed service at 12–15% may quote a higher headline rent to offset the fee perception in the landlord's mind.

- Local market knowledge gaps. National chains may have less granular data for specific roads or postcodes than independent local agents.

- Aspirational vs achievable rent. Some agents inflate the initial figure to win the instruction, expecting to advise a price reduction after a slow marketing period.

A useful cross-check: look at current active Rightmove and Zoopla listings for similar properties in the postcode and note both asking rent and time on market.

Important limitations

This article provides general information about the rental valuation process in England. Rules, fee structures, regulatory requirements, and market conditions vary by location, property type, and tenancy structure. Scotland, Wales, and Northern Ireland operate under different regulatory regimes — Scotland's private rented sector is governed by the Private Housing (Tenancies) (Scotland) Act 2016, which sets distinct requirements and rent review processes.

Nothing in this article constitutes formal valuation advice, investment advice, or legal guidance. Landlords with complex portfolios, HMO properties, leasehold properties, or properties let under non-standard tenancy arrangements should seek specialist advice from a RICS-registered valuer or a property solicitor before acting.

What to ask a qualified professional

Before instructing a lettings agent or commissioning a formal valuation, ask:

- Are you a member of a recognised professional body such as ARLA Propertymark, RICS, NAEA Propertymark, or UKALA?

- Can you provide evidence of comparable properties let and achieved in the last three months — not just asking prices from property portals?

- What is the basis of your valuation: gross yield, net yield, or comparable rent?

- For a formal RICS valuation: what is your RICS registration number, and which basis of value will you use (Market Rent or Estimated Rental Value)?

- What regulatory compliance checks do you carry out before recommending a rent level?

- How do you handle rent review requests from tenants, and what is your typical void period for properties similar to mine?

When to get professional help

A standard lettings agent appraisal is sufficient for most straightforward decisions about whether and at what rent to let a property. You should seek a formal RICS valuation or specialist advice if:

- You are refinancing against rental income and your lender requires a professional valuation

- The property qualifies as an HMO, which has specific licensing and regulatory requirements

- You are involved in a dispute, court proceeding, or divorce where rental income or property value is at issue

- The property is subject to rent control provisions (currently applicable in Scotland)

- The property is a listed building or has unusual construction affecting insurability and compliance

How Housey can help

Housey connects landlords with qualified professionals for both lettings appraisals and formal property assessments. Explore valuation surveys to find RICS-registered valuers who can provide a formal assessment for mortgage or legal purposes, or review insurance valuations if you need a reinstatement cost assessment alongside your rental appraisal.

Frequently asked questions

Is a rental valuation from an agent the same as a RICS valuation?

No. A lettings agent's appraisal is an informal market estimate used to set asking rent. A formal RICS valuation is carried out by a registered valuer under RICS Red Book standards and can be used for mortgage applications, legal proceedings, and formal accounting purposes. Only a RICS-qualified valuer can produce the latter, and the two documents serve entirely different purposes.

How often should I get my rental property revalued?

Most landlords review rental levels annually, typically before a tenancy renewal or at a break clause. In a rapidly changing local market, a mid-tenancy appraisal can help you understand whether your rent has drifted significantly below market. Changes to local amenities, transport links, or nearby development often shift comparable rents quickly.

Can a landlord challenge a Local Housing Allowance rate?

LHA rates are set annually by the Valuation Office Agency based on the 30th percentile of market rents for private lets in each Broad Rental Market Area. Individual landlords cannot challenge a BRMA rate directly, but if you believe your property's BRMA designation is incorrect, you can contact the VOA to clarify the correct area.

What compliance checks are required before letting a property in England?

Minimum requirements before a tenancy begins include: a valid EPC (minimum E rating), a Gas Safety Certificate if gas appliances are present, an EICR issued within the last five years, working smoke alarms on every floor, and a carbon monoxide alarm in rooms with solid fuel appliances. Landlords must also conduct Right to Rent checks and register deposits with an approved scheme. Requirements differ in Scotland, Wales, and Northern Ireland.

