Monitoring the Remodelling Sector While New Construction Continues to Rise

By Housey · Last reviewed 24th of May 2026

Monitoring the Remodelling Sector While New Construction Continues to Rise

The relationship between renovation demand and new-build output is not straightforward: they respond to different economic levers, serve different segments of the market, and compete for the same pool of skilled tradespeople. For homeowners considering improvement work — and for anyone tracking the wider UK residential market — understanding the dynamics of both sectors helps set realistic expectations around contractor availability, lead times, and material costs.

Key points

- ONS construction output data separates "repair and maintenance" (R&M) from "new work," providing a quarterly indicator of renovation sector activity alongside new-build volumes.

- Private housing new-build completions in England are published quarterly by the Ministry of Housing, Communities and Local Government (MHCLG); NHBC separately tracks new-build registrations and warranty enrolments as a forward indicator.

- The Federation of Master Builders (FMB) State of Trade Survey is published quarterly and reports on SME builder workloads, material availability, labour shortages, and price inflation — making it a practical leading indicator for homeowner project planning.

- The UK's housing stock has an average age placing the median dwelling built around the mid-1960s; this ageing inventory drives consistent demand for renovation, regardless of new-build volumes.

- When Stamp Duty Land Tax thresholds fall or house prices stagnate, homeowners more often improve in place rather than move — shifting expenditure from the transaction market into the renovation sector.

How new-build output and renovation demand interact

New-build and renovation are sometimes presented as substitutes, but the reality is more nuanced. New-build activity responds primarily to land availability, planning consent rates, housebuilder confidence, and mortgage conditions. Renovation demand is driven by a different set of factors: the condition of the existing stock, energy efficiency requirements, household formation, and the relative cost of moving versus improving.

When new-build output rises sharply — as occurred in the years following the launch of Help to Buy (2013–2023) — it does not necessarily depress renovation spending. In many periods, both sectors grow simultaneously, particularly when general consumer confidence is high. What new-build growth does do is intensify pressure on skilled labour and materials, as both sectors draw from the same supply base. This was especially visible during 2020–2022, when pandemic-driven renovation demand and a recovering new-build pipeline collided with material shortages and tradespeople committed months ahead.

