What to Do When a Tree Falls on Your House

By Housey · Last reviewed 11th of May 2026

What to Do When a Tree Falls on Your House

A tree falling on a house is among the most alarming emergencies a UK homeowner can face. It most often happens during storms or high winds, though diseased, drought-stressed, or root-damaged trees can fall with little warning at any time of year. The decisions made in the first minutes and hours after impact — whether to stay, who to call, and which contractors to authorise — directly affect the safety of everyone in the household, the outcome of your insurance claim, and the long-term structural integrity of your home.

Key points

- Evacuate all occupants immediately if the tree has breached the roof, if you can smell gas, if you see electrical sparks, or if there is any visible structural movement or wall distortion.

- Emergency removal of a tree from a damaged structure must be carried out by a qualified arborist holding current NPTC (Lantra Awards) chainsaw qualifications — cutting into a loaded tree incorrectly can cause catastrophic redistribution of weight onto a compromised structure.

- UK buildings insurance typically covers sudden, accidental damage from a fallen tree including removal costs and structural repairs, but check your policy for debris-removal sub-limits, which can be as low as £500 separately from the main repair claim.

- A neighbour is not automatically liable if their tree falls on your property; liability in English law depends on establishing negligence — for example, proving the tree was known to be diseased or dead and that no remedial action was taken.

- A chartered structural engineer should assess roof, wall, and foundation integrity before you reinhabit the property or begin permanent repair work; visible damage rarely tells the full story of what has happened to the structure.

Immediate steps: a decision guide for the first hour

Use the following guide to prioritise your response after a tree-fall incident.

- Evacuate immediately if the roof is breached, walls are cracking or moving, or ceilings are deflecting — treat the building as structurally compromised until a professional confirms otherwise. Do not go back inside to retrieve belongings.

- Call 999 if anyone is trapped or injured, if you can smell gas, if there is smoke or fire, or if the structure appears to be collapsing.

- Call National Gas Emergencies (0800 111 999) if you suspect a gas leak — also avoid using any electrical switches, which could ignite gas.

- Call your distribution network operator (DNO) if overhead power lines are involved — find yours at Energy Networks Association. Do not approach or touch downed cables.

- Call your buildings insurer as soon as practicable — most operate 24/7 emergency claims lines. Authorise only emergency weatherproofing before the loss adjuster has attended, unless delay would cause significant further damage.

- Document the damage from outside before any contractor begins clearance — photograph the tree, its break point or root plate, the roof impact zone, and any visible structural damage. This evidence is important for your insurance claim and any potential liability action.

- Arrange professional tree removal through a qualified arborist, not a general contractor. A tree bearing weight on a damaged roof requires specialist knowledge of how load redistributes as sections are removed.

Structural risks to watch for

Even after the tree has been removed, structural damage may not be immediately visible. Arrange a structural engineering assessment before anyone re-enters the property if you observe any of the following:

- Visible cracking or distortion in external or internal walls, particularly stepped diagonal cracks at corners or around window and door openings.

- Roof rafters, ridge board, or purlins that are visibly displaced, fractured, or sagging.

- Ceiling deflection, cracking, or partial collapse in any room below the impact zone.

- Doors or windows that no longer open or close correctly following the impact.

- Any visible gap or separation between the roof structure and the supporting wall plate.

- Foundation settlement cracks, especially widening cracks or cracks accompanied by sticking ground-floor doors.

Do not assume a building is structurally safe because it appears sound from the outside. Obtain a written structural assessment report before reinstating the roof covering or beginning permanent repairs.

Insurance and liability: who pays?

Your own buildings insurance

UK buildings insurance policies typically cover sudden, accidental damage from fallen trees, including:

- Emergency clearance and removal of the tree and debris.

- Repair to the roof, walls, guttering, and other structural elements.

- Temporary emergency boarding and weatherproofing.

- Alternative accommodation if the property is rendered uninhabitable.

Check your policy carefully for:

- Debris-removal sub-limits — some policies cap tree-clearance costs at £500–£1,000 separately from the main repair claim.

- Policy excess — you pay the excess before the insurer covers the balance.

- Unoccupied property exclusions — if the property was vacant beyond your policy's permitted period, cover may be restricted.

Neighbour's tree causing damage to your property

In England and Wales, a neighbour is not automatically liable simply because it was their tree. Liability arises in negligence: you would need to show the neighbour knew or should have known the tree was dangerous and failed to act. Evidence supporting a negligence claim includes a visibly dead or severely diseased tree, prior written correspondence raising concerns about the tree's condition, or a professional report advising the neighbour to carry out works.

In practice, most homeowners claim on their own buildings insurance first and allow the insurer to pursue a subrogated claim against the neighbour's liability insurance where negligence can be established.

Local authority and highway trees

If the tree belonged to the council or a highway authority, report the incident to the council in writing as soon as possible. Local authorities have a duty to inspect and maintain their trees, and negligence claims follow a similar framework to those against private landowners.