Sources and further reading

- Private renting for landlords: legal obligations — GOV.UK

- Local Housing Allowance rates — GOV.UK / Valuation Office Agency

- RICS Red Book: Global Standards — RICS

- Electrical safety standards in the private rented sector — GOV.UK

- ARLA Propertymark landlord guidance — Propertymark

- Check how to rent: England — GOV.UK

Useful next reads

Surveys & Inspections

Surveys & InspectionsUnderstanding and addressing bowed or bulging walls in your property

A bowed or bulging wall may indicate wall tie failure, foundation movement, or overloading.

Surveys & Inspections

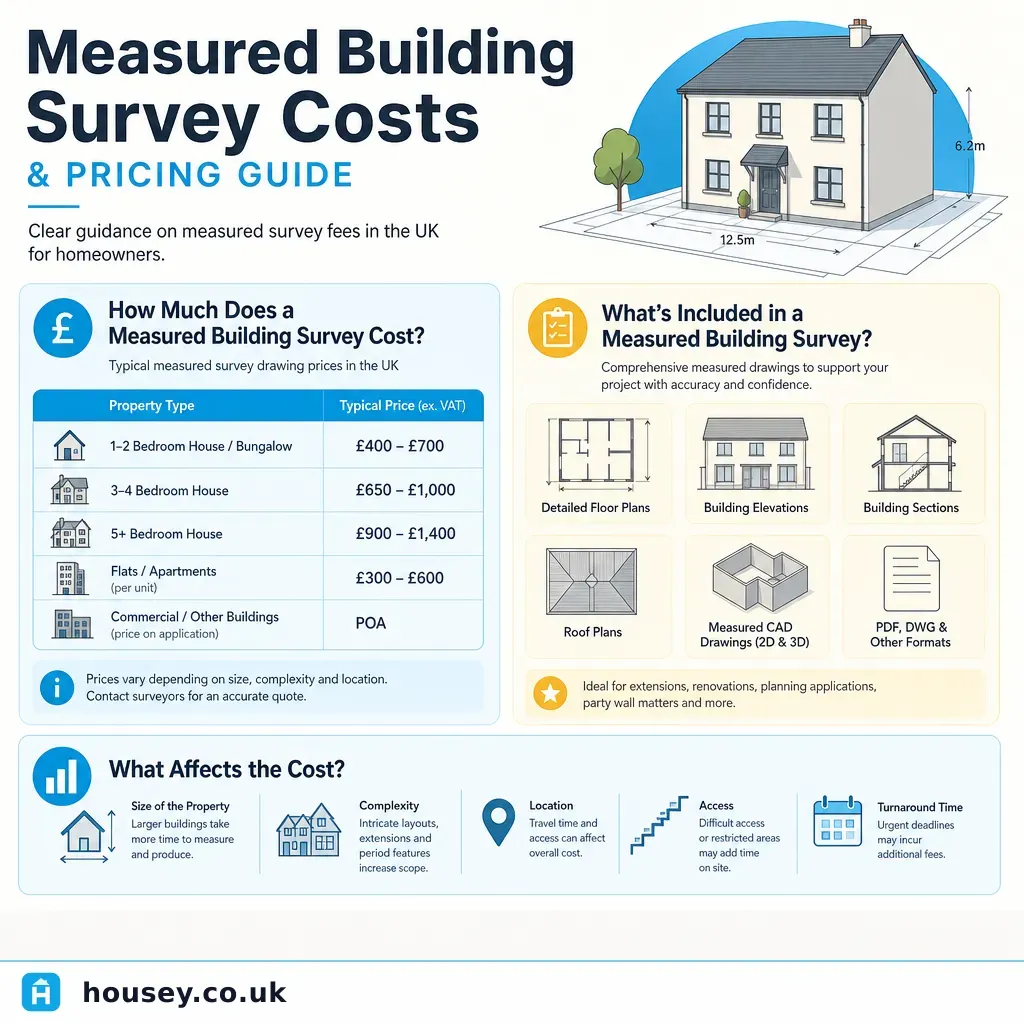

Surveys & InspectionsMeasured Building Survey Costs and Pricing Guide

A measured building survey in the UK typically costs between £500 and £5,000 for residential properties, depending on floor area, number of levels, drawing scope, and survey method.

