What Drives Current Property Valuation Peaks

By Housey · Last reviewed 18th of May 2026

What Drives Current Property Valuation Peaks

Property prices across much of the UK have reached or approached record levels in recent years, and understanding what lies behind those peaks matters whether you are buying, selling, remortgaging, or ensuring your buildings insurance reflects a credible reinstatement cost. Property valuations in the UK are shaped by a combination of structural economic conditions, local supply-and-demand dynamics, and the specific methodology applied — each approach yielding a different figure depending on the purpose of the exercise.

Key points

- Market value and insurance reinstatement (rebuild) value use entirely different methodologies and should never be conflated: a property worth £450,000 on the open market may cost £220,000 to rebuild — or, in some markets, considerably more than the sale price.

- RICS-registered valuers follow the Red Book (RICS Valuation — Global Standards 2022) for formal market valuations; residential lender valuations are additionally governed by UK Finance Lenders' Handbook instructions.

- The primary method for UK residential market valuation is the sales comparison approach, using recent comparable transactions from the HM Land Registry register adjusted for differences in condition, size, EPC rating, and property attributes.

- Stamp Duty Land Tax (SDLT) thresholds create measurable price clustering in England's market, with demand concentrating just below key bands at £250,000, £500,000, and £925,000.

- Rebuild costs have risen sharply since 2020 due to materials and labour price inflation; the ABI rebuild cost calculator and RICS Reinstatement Cost Assessment (RCA) service are the recognised references for insurance valuations.

What "market value" means in the UK context

Under the RICS Red Book, market value is defined as "the estimated amount for which an asset or liability should exchange on the valuation date between a willing buyer and a willing seller in an arm's length transaction, after proper marketing and where the parties had each acted knowledgeably, prudently and without compulsion."

This definition matters in practice because it excludes:

- Distress sales — where a forced seller accepts below-market offers due to financial pressure or time constraints.

- Special purchaser premiums — where a buyer values the property above market because of its proximity to their own land or business.

- Off-market transactions — where insufficient marketing may not have found the best available price.

For most residential purposes — mortgage valuations, probate, Help to Buy redemptions, shared ownership staircasing — the Red Book framework applies. An RICS-registered valuer draws on recent comparable sold prices from HM Land Registry to anchor their professional opinion.

The key drivers of UK property valuation peaks

Driver | Mechanism | Who is most affected |

|---|---|---|

Constrained housing supply | Low completions relative to household formation keep competition among buyers elevated | All buyers in undersupplied markets, particularly urban and commuter areas |

Historically low mortgage rates (pre-2022) | Lower borrowing costs expanded the pool of buyers competing for available stock | First-time buyers and high-LTV borrowers |

Interest rate rises (from 2022) | Reduced affordability, putting downward pressure on prices in higher-LTV segments | Buyers with smaller deposits; property investors; higher-priced segments |

SDLT threshold effects | Demand clustering just below £250,000, £500,000, and £925,000 creates price stickiness near key bands | Sellers and buyers near these thresholds; investors pricing acquisitions |

Planning and conservation restrictions | Green belt, Article 4 directions, and conservation area designations limit new supply in high-demand areas | Buyers in London, the South East, and historic market towns |

Energy efficiency premium | A/B rated homes increasingly attract a premium over D/E-rated equivalents in competitive markets | Buyers considering long-term running costs; landlords managing MEES exposure |

Rebuild cost inflation | Materials and labour price rises since 2020 drive reinstatement values independently of market trends | All property owners — affects insurance valuations in particular |

How comparable sales drive residential valuations

The sales comparison approach is the dominant methodology for UK residential market valuations. In practice, a RICS-registered valuer or estate agent appraiser will:

- Identify comparable transactions within a defined time window (usually 3–6 months) and area (typically within 0.5 miles for urban properties, wider for rural or unusual stock).

- Adjust comparables for material differences: floor area (often expressed as £ per sq ft), bedroom and bathroom count, garden, parking, condition, EPC rating, floor level for flats, and lease length for leasehold.

- Weight recent transactions more heavily than older ones, particularly in a moving market.

- Apply a judgement discount or premium for unusual features: listed building status, short lease (below 80 years typically carries a noticeable discount due to extension costs), onerous ground rent escalation, flying freehold, or restricted access.

Worked example: A two-bedroom Victorian terrace in a market town, EPC D, street parking only, recently redecorated. Comparable sales on similar streets within 0.3 miles range from £265,000 to £310,000. The valuer identifies parking as adding approximately £8,000–£10,000 based on matched-pair evidence; EPC D versus C comparables suggest a discount of £5,000–£8,000. Applying these adjustments and weighting the most recent transaction most heavily, the valuer reports a market value of £282,000.

