Knowledge Base

Property advice that actually helps

Researched, UK-specific guides for every stage of homeownership — from buying and surveys to retrofit, planning and major works.

Buying & Moving

Buying & MovingObtaining and interpreting your property's floor plans and architectural drawings

Existing floor plans may be available through your local planning authority's public register, your solicitor's conveyancing file, or the original developer. If no accurate drawings exist, a measured building survey by a qualified surveyor produces floor plans and elevations suitable for planning applications, party wall notices, and construction works.

Buying & Moving

Buying & MovingProperty Market Trends: Understanding Demand and Land Value Dynamics

UK property demand is shaped by mortgage affordability, employment levels, housing supply constraints, and planning policy. Land values reflect location, planning status, and development potential rather than simply what is built on a plot. Both are tracked by HM Land Registry and ONS data, but local variations mean national averages rarely reflect conditions in a specific postcode or street.

Buying & Moving

Buying & MovingLeasehold Explained: Ownership Rights and Long-Term Implications

Leasehold means you own the right to occupy a property for a fixed term — you do not own the land or building. Most flats in England and Wales are leasehold. As the lease term shortens it becomes harder to sell or mortgage. Leaseholders have statutory rights to extend their lease, challenge service charges, and take over building management without buying the freehold.

Buying & Moving

Buying & MovingNew Build Property Selection and Pre-Completion Inspection Services

A new-build snagging survey is a professional inspection carried out before or shortly after legal completion that identifies defects, unfinished work, and specification deviations. Most inspectors produce a numbered, photographed snagging list you can submit to your developer for remediation — ideally before completion, while your leverage as a buyer remains strongest.

Buying & Moving

Buying & MovingPreparing Your Home for Sale: Practical Seller Strategies

Preparing a home for sale involves gathering key documents such as an EPC, planning permissions, and building regulations certificates, addressing condition issues that affect survey outcomes and buyer confidence, and presenting the property well for photography and viewings. Neutral décor, professional photography, and realistic pricing consistently have the greatest effect on offers received and time on market.

Buying & Moving

Buying & MovingDownsizing Your Home: Strategic Planning and Practical Steps

Downsizing means selling a larger property and buying a smaller one to release equity and reduce running costs. In the UK, transaction costs — estate agent fees, stamp duty, and conveyancing — typically total £12,000 to £15,000 or more, so the financial benefit depends on the price gap between your current and future home. Timing, tenure type, and local market conditions all affect whether the move makes sense.

Buying & Moving

Buying & MovingSpecialised Moving Solutions for Premium and High-Value Properties

High-value relocations require specialist companies with all-risk transit insurance, climate-controlled vehicles, and trained handlers for art, antiques, and pianos. Standard household removals companies typically cap liability at £40,000–£50,000 per item and do not carry the materials, skills, or insurance needed for fine art, grand pianos, wine collections, or other irreplaceable items.

Buying & Moving

Buying & MovingJoint Mortgage to Single Ownership: Removing Names and Modifying Deeds

Removing a name from a joint mortgage requires both a transfer of equity — updating legal title at HM Land Registry — and the lender's formal written consent to modify the loan. A conveyancer handles the title change and lender liaison, while the lender reassesses sole affordability. Stamp Duty Land Tax may apply on the value of equity transferred, including any mortgage liability assumed.

Buying & Moving

Buying & MovingFirst-Time Buyers in Action: The UK Homeownership Journey

Buying your first home in the UK involves a defined sequence of stages — offer, survey, conveyancing, exchange, and completion — typically spanning 12–16 weeks. Each stage requires specific documents and professional input. Being prepared early, choosing a responsive conveyancer, and commissioning an independent RICS survey are the three decisions that most reliably prevent costly delays.