Temporary protection and emergency repairs

While awaiting full assessment and repair, take reasonable steps to limit further damage:

- Arrange emergency roof covering — a tarpaulin fixed professionally by qualified roofers prevents further water ingress. Do not attempt this yourself if the roof structure is compromised.

- Board broken windows and doors to secure the property against weather and unauthorised access.

- If water has entered near electrical fittings, isolate the affected circuit at the consumer unit only if it is safe to reach. A qualified electrician (NICEIC or NAPIT registered) should inspect before power is restored to affected circuits.

Do not attempt to remove embedded sections of tree yourself, or carry out structural repairs before the building has been professionally assessed.

What to ask a qualified professional

Arborist / tree surgeon:

- Do you hold current NPTC (Lantra Awards) chainsaw and aerial-rescue qualifications?

- Are you experienced in rigging and removing trees from damaged or compromised structures?

- Do you carry a minimum of £5 million public liability insurance?

- Will you provide a written method statement before starting work?

Structural engineer:

- Are you a Chartered Member of the Institution of Structural Engineers (MIStructE) or a Chartered Structural Engineer via RICS?

- What will your inspection cover — roof structure, wall integrity, foundations?

- Will you provide a written structural assessment report and specify the repair works required?

- How soon can you attend the property?

Roofer:

- Are you experienced in working on storm-damaged or structurally compromised roofs?

- Will you provide a written scope of works and materials specification?

- Do you carry public liability insurance of at least £2 million?

- Can you arrange temporary weatherproofing immediately, pending permanent repairs?

Important limitations

This guide provides general information only. Every tree-fall incident is different — the species and size of the tree, the age and construction of the building, the specific damage sustained, and the terms of your insurance policy all affect the correct course of action. Nothing in this guide constitutes structural engineering advice, legal advice, or insurance advice. Always instruct a qualified structural engineer to inspect the property before re-entering, and consult your insurer before authorising repair works that may affect your claim.

Red flags that indicate a more serious situation

Seek professional help without delay if:

- The tree has not fully come to rest — part of it is suspended or balanced against the roof or a wall. Do not approach it.

- The impact has occurred near a gas meter, service pipe, or boiler flue — evacuate and call 0800 111 999 immediately.

- Rainwater is entering the breach rapidly — water in floor voids, wall cavities, or near electrical fittings escalates risk significantly.

- The property is a pre-1919 solid-wall brick or stone building — these lack the structural redundancy of modern cavity-wall construction and may be more vulnerable to progressive damage after an impact.

- The building is leasehold — your insurance obligations and responsibilities may differ from a freeholder's. Contact your freeholder or managing agent immediately.

When to get professional help

Professional involvement is required from the outset in a tree-fall emergency. The key specialists you may need are:

- Qualified arborist — safe removal of the tree from the structure.

- Structural engineer — assessment of roof, wall, and foundation integrity.

- Roofer — temporary weatherproofing and permanent roof repairs.

- Qualified electrician (NICEIC or NAPIT registered) — inspection if water has entered near electrical fittings or if the consumer unit may have been affected.

- Loss adjuster — appointed by your insurer to assess the damage and approve the scope of repairs.

How Housey can help

Once the immediate emergency is stabilised, Housey can connect you with qualified tree surgeons, specialists in structural engineering assessment, and experienced roofers for the assessment and repair stages. Describe the damage, receive quotes from vetted professionals in your area, and compare them before committing to any contractor.

Frequently asked questions

Does my home buildings insurance cover a fallen tree?

Most UK buildings insurance policies cover sudden, accidental damage from a fallen tree, including removal costs and structural repairs. Check your policy for debris-removal sub-limits (sometimes as low as £500 separately from the main claim), your excess amount, and any conditions relating to property maintenance or unoccupancy. Contact your insurer as soon as possible — most operate a 24/7 emergency claims line.

Am I legally responsible if my tree falls on my neighbour's house?

Not automatically. In English law, liability is based on negligence. If a healthy tree fell during a storm, you are unlikely to be held liable. If the tree was visibly diseased or dead, or had been flagged as hazardous and no action was taken, liability may arise. Your buildings insurance liability section may offer some protection; seek advice from a property solicitor for guidance specific to your circumstances.

How quickly can a qualified tree surgeon respond to a fallen tree emergency?

Many qualified arborists offer 24/7 emergency call-out services, though response times vary by location and demand — particularly after widespread storm events when the profession is at peak capacity. Your insurer may have preferred contractors with faster response times. Expect higher call-out rates outside normal working hours. Prioritise arborists with NPTC or Lantra Awards qualifications for structural removal work.

Do I need planning permission to remove a storm-damaged tree?

If the tree was subject to a TPO, you may carry out urgent works to remove immediate danger without prior consent, but must notify the local planning authority as soon as reasonably practicable. Trees in Conservation Areas follow similar emergency provisions. For non-protected trees no prior consent is needed. Retain photographic evidence of the storm damage to support any retrospective notification the council may require.