Insurance valuations — why they differ from market value

The reinstatement cost used for buildings insurance is entirely separate from market value. It represents the cost of demolishing the structure and rebuilding it to the same floor area and specification, to current Building Regulations standards, including:

- Architect, structural engineer, and principal designer fees

- Site clearance and enabling works

- Labour and materials at current rates, indexed using BCIS (Building Cost Information Service) data

- Compliance with current Building Regulations, including Part L (energy efficiency), Part M (accessibility), and Part B (fire safety)

The ABI's free rebuild cost calculator is the standard reference for standard residential properties. For unusual, listed, or high-value properties, a formal RICS Reinstatement Cost Assessment (RCA) provides a more reliable basis for insurance cover.

Common errors in insurance valuations:

- Underinsurance: Setting reinstatement cover at market value when rebuild cost is higher — most common in London and the South East, where land values can make market price exceed true build cost.

- Overinsurance: Setting cover at market value when build cost is lower — common in lower-value markets where land represents a large share of market price.

- Stale valuations: Not updating reinstatement figures after major extensions, alterations, or periods of significant materials cost inflation.

Important limitations

Property valuations depend on professional judgement applied to specific, current market evidence. The drivers described in this article reflect general trends across the UK residential market and cannot predict the value of any specific property. Formal valuations for mortgage purposes, probate, capital gains tax, Help to Buy, shared ownership, or lease extension premium calculations must be carried out by a qualified RICS-registered valuer with knowledge of the relevant local market. Insurance valuations for complex, listed, or high-value properties should be provided by a qualified cost consultant or RICS member, not calculated using a generic online tool. Nothing in this article constitutes professional valuation advice.

When this becomes urgent

Seek a professional valuation promptly if:

- Your buildings insurance reinstatement figure has not been reviewed since before 2020 — materials and labour cost inflation since then may mean you are significantly underinsured.

- You have received a lender's mortgage valuation below the agreed purchase price and want to understand whether a review or challenge is appropriate.

- You are involved in probate, divorce proceedings, or a business dissolution where a formal, independent valuation is required.

- You are extending a leasehold — the statutory lease extension premium is calculated using a formal RICS valuation, and the process has defined legal timescales.

- Your property has been significantly extended or altered since the last formal valuation.

What to ask a qualified professional

Before instructing a RICS-registered valuer:

- Are you RICS-registered and do you carry professional indemnity insurance? Can you confirm your RICS membership number?

- What is the stated purpose of the valuation, and will the report be Red Book-compliant?

- What comparable evidence will you use, and over what time window and area?

- Do you have direct experience of valuing properties of this type in this specific local market?

- Are your fees quoted inclusive of VAT, and what is the expected turnaround time?

- If the instruction includes insurance purposes, will you provide a RICS Reinstatement Cost Assessment (RCA) rather than a market value report?

When to get professional help

Consider a professional valuation rather than relying on automated estimates if:

- You are making a significant financial decision — purchase, remortgage, or equity release — where the valuation underpins the transaction.

- Your property is unusual in construction, condition, tenure, or planning history in ways that automated valuation models cannot assess.

- There is a dispute about value for inheritance, boundary, planning, or insurance purposes.

- Your buildings insurance reinstatement figure has not been updated in more than three years, or since a major extension or renovation.

How Housey can help

Housey connects homeowners and buyers with RICS-registered professionals who can carry out valuation surveys for purchase, remortgage, and dispute purposes. If your buildings insurance reinstatement cost needs reviewing, insurance valuations from a qualified cost consultant ensure your cover keeps pace with rebuild cost inflation. For a broader picture combining condition assessment with valuation context, a RICS Home Survey provides professional insight across both dimensions.

Frequently asked questions

What is the difference between asking price and market value?

Asking price is set by the vendor — usually guided by an estate agent's appraisal — and reflects what the seller hopes to achieve. Market value is a formal professional opinion of the most probable sale price in an arm's length transaction. In a rising market, achieved prices may exceed asking; in a flat or falling market, agreed sale prices may fall below. A mortgage lender's valuation is based on market value evidence, not asking price.

How does a mortgage valuation differ from a full survey?

A mortgage valuation is a brief inspection carried out primarily for the lender's benefit, confirming the property provides adequate security for the loan. It does not identify all defects or report comprehensively on condition. A RICS Level 2 or Level 3 Home Survey is a separate, more detailed inspection for the buyer's benefit and should not be omitted based solely on the mortgage valuation result.