What the data tells us about renovation sector health

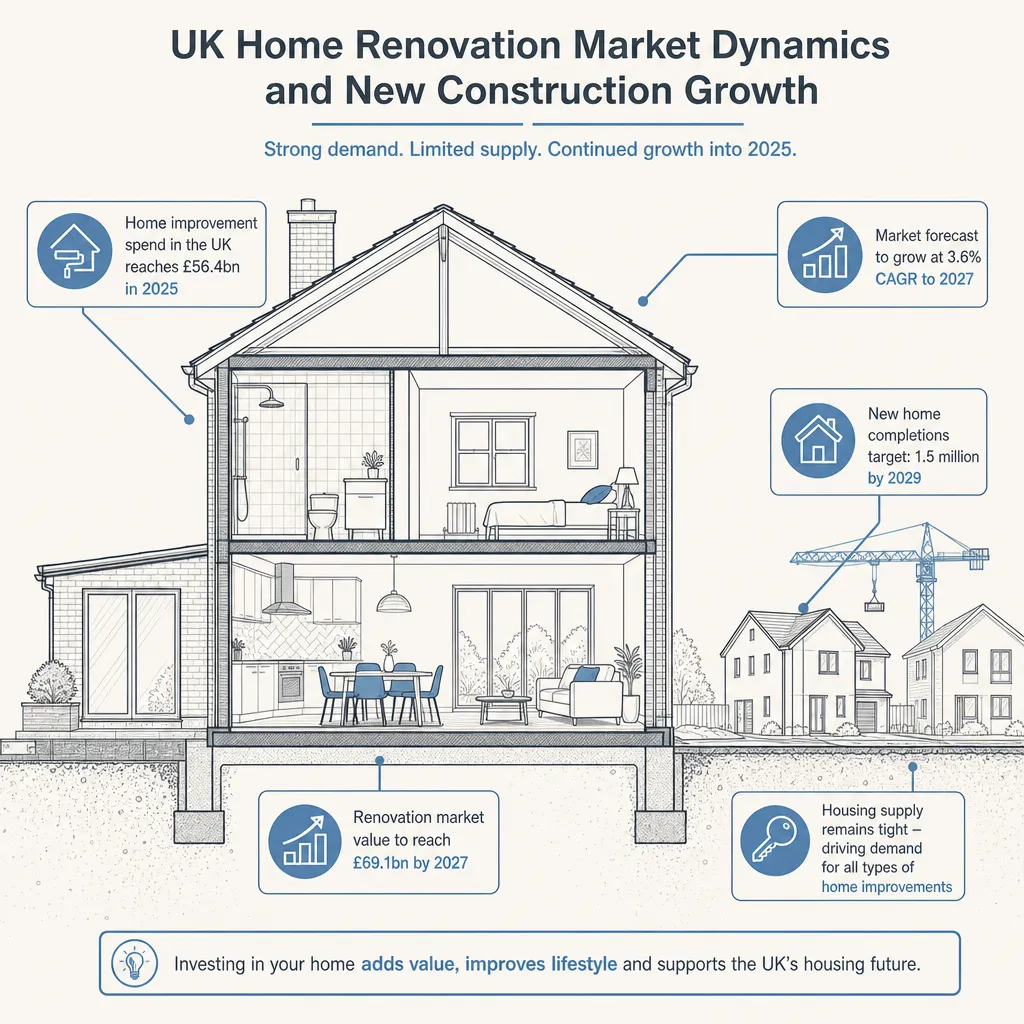

The ONS publishes monthly and quarterly construction output figures that disaggregate repair and maintenance from new work. Private housing R&M output is the most direct indicator of residential renovation sector activity. Separately, MHCLG's house building statistics cover new-build completions and starts.

Key indicators homeowners and contractors should monitor:

Indicator | Source | What it signals |

|---|---|---|

Private housing R&M output (quarterly) | ONS Construction Output | Overall volume of renovation sector activity |

New private housing completions (quarterly) | MHCLG House Building Statistics | New-build delivery rate against housing targets |

FMB State of Trade Survey: workloads and enquiries | Federation of Master Builders | SME builder capacity and forward demand |

Construction material price indices | ONS / BCIS | Cost pressure on renovation projects |

RICS UK Residential Market Survey | RICS | Buyer confidence, price expectations, stock levels |

These indicators together give a more complete picture than any single measure. A period of high new-build activity combined with an FMB survey showing full order books and material shortages signals that homeowners commissioning renovation work may face longer wait times and higher quotes.

What drives renovation demand independently of new build

Several structural factors sustain UK renovation demand regardless of new-build volumes:

Ageing housing stock. The UK's residential stock is old by international standards. Pre-1919 homes make up a significant proportion of the national housing stock, particularly in northern England, Wales, and Scotland. These properties require ongoing maintenance and periodic improvement investment regardless of new-build activity.

Energy retrofit obligations. Minimum Energy Efficiency Standards (MEES) require private rented properties to meet at least EPC band E, with proposed future tightening towards band C. This regulatory driver creates baseline renovation demand independent of consumer preference or economic conditions.

Stamp Duty Land Tax friction. Moving home in England involves SDLT costs that can run to tens of thousands of pounds on average-priced properties. When SDLT costs are high relative to expected gains from moving, more homeowners choose to extend or adapt their current home rather than trade up.

Planning constraints in desirable locations. In many urban and suburban areas, planning restrictions on new development in established neighbourhoods mean the only practical route to more space is renovation rather than new build.

What this means for homeowners planning improvement work

Understanding where the renovation sector sits in the cycle helps homeowners time projects more effectively:

- In a high-demand period (full builder order books, rising material costs, long lead times): consider starting enquiries earlier than you might expect — good contractors may be 3–6 months or more out.