Sources and further reading

- Tree Preservation Orders and trees in Conservation Areas — GOV.UK

- Home insurance — what it covers — Association of British Insurers

- Find your electricity distribution network operator — Energy Networks Association

- Find a structural engineer — Institution of Structural Engineers

- Arboriculture qualifications — Lantra Awards

- NICEIC registered electricians — NICEIC

Useful next reads

Improvement & Build

Improvement & BuildTree Removal Services for Fallen Trees

When a tree falls, your first priority is safety — keep clear of structures, unstable root plates, and overhead cables.

Improvement & Build

Improvement & BuildShrub and Vegetation Removal: Costs and Process

Shrub and vegetation removal costs £50–£2,500 or more depending on area size, species involved, and whether stumps need grinding.

Improvement & Build

Improvement & BuildWindow and Door Sill Damage: Repair Solutions

Window and door sill damage ranges from surface cracking and peeling paint to structural rot, spalling stone, or broken concrete.

Improvement & Build

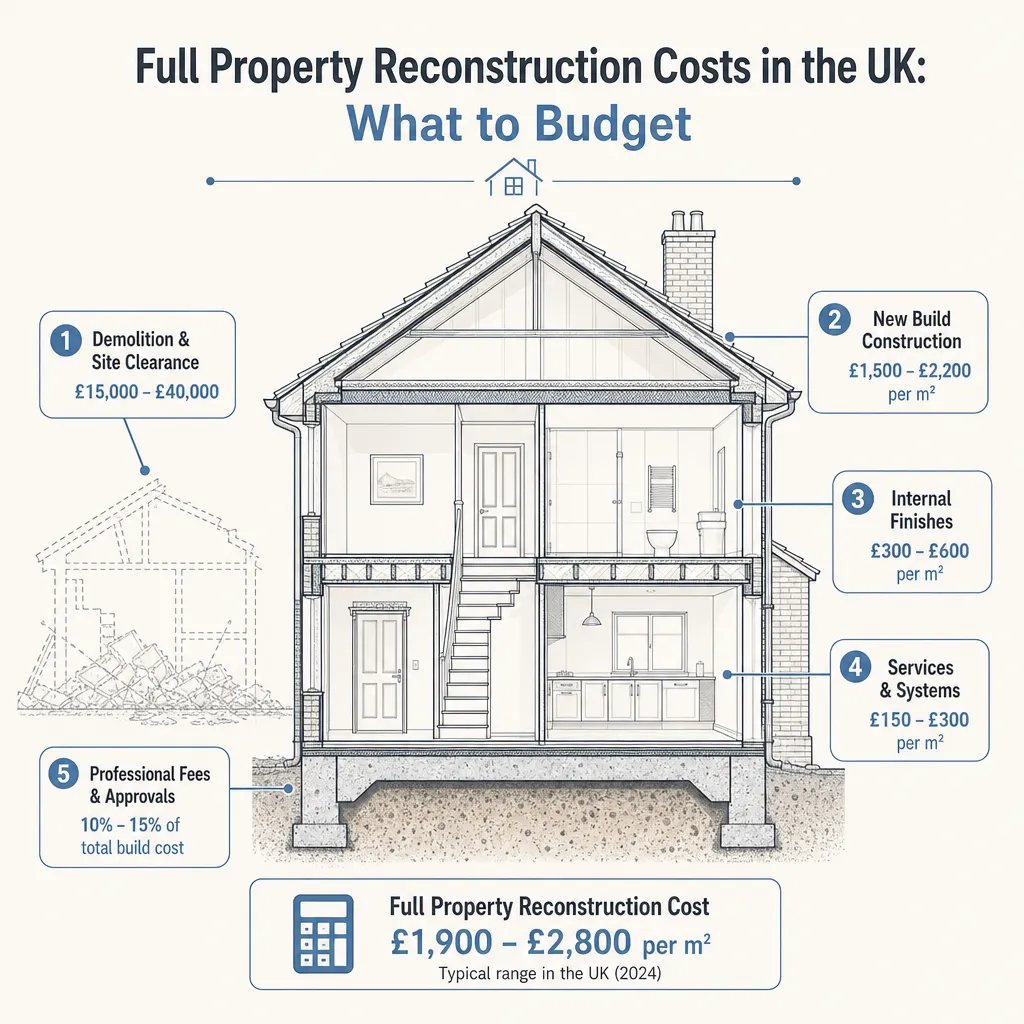

Improvement & BuildFull Property Reconstruction Costs in the UK: What to Budget

Full property reconstruction in the UK typically costs £1,500–£3,000 or more per square metre, excluding demolition, professional fees, and VAT.

Improvement & Build

Improvement & BuildTree Stump Removal Services

Tree stump removal in the UK is most commonly done by stump grinding, which reduces the stump to around 150–300 mm below ground level.