Surveys & Inspections

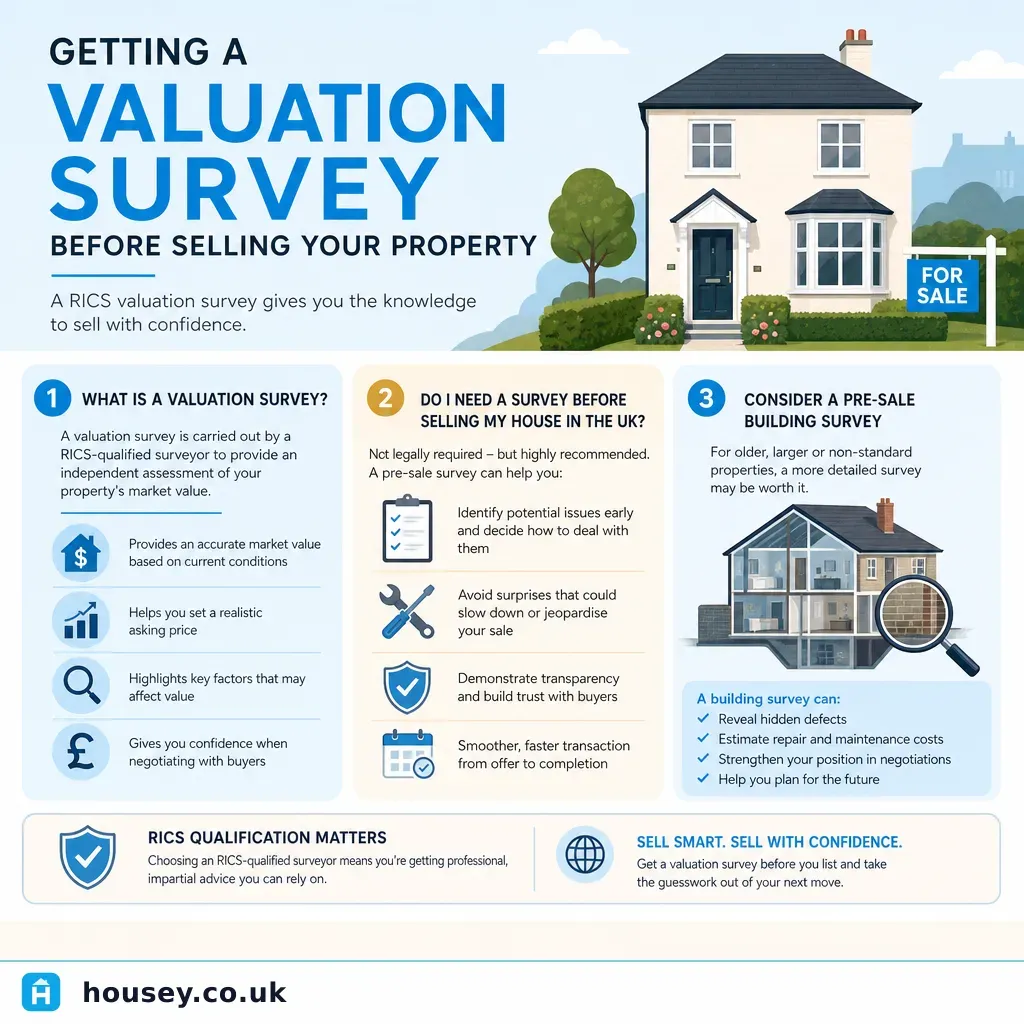

Surveys & InspectionsGetting a Valuation Survey Before Selling Your Property

Before selling, a free estate agent appraisal gives a market price guide, but only a RICS Red Book valuation carries formal professional standards and legal weight.