Buying & Moving

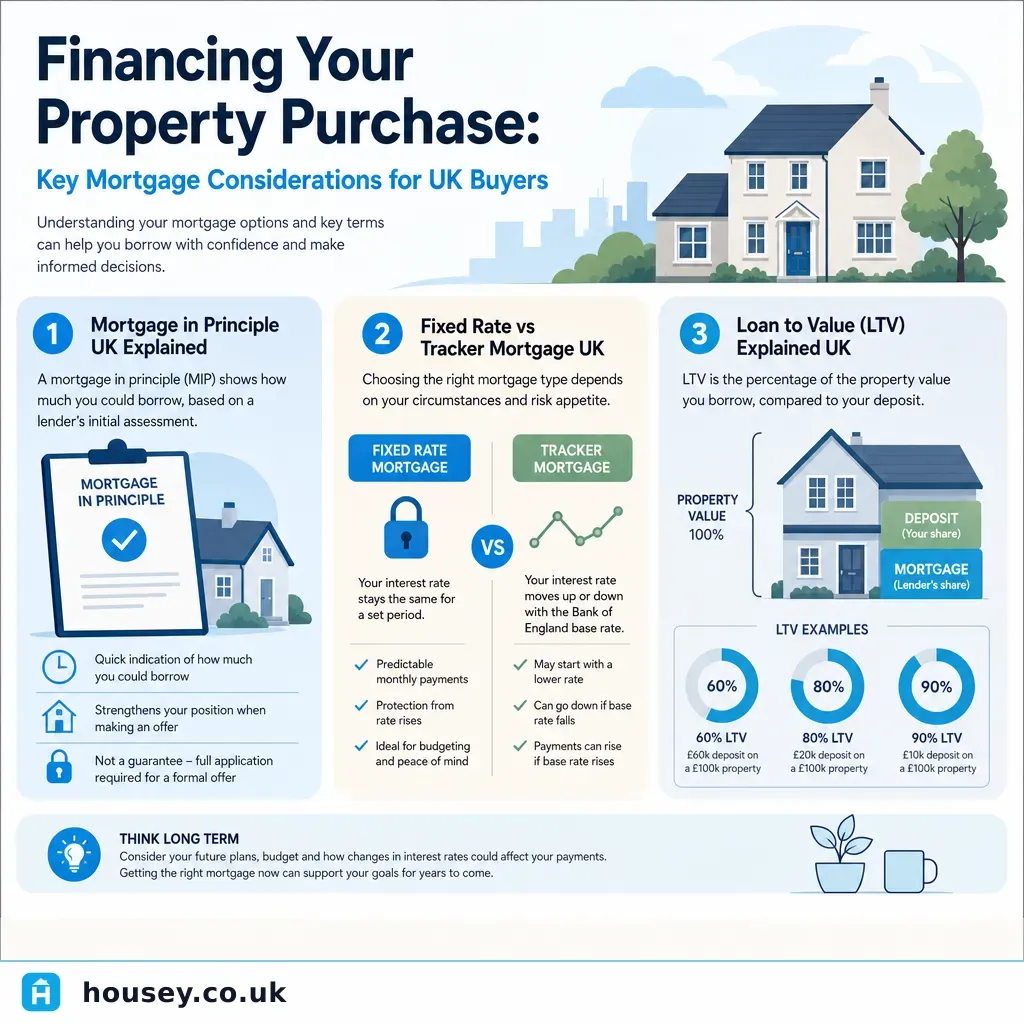

Buying & MovingFinancing Your Property Purchase: Key Mortgage Considerations for UK Buyers

Choosing the right mortgage involves matching the product type to your circumstances, not just comparing headline rates. Your loan-to-value ratio, income structure, and credit history determine which products you can access and at what cost. A formal mortgage offer is different from an Agreement in Principle and is only issued after the lender has valued the property and assessed your full application.

Buying & Moving

Buying & MovingValuing Your Home: Tools and Methods for Property Estimation

You can estimate your home's value using online automated tools, Land Registry sold prices, and estate agent appraisals — but these differ significantly in accuracy and purpose. For a mortgage, remortgage, or legal matter, only a formal RICS Red Book valuation prepared by a registered valuer carries the authority that lenders and courts require.

Buying & Moving

Buying & MovingOver-Improving Your Home: When Investment Returns Diminish

Over-improving a property means spending more on renovation than the local market returns at sale. Every home has a ceiling value set by comparable sales on the same street — improvements move a property towards the top of that range but rarely above it. A pre-works opinion of value from a RICS-registered valuer is the most reliable way to understand your property's ceiling before committing to significant spend.