Transferring Property Ownership: Legal Mechanisms and Requirements

By Housey · Last reviewed 25th of May 2026

Transferring Property Ownership: Legal Mechanisms and Requirements

Changing who legally owns a property in England and Wales is governed by a well-established but procedurally demanding process administered through HM Land Registry. Whether you are selling, gifting a property to a family member, adding a partner to the title, or restructuring ownership between existing co-owners, understanding the correct legal mechanism — and the tax and lender obligations each triggers — can prevent costly errors and delays at a legally significant moment.

Key points

- All ownership transfers in England and Wales must be registered at HM Land Registry; unregistered transfers do not confer legal title under the Land Registration Act 2002.

- A TR1 (Transfer of Whole of Registered Title) or TP1 (Transfer of Part) form is the prescribed HM Land Registry deed used for most ownership changes.

- Stamp Duty Land Tax (SDLT) may be payable even on transfers with no cash consideration — for example, when a property is transferred subject to an existing mortgage.

- HMRC requires an SDLT return to be submitted within 14 days of completion, even where no tax is payable (a nil return is still required in most cases).

- Transfers between spouses or civil partners are generally exempt from Capital Gains Tax (CGT) whilst the parties are living together, but may trigger CGT obligations on later disposal by the recipient.

The legal framework: how ownership actually transfers

Property ownership in England and Wales is governed principally by the Land Registration Act 2002. Legal ownership only passes when HM Land Registry records the change of proprietor in the register — an agreement to transfer, or an unsigned deed, does not change legal title.

The primary vehicle for a full transfer is the TR1 form, a prescribed HM Land Registry deed completed by the transferor (current owner) and executed — signed in the presence of an independent witness — by both parties where covenants are given. For transfers of part of a registered title, such as a plot of land being sold separately from the main property, a TP1 form is used instead.

For unregistered land — a small but still existing part of the UK property stock — the process differs and involves title deeds and a first registration application. A solicitor experienced in unregistered conveyancing should be instructed in those cases.

Common transfer mechanisms compared

Mechanism | Typical scenario | SDLT position | CGT position | Key requirement |

|---|---|---|---|---|

Sale at market value | Standard purchase or sale | Payable on purchase price | Seller potentially liable unless principal private residence relief applies | Full conveyancing process; regulated solicitor required |

Gift with no consideration | Transfer to family member; no mortgage in place | Nil if no mortgage assumed | Market value used for CGT even if no money changes hands | Tax advice on IHT recommended; TR1 deed required |

Transfer subject to mortgage | Adding or removing a co-owner on a mortgaged property | SDLT on outstanding mortgage balance assumed | Depends on consideration passing | Lender consent essential before proceeding |

Spouse or civil partner transfer | Matrimonial restructuring or divorce settlement | Exempt between spouses or civil partners | CGT exempt if living together; seek advice on separation scenarios | Family law and conveyancing advice both required |

Assent from estate | Inheriting property from a deceased person | Not usually payable | Base cost is probate value | Grant of probate or letters of administration required first |

Severance of joint tenancy | Changing from joint tenants to tenants in common | No SDLT event | No CGT event | Form SEV or deed registered at HM Land Registry |

SDLT and CGT rules are subject to legislative change and depend on individual circumstances. Seek professional tax advice before proceeding. Indicative guidance only.

Documents typically required for a property transfer

- TR1 or TP1 deed — completed and executed by the transferor; executed by the transferee where covenants are given

- Official copies of the title register and title plan — current entries obtained from HM Land Registry

- Proof of identity for all parties — photographic ID and proof of address under the HM Land Registry Digital Identity Standard

- SDLT return (HMRC form SDLT1) — submitted within 14 days of completion; nil returns are required even where no tax is payable

- AP1 (application to change the register) — submitted by the solicitor to update the proprietor entry at HM Land Registry

- Lender consent documentation — required if a mortgage remains in place after the transfer

- Mortgage discharge documentation — if the existing mortgage is being repaid as part of the transfer

- Gift letter and donor bank statements — if any part of the consideration is a financial gift

Which transfer mechanism applies to your situation?

- Transfer at full market value to a third party? Standard conveyancing sale process applies — instruct a conveyancing solicitor.

- Gifting to a family member with no mortgage? TR1 deed with no cash consideration — take legal and tax advice on CGT and Inheritance Tax (IHT) before proceeding.

- Adding a partner or spouse to a mortgaged title? Lender consent required first; a remortgage may be needed; SDLT is payable on the share of the outstanding mortgage being transferred.