- In a softer demand period (FMB surveys show declining workloads, material prices stabilising): contractor availability tends to improve and quotes may be more competitive.

- Check material costs before budgeting: construction material prices can shift meaningfully quarter-to-quarter. Ask builders to break out materials and labour in quotes, and clarify whether material costs are fixed or subject to adjustment.

Red flags in the current market

Be cautious if:

- A contractor quotes significantly below the market rate during a period of high material prices — this may indicate corners being cut on materials, underpayment of subcontractors, or a firm under financial pressure.

- Lead times have dropped sharply in a previously congested trade but material prices have not fallen commensurately — this can indicate a demand correction underway that may affect contractor viability mid-project.

- Multiple contractors decline to quote on a straightforward project — high refusal rates usually indicate the pipeline is full rather than the project being problematic. Consider revising scope or timing rather than accepting the only quote received.

- A builder cannot provide references from recent comparable projects — in a healthy market, active contractors have a recent track record they are willing to share.

When to get professional help

If you are planning a substantial improvement project (over £50,000 of works), consider appointing a project manager or contract administrator to manage procurement, contractor selection, and programme. For complex or high-value projects, RICS-regulated quantity surveyors can provide cost plans, tender management, and independent cost certification — reducing the risk of budget overrun in a volatile materials market.

How Housey can help

Housey's service directory connects homeowners with vetted local contractors across a range of renovation disciplines. Whether you are planning an extension, energy retrofit, or a whole-home refurbishment, comparing multiple quotes from local providers remains the most reliable way to benchmark cost in a fluctuating market.

Frequently asked questions

Is UK renovation spending growing or declining?

ONS construction output data shows that private housing repair and maintenance has historically been resilient even during new-build downturns. Demand drivers — ageing stock, energy efficiency requirements, stamp duty friction on moving — tend to sustain renovation spending through economic cycles. Checking the latest ONS quarterly construction output release gives the most current picture.

Do new-build developments affect renovation contractor availability?

Yes. Both sectors draw on similar pools of skilled labour (bricklayers, joiners, plumbers, electricians) and often compete for the same materials. In periods of high new-build activity, renovation contractors may be busier and lead times longer. Monitoring FMB State of Trade surveys gives a practical indication of SME builder capacity.

How does stamp duty affect home improvement spending?

When Stamp Duty Land Tax costs are high relative to expected value gains from moving, more homeowners choose to improve rather than move. This effect has been observed in periods following SDLT threshold changes. HMRC's SDLT receipts data and house price indices from Nationwide and Halifax provide useful context.

Sources and further reading

- Construction Output in Great Britain — Office for National Statistics

- House Building Statistics — Ministry of Housing, Communities and Local Government

- State of Trade Survey — Federation of Master Builders

- UK Residential Market Survey — RICS

- Minimum Energy Efficiency Standards for domestic private rented properties — GOV.UK

Useful next reads

General property advice

General property advicePost-Lockdown Migration: Understanding Buyer Movement Out of Urban Areas

The COVID-19 lockdowns triggered a significant shift in UK buyer priorities, with many households trading city flats for more space in commuter towns, market towns, and rural areas.

General property advice

General property adviceRental Market Trends: Garden Space Demand Among Tenants

Demand for rental properties with garden access has grown markedly since 2020, with families, remote workers, and pet owners rating outdoor space among their top priorities.

General property advice

General property adviceGarden Space Demand: What Modern Homebuyers Are Looking For

Gardens and private outdoor space rank among the most sought-after features for UK homebuyers, particularly since 2020.

General property advice

General property adviceUK Home Renovation Market Dynamics and New Construction Growth

UK home renovation demand is driven by the cost of moving, ageing housing stock, energy efficiency requirements, and hybrid working patterns.

General property advice

General property adviceWhat to do when your boiler stops working

When your boiler stops working, check the pressure gauge (should read 1–1.