Why has my buildings insurance rebuild cost risen so much?

Rebuild costs are driven by construction labour and materials prices, both of which rose sharply from 2020 through 2023 and remain elevated. BCIS rebuild cost indices reflect these movements. A reinstatement figure set three or more years ago is likely to understate the current cost, potentially leaving the property underinsured. Review your figure at least every three years or after any major works using the ABI calculator.

Do automated valuation models replace a professional survey?

No. Automated valuation models (AVMs) provide statistical estimates based on comparable sales and algorithmic adjustments, but cannot assess condition, legal complications, planning constraints, unusual construction, or specific property features. For any significant financial decision, a RICS-registered valuer's professional opinion is the appropriate standard.

Sources and further reading

- UK House Price Index — HM Land Registry / ONS

- RICS Valuation — Global Standards (Red Book) — RICS

- ABI rebuild cost calculator guidance — Association of British Insurers

- BCIS rebuild cost indices — Building Cost Information Service (RICS)

- Stamp Duty Land Tax rates and thresholds — GOV.UK

Useful next reads

Buying & Moving

Buying & MovingHow to Get Your Property Professionally Valued

To get a professional property valuation in the UK, instruct a RICS Registered Valuer for any formal purpose — mortgage, probate, Help to Buy, or legal proceedings.

Buying & Moving

Buying & MovingUnderstanding Local Property Values: What Homes Sold For in Your Area

Sold prices for UK properties are publicly recorded by HM Land Registry for England and Wales, Registers of Scotland, and Land and Property Services in Northern Ireland.

Buying & Moving

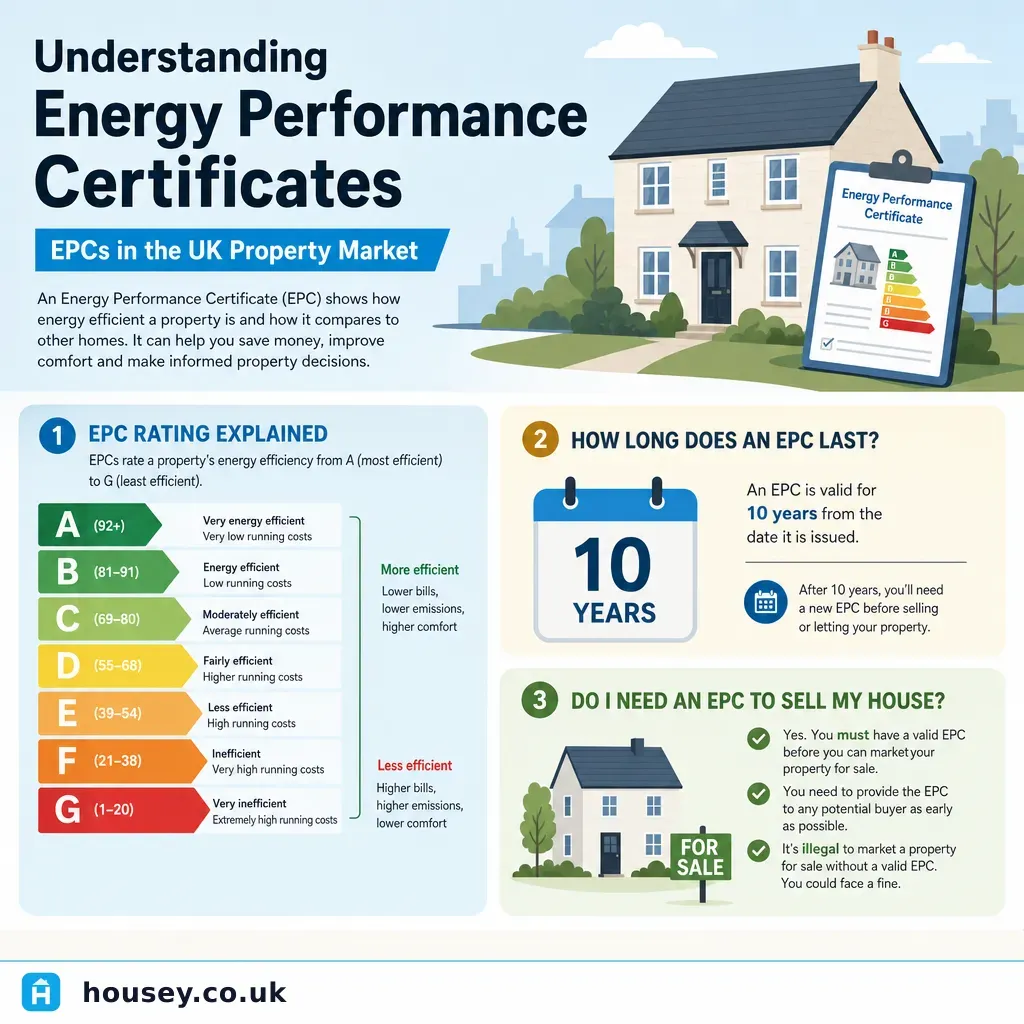

Buying & MovingUnderstanding Energy Performance Certificates: EPCs in the UK Property Market