- Transfer following separation or divorce? Seek both family law and conveyancing advice; court orders frequently govern the timing and mechanism.

- Inheriting through an estate? The personal representative must complete probate before any transfer can proceed; an AS1 assent form passes title from the estate to the beneficiary.

- Changing co-ownership type from joint tenants to tenants in common? File Form SEV at HM Land Registry — there is no change of ownership, but registration is required for the severance to take effect against third parties.

Important limitations

This article describes general principles of property transfer law in England and Wales as of May 2026. Scotland and Northern Ireland have separate legal systems with different forms and processes. SDLT, CGT, and Inheritance Tax rules are complex, subject to legislative change, and depend heavily on individual circumstances. Nothing in this article constitutes legal or tax advice. Instruct a qualified, SRA- or CLC-regulated conveyancing solicitor and, where relevant, a tax adviser before proceeding with any transfer.

When this becomes urgent

Seek legal advice without delay if:

- A property in a deceased estate is subject to a mortgage and needs to be transferred quickly to prevent arrears accruing.

- A court order in divorce proceedings sets a deadline for completing a transfer of equity.

- You have already exchanged contracts and discover a title issue that may affect the transfer mechanism or completion date.

What to ask a qualified professional

Before instructing a solicitor for a property transfer, ask:

- What form of transfer deed is appropriate for my specific situation — TR1, TP1, or another instrument?

- Is SDLT payable, and if so, on what amount and within what timeframe?

- Are there CGT or IHT implications I should address before proceeding?

- If a mortgage is in place, what lender consent is needed and how long does it typically take to obtain?

- What are your fees for this type of transfer, and what disbursements should I budget for?

- Will you submit the SDLT return on my behalf, and what information do you need from me to do so?

When to get professional help

Property ownership transfer almost always requires a qualified conveyancing solicitor or licensed conveyancer. Seek regulated advice before proceeding if:

- The property is mortgaged — lender consent and possible remortgage advice are essential.

- The transfer forms part of divorce or separation proceedings.

- You are concerned about Inheritance Tax implications, particularly if the donor is elderly or in poor health and may not survive seven years from the date of a gift.

- The property is leasehold — the lease may require landlord consent for permitted transfers.

- The title has known defects, missing documents, or active disputes.

How Housey can help

Housey works with regulated conveyancing solicitors experienced in all types of property ownership transfer — from standard sales and transfer of equity to family gift transfers and estate assents. Use our conveyancing service to compare quotes from vetted firms and find professional advice matched to your transfer type.

Frequently asked questions

Can I transfer property to a family member without selling it?

Yes. A gift transfer using a TR1 deed is legally possible. However, if the property is mortgaged, you will need the lender's consent. Capital Gains Tax may be payable on any gain accrued since you acquired the property — market value at the transfer date is used even if no money changes hands. Take professional tax advice before proceeding.

Do I need to pay Stamp Duty Land Tax when transferring property as a gift?

It depends on whether a mortgage is involved. If the property transfers with no outstanding mortgage and no cash consideration, SDLT is typically nil. If transferred subject to an existing mortgage, HMRC treats the outstanding balance as chargeable consideration, which may trigger an SDLT liability. A nil return may still be required. Confirm with your solicitor.

How long does a property transfer take to complete and register?

A straightforward freehold sale typically completes in 8 to 16 weeks. A transfer of equity with lender involvement may take 4 to 10 weeks depending on the lender's response time. Following completion, registration at HM Land Registry can currently take several weeks to several months depending on application volumes and complexity.

Can I transfer property without using a solicitor?

HM Land Registry forms are publicly available, but the process involves legal, tax, and lender obligations that are easy to get wrong without professional guidance. Errors in the TR1 deed, missed SDLT filings, or failure to obtain lender consent carry serious consequences. Using a qualified solicitor or licensed conveyancer is strongly recommended.

Sources and further reading

- HM Land Registry: registering land or property — GOV.UK / HM Land Registry

- HMRC SDLT guidance: transfers of equity — GOV.UK / HMRC

- Land Registration Act 2002 — legislation.gov.uk

- HM Land Registry Practice Guide 24: private trusts of land — GOV.UK / HM Land Registry

Useful next reads

Buying & Moving

Buying & MovingProperty Ownership Transfer: Legal Process and Documentation

Transferring property ownership in England and Wales involves a formal legal deed — usually the TR1 form — submitted to HM Land Registry alongside an SDLT return filed within 14 days of completion.

