Should You Proceed Without a Formal Survey? Risks and Implications

By Housey · Last reviewed 11th of May 2026

Should You Proceed Without a Formal Survey? Risks and Implications

The decision to skip a property survey is one many buyers face under pressure — tight exchange timelines, competitive markets, or a belief that a mortgage valuation covers the same ground. In England and Wales, there is no legal requirement to obtain an independent survey before exchanging contracts, which means the financial and structural risk of any undisclosed defects passes entirely to the buyer the moment exchange takes place.

Key points

- A mortgage lender's valuation is not a survey — it checks the property is adequate security for the loan, usually without a detailed inspection of condition, and produces no buyer-facing condition report.

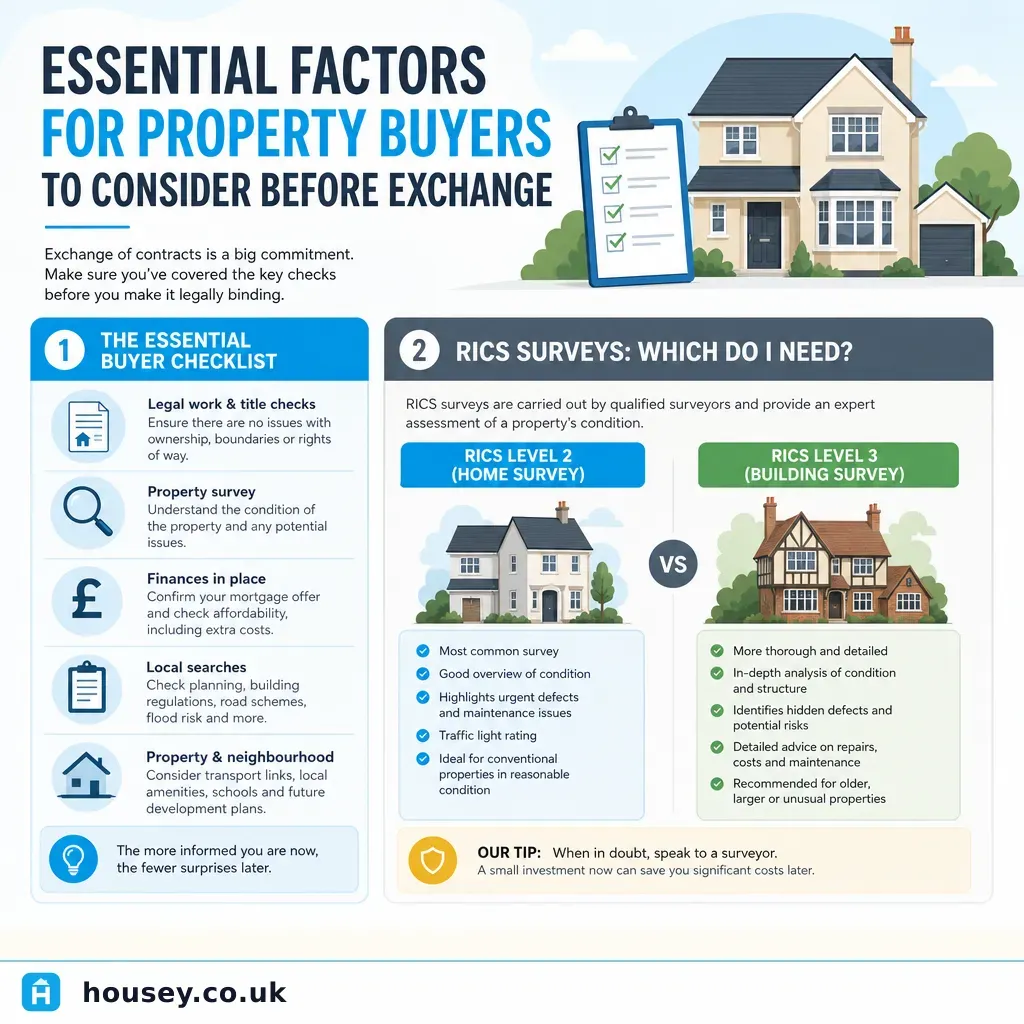

- RICS Home Surveys are available at three levels: Level 1 (Condition Report), Level 2 (Home Survey with traffic-light ratings), and Level 3 (Building Survey, the most detailed, suited to older or complex properties).

- In England and Wales, residential property is sold under caveat emptor — the buyer bears responsibility for defects that a reasonable pre-exchange inspection would have identified.

- A RICS Level 3 Building Survey typically costs £600–£1,500 for most residential properties depending on size and location — a fraction of the cost of typical major defect repairs. Indicative UK costs, last reviewed 2026-05-11.

- Leasehold buyers face risks beyond physical condition — including pending major works, service charge arrears, and lease length issues — that a mortgage valuation will not identify.