Surveys & Inspections

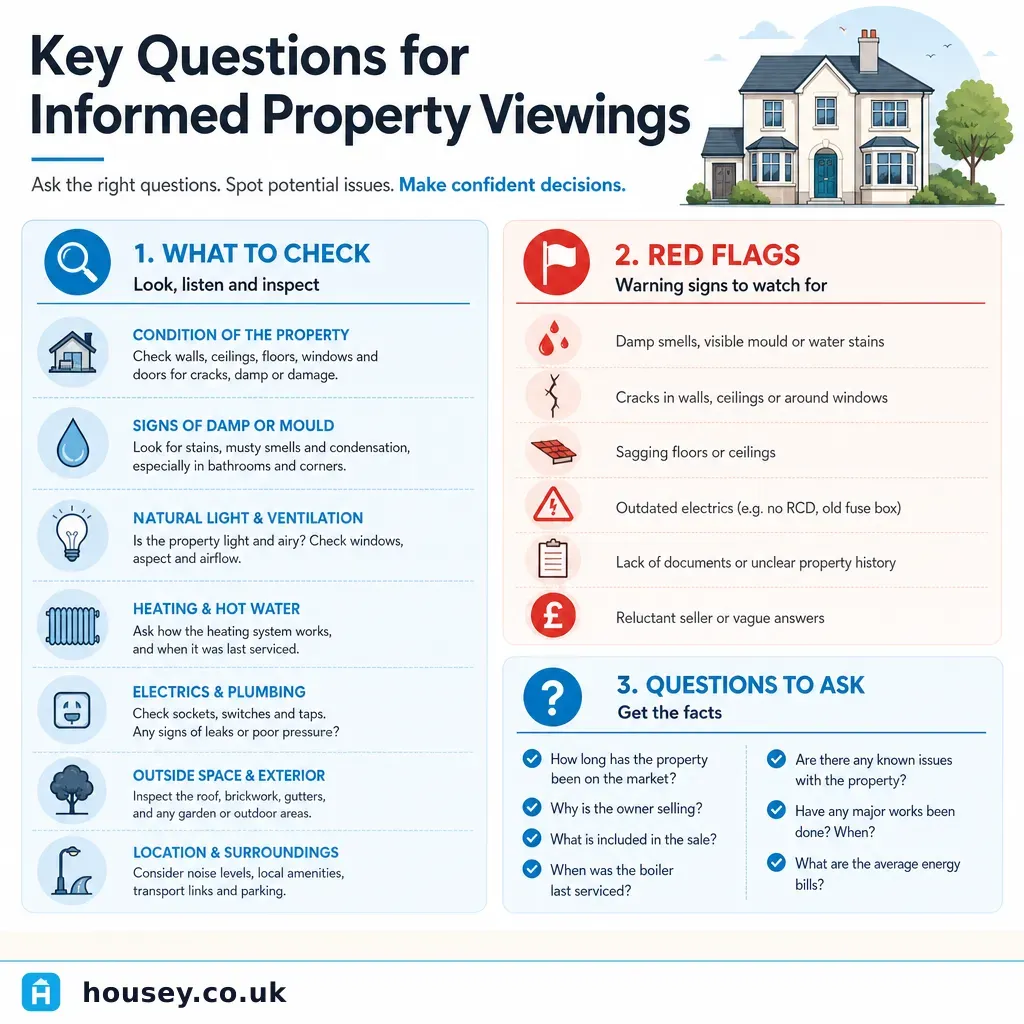

Surveys & InspectionsKey Questions for Informed Property Viewings

At a property viewing, ask specifically about structural movement, damp or water ingress, the age and service history of the boiler and electrics, whether any extensions obtained building regulations sign-off, and the seller's chain position.

Surveys & Inspections

Surveys & InspectionsProperty Valuation Survey: Understanding Market Worth and Cost Assessment

A property valuation survey establishes a property's market value at a specific date.