Buying & Moving

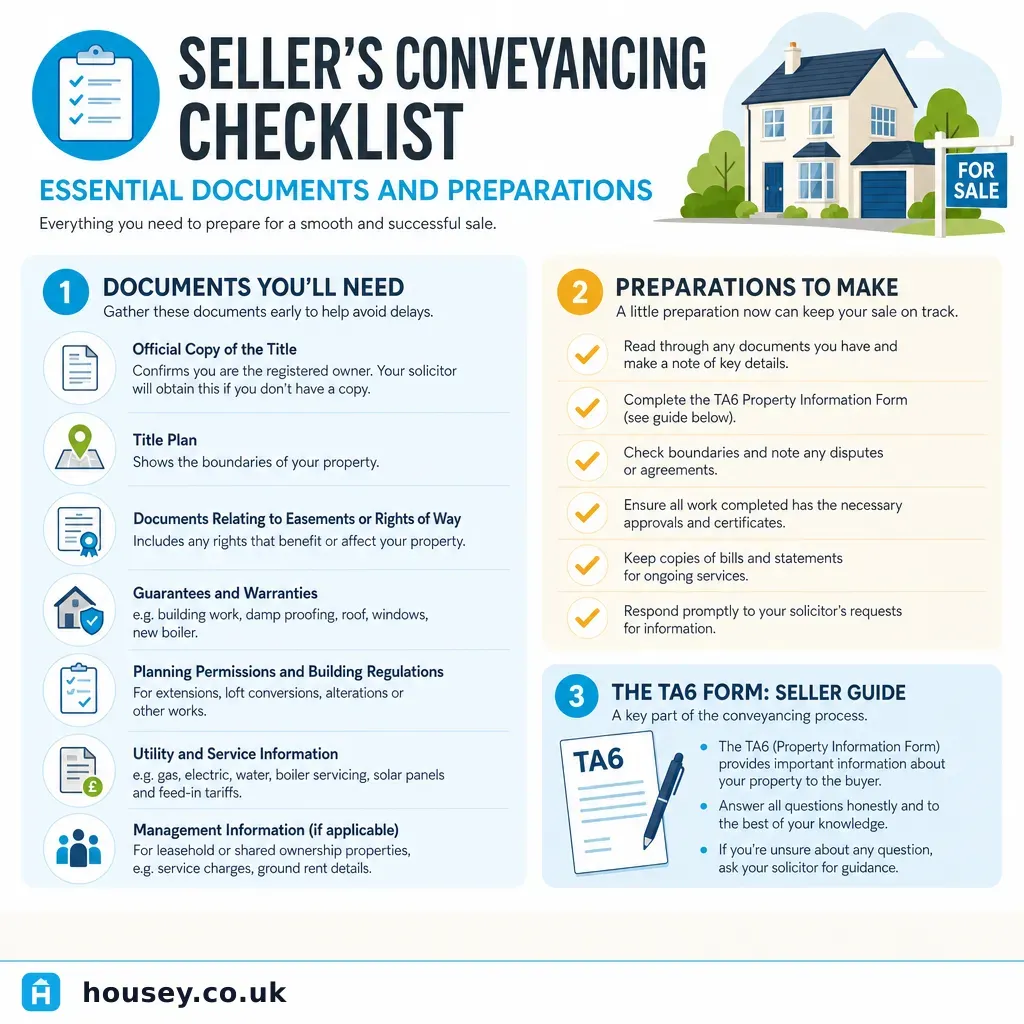

Buying & MovingSeller's Conveyancing Checklist: Essential Documents and Preparations

Sellers need to gather title documents, completed Law Society forms (TA6 and TA10), building regulations certificates, planning permissions, and — for leasehold properties — a management information pack before or shortly after accepting an offer.

Buying & Moving

Buying & MovingComplete Homebuying Checklist and Essential Services for First-Time Buyers

First-time buyers in the UK should commission an independent RICS Home Survey before exchange — a mortgage lender's valuation does not protect you.

Buying & Moving

Buying & MovingBuyer's Conveyancing Checklist: Steps and Documents You'll Need

Conveyancing for buyers in England and Wales typically takes 8–16 weeks across five stages: instruction and ID checks, searches, mortgage offer and enquiries, exchange, and completion.

Buying & Moving

Buying & MovingProperty Information Questionnaires: What You Need to Complete for Sale

When selling a home in England and Wales, you must complete the TA6 Property Information Form and TA10 Fixtures, Fittings and Contents form before contracts can be exchanged.