What a mortgage valuation does (and does not) cover

When your mortgage lender instructs a valuation, they are acting in their own interest — confirming the property is worth enough to secure their loan. The lender's valuation:

- Is often a brief desktop assessment or drive-by check for standard modern properties.

- May involve a short internal visit but does not systematically inspect condition.

- Typically does not produce a detailed report for the buyer, though some lenders share a summary copy.

- Does not identify damp, structural movement, timber defects, electrical condition, roof condition, or drainage issues.

- Makes no recommendations for specialist investigations or repairs.

Treating a mortgage valuation as a substitute for an independent survey is one of the most common and costly mistakes buyers make.

The principle of caveat emptor in English property law

In England and Wales, residential property is sold under caveat emptor — the buyer must beware. Sellers are not generally obliged to volunteer information about defects they have not been specifically asked about, though they must answer the standard TA6 property information form honestly and must not actively misrepresent. This places a clear obligation on the buyer to investigate before exchange.

Scotland operates differently: sellers must commission a Home Report (comprising a single survey, property questionnaire, and EPC) before marketing. This does not remove the value of a buyer-side independent survey, but it changes the information landscape at the point of offer.

In Northern Ireland, no equivalent to the Scottish Home Report exists, and caveat emptor principles apply as in England and Wales.

Which survey level should you choose?

- Choose a RICS Level 1 Condition Report if: the property is a modern new-build in good condition and you want a basic summary of accessible elements; note this is the most limited level of inspection.

- Choose a RICS Level 2 Home Survey if: the property is a conventional house or flat built after approximately 1900, appears to be in reasonable condition, and you want traffic-light condition ratings and maintenance recommendations.

- Choose a RICS Level 3 Building Survey if: the property is pre-1900, has visible defects, has been heavily altered, is of non-standard construction (timber frame, prefabricated, thatched, concrete panel), or is listed.

- Commission a structural survey in addition to or instead of a general survey if: there are visible cracks, signs of subsidence, evidence of underpinning, or significant structural alterations you want assessed in detail.

- Consider waiving a formal survey only if: you are an experienced investor purchasing at auction who has carried out a thorough pre-auction inspection and explicitly accepts the full risk of unknown defects — this is an unusual exception, not a general recommendation.

Red flags that make skipping a survey particularly risky

These property characteristics markedly increase the probability of significant undisclosed defects:

- Pre-1919 construction: solid walls, original roof structures, and buried drainage can conceal expensive defects invisible without specialist inspection.

- Visible cracking: stepped cracking in brickwork, diagonal cracks above door or window frames, or cracks wider than approximately 5 mm may indicate structural movement.

- Signs of damp: tide marks on walls, blown plaster, musty smell, or recently repainted patches in unusual locations.

- Altered layout: removed walls (particularly common in Victorian terraces), loft conversions, and extensions all carry potential structural and building control implications.

- Flat roofs: more prone to failure than pitched roofs; a surveyor can assess remaining service life.

- Non-standard construction: Wimpey no-fines, Airey houses, BISF steel frame, and similar types raise mortgage and insurance implications and require specialist assessment.

- Short leasehold: a lease below 80 years is approaching the point at which statutory extension costs increase significantly; below 70 years, many lenders will decline to lend.

- Flood risk: check the Environment Agency flood risk map before proceeding; a mortgage valuation will not assess insurance implications.

- Disclosed insurance claims: previous claims for subsidence, flooding, or fire markedly increase the risk of unresolved underlying defects.

What does skipping a survey actually cost?

There is no single reliable national figure for post-purchase repair costs where surveys were waived, but common categories of major unexpected defect include:

- Roof replacement: £5,000–£15,000+ depending on size and covering type.

- Damp and timber treatment: £1,000–£10,000+ depending on extent and cause.

- Underpinning for subsidence: £10,000–£30,000+.

- Full rewire: £3,000–£10,000+ for a typical house.

- Drain repairs or relining: £1,000–£20,000+ depending on whether drainage is shared or adopted.

Indicative UK cost ranges, last reviewed 2026-05-11. Actual costs depend on property size, location, defect extent, and contractor rates.

A RICS Level 2 survey typically costs £400–£900 for most residential properties; a Level 3 survey £600–£1,500. These figures are indicative, last reviewed 2026-05-11; request quotes for your specific property. The cost comparison with potential repair bills is stark.

Important limitations

This article provides general guidance on the risks of proceeding without a survey in the UK property market. It does not constitute legal or financial advice and should not be treated as a substitute for professional assessment. Property condition varies enormously between individual buildings. The appropriate level of survey for a specific property should be determined by a qualified RICS-regulated surveyor who has inspected it in person. Conveyancing and property law in Scotland and Northern Ireland differ from England and Wales.