An Energy Performance Certificate (EPC) rates a property's energy efficiency on a scale from A (most efficient) to G (least efficient).

Buying & Moving

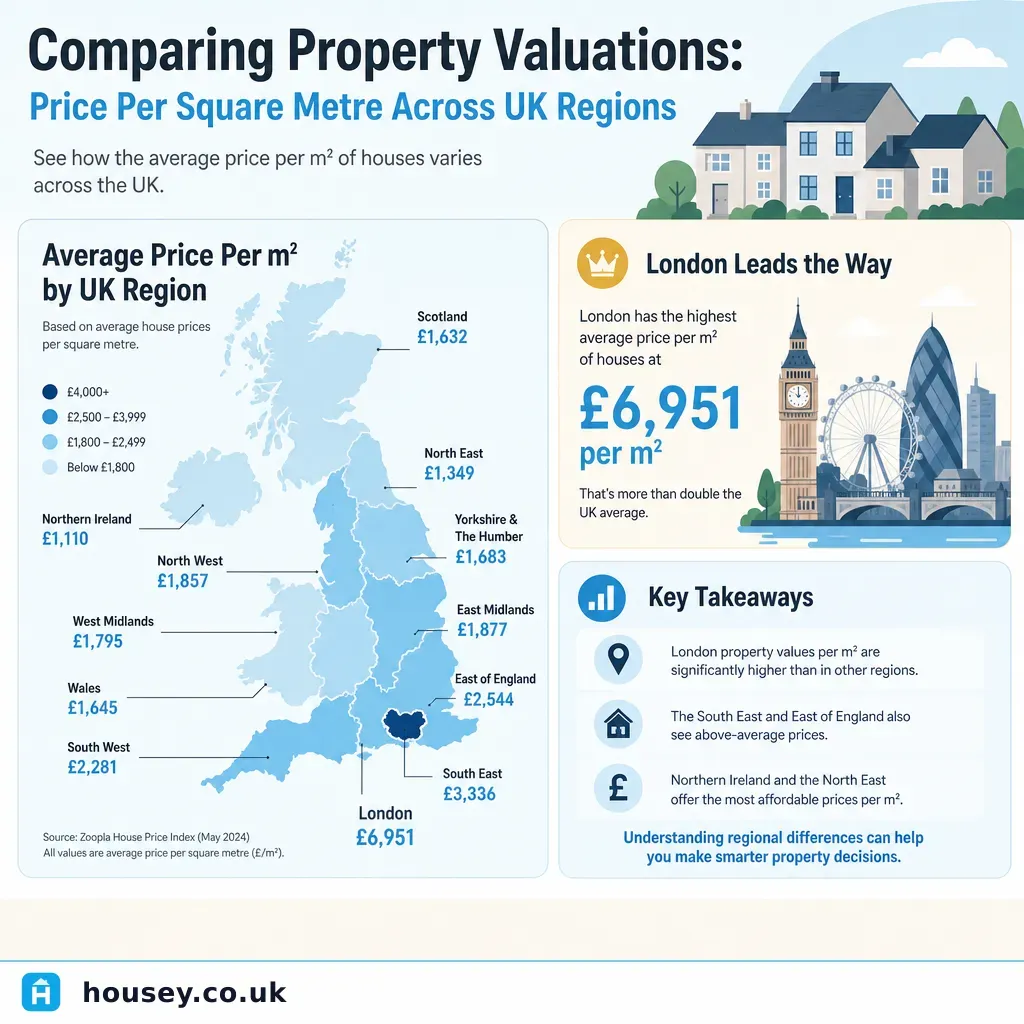

Buying & MovingComparing Property Valuations: Price Per Square Metre Across UK Regions

Property prices per square metre vary dramatically across UK regions.

Buying & Moving

Buying & MovingDetermining Your Property's Market Value: Valuation Guide for Sellers

Market value in the UK is most reliably established by combining estate agent appraisals with your own analysis of recent sold prices on the HM Land Registry database.