What to ask a qualified professional

Before instructing a surveyor, ask:

- What survey level do you recommend for this property, and why?

- What are the most significant risks for this type and age of construction?

- If you identify concerning indicators during a Level 2 inspection, will you recommend specialist investigations?

- Will the report include indicative repair cost estimates, or condition ratings only?

- Are you RICS-regulated, and what professional indemnity insurance do you carry?

- How long will the report take to produce, and will it be ready before my exchange deadline?

- Will you personally carry out the inspection?

When to get professional help

Always seek a RICS-regulated surveyor before exchanging contracts on any residential property. Waiving an inspection entirely is a significant financial risk in most circumstances.

Contact a professional before proceeding if any of the following apply:

- Visible structural cracks or signs of movement are present in the property.

- Japanese knotweed has been disclosed or is visible within or adjacent to the boundary.

- The construction type is non-standard or has been flagged as a concern by your mortgage lender.

- The lease length is below 80 years.

- Previous insurance claims for subsidence, flooding, or fire have been disclosed on the TA6.

- Your solicitor or conveyancer has flagged unusual title, boundary, or planning issues.

If you have already exchanged without a survey and subsequently discover a significant defect, speak to a solicitor promptly about whether any misrepresentation occurred on the TA6 or in pre-contract enquiries, as limitation periods apply.

How Housey can help

Housey connects buyers with RICS-regulated surveyors across the UK. Whether you need a RICS Level 2 Home Survey for a standard residential property, a RICS Level 3 Building Survey for an older or more complex home, or a structural survey where specific defects are already visible, you can compare quotes from qualified professionals through RICS Home Surveys on Housey.

Frequently asked questions

Is a survey a legal requirement when buying a house in the UK?

No. In England and Wales there is no legal requirement to obtain an independent survey before exchange. However, caveat emptor applies — the buyer accepts responsibility for defects not disclosed by the seller. In Scotland, the seller must provide a Home Report including a single survey before marketing, though buyers may still commission their own survey independently.

Can I rely on the mortgage lender's valuation instead of a survey?

No. A mortgage valuation confirms the property is adequate security for the lender's loan; it does not inspect condition and does not produce a detailed report for the buyer. It will not identify structural defects, damp, timber decay, roof condition, or drainage issues. It should never be treated as a substitute for an independent survey.

What is the difference between a RICS Level 2 and Level 3 survey?

A RICS Level 2 Home Survey provides traffic-light condition ratings for accessible elements and suits conventional properties in reasonable condition. A RICS Level 3 Building Survey provides more detailed descriptions of construction, condition, and defects, and is more appropriate for older, larger, altered, or non-standard properties. Your surveyor can advise which level is appropriate for the specific property.

Can I recover costs from the seller if problems emerge after completion?

Generally no. In England and Wales, residential sales operate under caveat emptor. The main exception is if the seller made a material misrepresentation on the TA6 property information form or in direct pre-contract enquiries. If you believe misrepresentation occurred, speak to a solicitor promptly as limitation periods apply.

Sources and further reading

- RICS Home Survey Standard — RICS

- Buying or selling your home — GOV.UK

- Leasehold Advisory Service: buying a leasehold property — Leasehold Advisory Service

- Check flood risk for a property — GOV.UK / Environment Agency

- Citizens Advice: surveys and valuations when buying a home — Citizens Advice

Useful next reads

Surveys & Inspections

Surveys & InspectionsHow Professional Home Surveys Deliver Real Value For Buyers

A professional home survey by a RICS-registered surveyor can identify defects, legal compliance gaps, and cost liabilities before exchange of contracts, giving buyers an evidence base for negotiation or withdrawal.

Surveys & Inspections

Surveys & InspectionsUnderstanding Property Surveys: Types and When You Need Them

The three main RICS survey types are the Level 1 Condition Report (for standard properties in good condition), the Level 2 Home Survey (conventional homes in reasonable condition), and the Level 3 Building Survey (older, unusual, or defective properties).

Surveys & Inspections

Surveys & InspectionsWind Mitigation Inspection: How to Protect Your UK Home from Storm Damage

The UK has no formal wind mitigation inspection scheme, but a RICS Level 3 survey or specialist roof inspection assesses the same storm resilience factors.

Surveys & Inspections

Surveys & InspectionsEssential Factors for Property Buyers to Consider Before Exchange

Before exchanging contracts on a UK property, buyers should commission an appropriate RICS survey, review the property's legal title and search results, check the planning history, assess structural condition, and confirm the EPC rating.

Surveys & Inspections

Surveys & InspectionsSafe Property Viewing Practices: Protecting Yourself During Inspections

When viewing a property in the UK, always tell someone where you are going and share the full address before you leave.